20 May 2026

Ryan Davies, CFA Senior Portfolio Manager

Michael P. Evans, CFA Managing Director, Equity Client Portfolio Manager

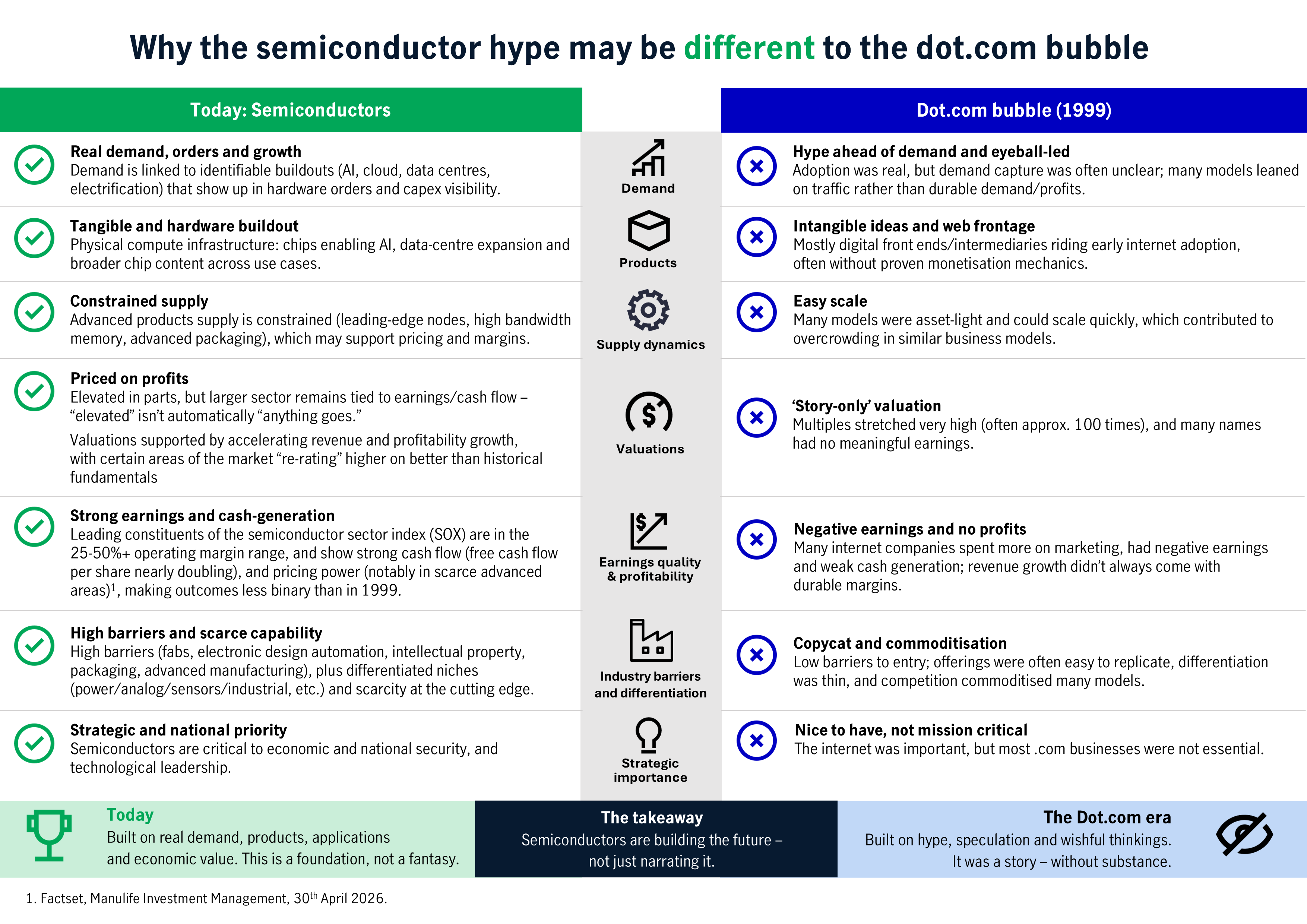

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

A typical day now runs on semiconductors.

