17 August 2021

Frances Donald, Global Chief Economist & Head of Macro Strategy

We firmly believe that the ESG lens can and should be applied to most traditional macro factors that flow through to investment decisions. While the impact of choosing to embark on such a path may seem subtle initially, we have no doubt that it will soon become a critical component of the macro outlook. We highlight three areas we’ve been focusing on.

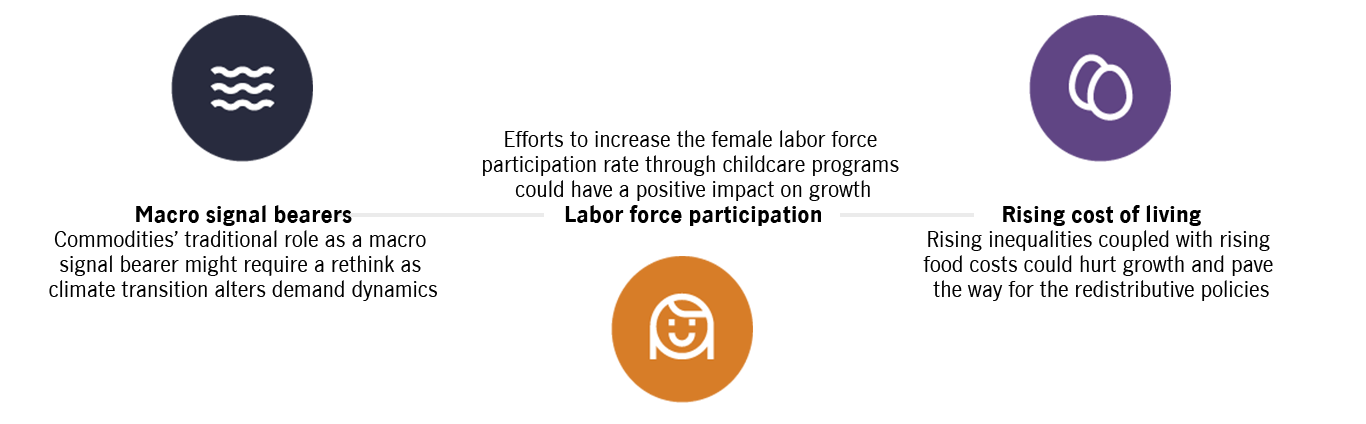

Macro factors that should be increasingly viewed through an ESG lens

Source: Manulife Investment Management, July 1, 2021.

The green transition will likely shift supply/demand functions for a variety of assets, particularly in the commodities space. This transition isn’t only about the opportunities within those asset classes, it’s also about thinking differently about their predictive power and value as macro signals. For example, macro analysts have historically used copper as a cyclical indicator, but the ESG transition is likely to affect the demand/supply dynamic for the commodity in a way that may muddy its predictive abilities. Meanwhile, the price of lithium and cobalt—key to manufacturing batteries for electric vehicles—could become an important macro indicator as consumer adoption of electric cars gathers pace. Put differently, viewing changing market dynamics through an ESG lens encourages analysts to evolve their perspective of a historically accepted view that may alter the value we attach to different commodities.

Rising government focus on national childcare programs aimed at increasing female labor force participation rates in a post-COVID-19 environment is a component of the S element in ESG that we believe will have clear implications for growth, inflation, and labor costs. Our preliminary work on this topic suggests that national childcare programs can meaningfully support labor supply, boost growth, and reduce pressure on wages. That said, shifting dynamics within the labor force and the nature of work available aren’t restricted to childcare programs and working parents—an increased policy focus on the economic consequences of gig workers is likely to press on the S in ESG in a more meaningful way. In our view, it’s time to start actively considering how diversity, equity, and inclusion policies will inform macroeconomic analysis going forward.

Income inequality is widening globally—it’s an important issue that needs addressing, particularly at a time in which we’re also experiencing rising food price inflation. We see this as a growing risk to the global economic outlook, particularly within the context of a rising global population and sustained deforestation, which could have an adverse impact on food supply. These developments can dent aggregate demand, especially in emerging markets, and lead to political instability, increasing the need for us to add a geopolitical risk premium to our analysis.