You wake up, check your phone, and the screen adjusts brightness automatically. You commute in a car filled with electronics that manage safety, power and navigation. At work, you open documents stored in the cloud. At night, you stream, game, or ask an artificial intelligence (AI) tool to help you learn something new.

Most of this feels like “apps” and “software.” But under the surface, it’s driven by an industrial-scale ecosystem that designs, builds and tests the electronic components that make the digital world function. That ecosystem is the global semiconductor industry.

“Semiconductors” don’t just mean one kind of chip. It includes different device types, each doing a different job:

But the industry is also the supply chain that makes these devices possible – spanning design, raw materials, wafers, photomasks, manufacturing equipment, production, and back-end inspection, testing and packaging.

In other words, semiconductors are the backstage crew behind model life. The sector can mean a much wider set of businesses than just the most talked-about chip brands.

The world is being rebuilt around three forces that reinforce each other.

1. AI and data centres are scaling fast

AI is pushing data centre demand higher – and not only for raw computing, but also for the connectivity that links processors, memory, and networks. Compute capacity is a bottleneck and can be “consumed as soon as it is installed,” which is another way of saying demand is pressing hard on supply.

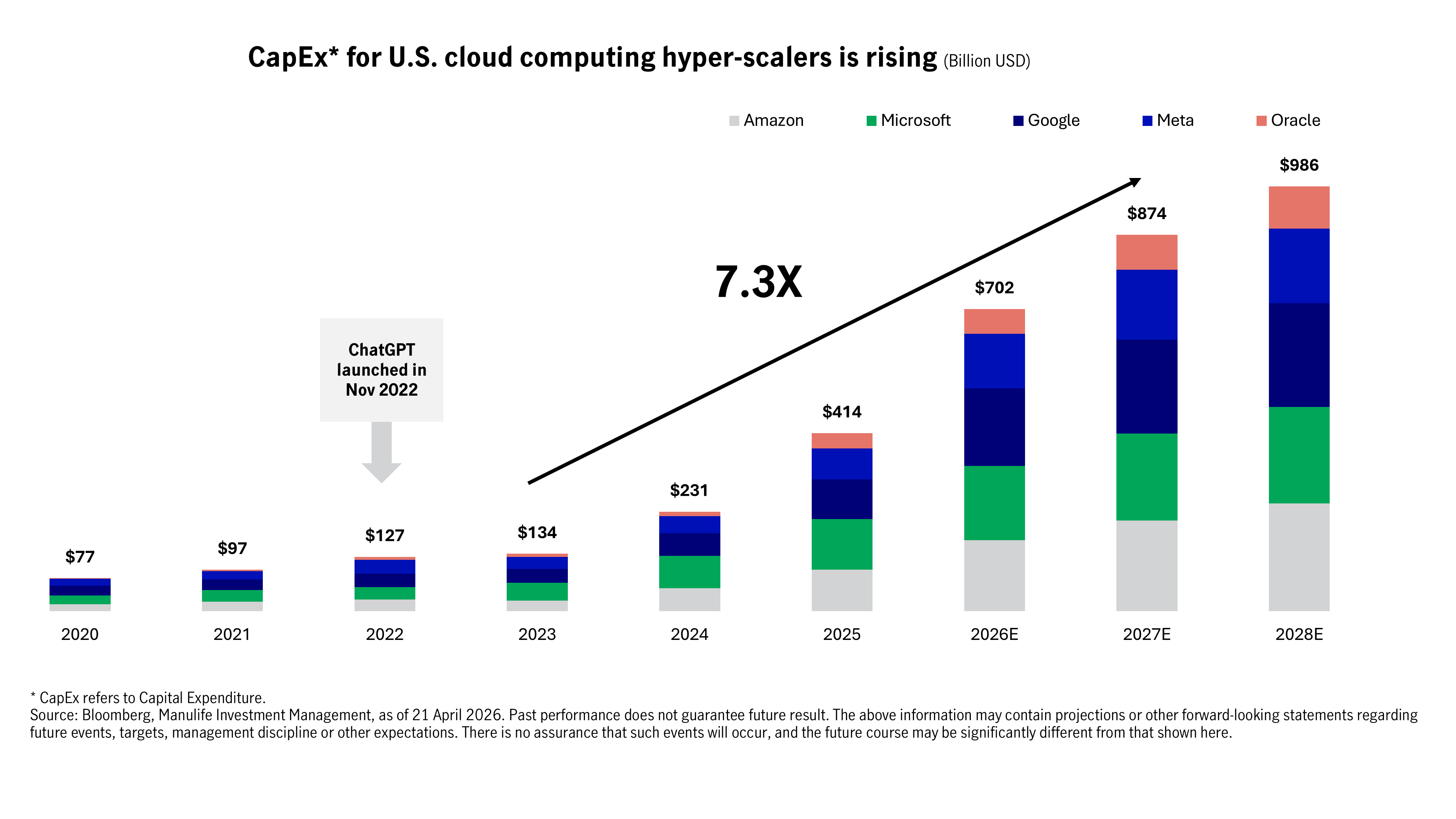

And the spend is no longer theoretical. The capital expenditure (CapEx) of the major U.S. hyper-scalers is projected to rise from US$77 billion (2020) to US$986 billion (2028E) – a 7.3x increase.

2. The world is electrifying

From electric vehicles (EVs), charging to renewables to modern data centres, energy is increasingly a constraint. That puts a spotlight on power efficient chips – exactly the kind of challenge that power-related semiconductors help solve.

3. Technology is moving into the physical world

Robotics and automation are long-term themes, including humanoid robots, which require multiple types of semiconductors: sensors to perceive, logic to decide, and power management to operate. All of these are not ‘one-quarter’ trends, they are multi-year shifts.

When markets pull back, it’s easy to assume the story is over. But in semiconductors, the long-term story is tied to real budgets and long-lived infrastructure.

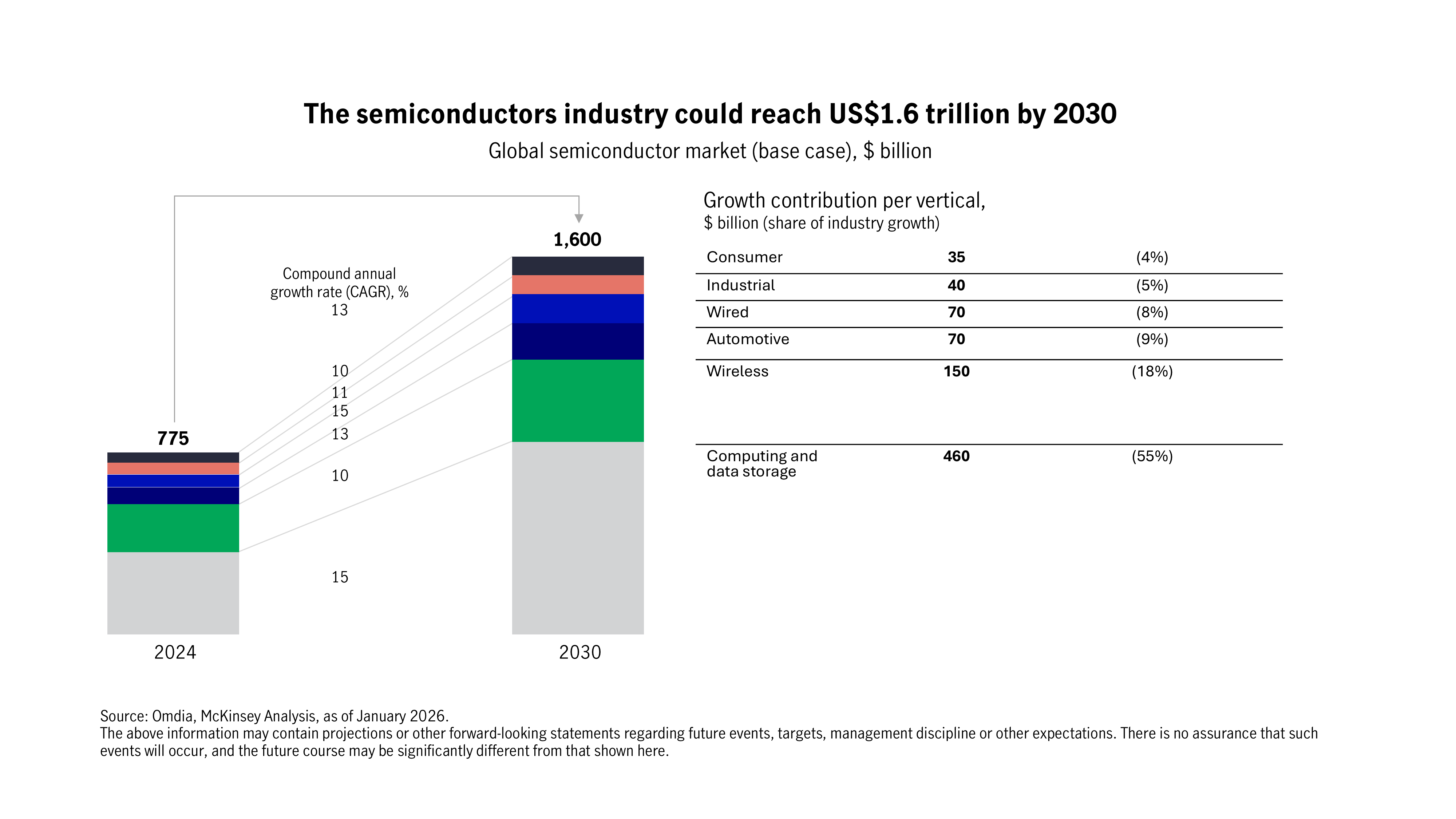

The global semiconductor market is projected to reach US$1.6 trillion by 2030, up from US$775 billion in 2024 – at 13% compound annual growth rate (CAGR).

These underline the direction of travel that huge amounts of investments are being committed to build capacity.

And this is where today’s environment starts to look different from the dot-com era.

Parts of the market can get overheated; drawdowns happen. But the direction is hard to ignore: a larger chip market by 2030, accelerating infrastructure spend, a widening set of real-world applications, and tightness in advanced supply.

If AI is a race, semiconductors are the track, the timing system, the stables and the supplies. You don’t need to know exactly which runner wins to believe that the race itself is getting bigger.

Buying a couple of headline AI or semiconductor names may feel simple, but it may also make your portfolio fragile. Semiconductor sub-sectors don’t move together; different parts of the chain may peak at different times. And what’s popular today may not be the leader tomorrow.

That’s exactly why an early pure player, with an active management approach may matter and help:

For investors, the opportunity may be less about guessing the next headline winner – and more about owning the ecosystem that makes the digital world work.

Real assets and the infrastructure behind AI

Artificial intelligence (AI) is often positioned as a story of models and applications, but its growth depends heavily on something far more tangible. Real assets such as data centres, power grids, and raw materials form the physical that supports AI development. As structural forces reshape the investment landscape, real assets are emerging as an enabler of the AI buildout.

The engine behind AI: Semiconductors are fuelling the next era of technology

Semiconductors belong to one of the most specialised yet globally integrated industry chains. From design, equipment, and materials to manufacturing and commercialisation, the production of a smartphone chip alone spans many countries across continents, creating tremendous opportunities for companies, consumers, and investors. With semiconductors increasingly becoming the backbone of an artificial intelligence (AI) race few are prepared for, understanding this sector is key to unlocking where the next wave of technology competition is heading.

AI innovation: Asia helps build many of the world’s technologies behind it

When electricity first arrived, the world built the necessary infrastructure – power plants, transmission lines – before the real transformation could take hold. A similar process is happening with artificial intelligence (AI). Today's massive investment in chips, data centres, and power grids is laying the foundation for a potential expansion in AI application that could take years to develop. In our view, the discussion is increasingly shifting from whether AI adoption will continue to how the enabling infrastructure is being built. Asia appears to be playing an important role in that development.

Real assets and the infrastructure behind AI

Artificial intelligence (AI