Over the course of the last few years, we’ve come to view the integration of ESG factors into macroeconomic analysis as less of a choice and more of a necessity. We are, after all, in the business of identifying emerging trends and evaluating how they could lead to opportunities or translate into headwinds to growth. In our view, failure to apply an ESG lens to all aspects of macroeconomic analysis would hinder our ability to do our work and do it well.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

17 August 2021

Frances Donald, Global Chief Economist & Head of Macro Strategy

We firmly believe that the ESG lens can and should be applied to most traditional macro factors that flow through to investment decisions. While the impact of choosing to embark on such a path may seem subtle initially, we have no doubt that it will soon become a critical component of the macro outlook. We highlight three areas we’ve been focusing on.

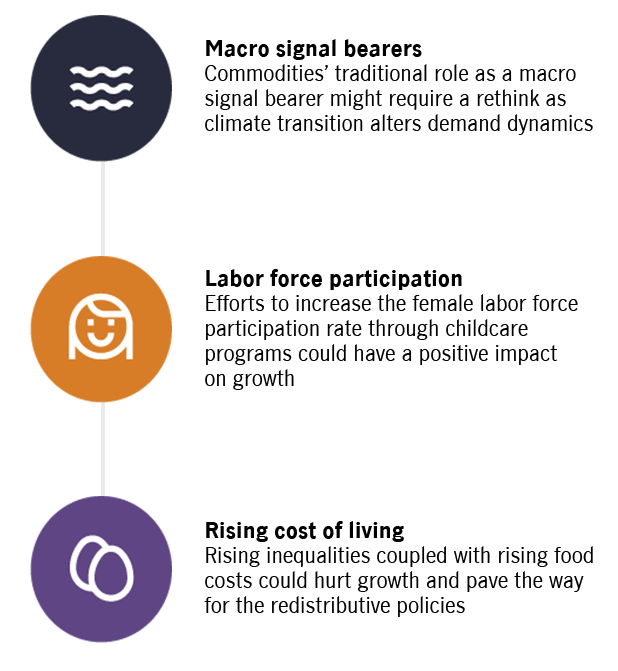

Macro factors that should be increasingly viewed through an ESG lens

Source: Manulife Investment Management, July 1, 2021.

The green transition will likely shift supply/demand functions for a variety of assets, particularly in the commodities space. This transition isn’t only about the opportunities within those asset classes, it’s also about thinking differently about their predictive power and value as macro signals. For example, macro analysts have historically used copper as a cyclical indicator, but the ESG transition is likely to affect the demand/supply dynamic for the commodity in a way that may muddy its predictive abilities. Meanwhile, the price of lithium and cobalt—key to manufacturing batteries for electric vehicles—could become an important macro indicator as consumer adoption of electric cars gathers pace. Put differently, viewing changing market dynamics through an ESG lens encourages analysts to evolve their perspective of a historically accepted view that may alter the value we attach to different commodities.

Rising government focus on national childcare programs aimed at increasing female labor force participation rates in a post-COVID-19 environment is a component of the S element in ESG that we believe will have clear implications for growth, inflation, and labor costs. Our preliminary work on this topic suggests that national childcare programs can meaningfully support labor supply, boost growth, and reduce pressure on wages. That said, shifting dynamics within the labor force and the nature of work available aren’t restricted to childcare programs and working parents—an increased policy focus on the economic consequences of gig workers is likely to press on the S in ESG in a more meaningful way. In our view, it’s time to start actively considering how diversity, equity, and inclusion policies will inform macroeconomic analysis going forward.

Income inequality is widening globally—it’s an important issue that needs addressing, particularly at a time in which we’re also experiencing rising food price inflation. We see this as a growing risk to the global economic outlook, particularly within the context of a rising global population and sustained deforestation, which could have an adverse impact on food supply. These developments can dent aggregate demand, especially in emerging markets, and lead to political instability, increasing the need for us to add a geopolitical risk premium to our analysis.

Over the course of the last few years, we’ve come to view the integration of ESG factors into macroeconomic analysis as less of a choice and more of a necessity. We are, after all, in the business of identifying emerging trends and evaluating how they could lead to opportunities or translate into headwinds to growth. In our view, failure to apply an ESG lens to all aspects of macroeconomic analysis would hinder our ability to do our work and do it well.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited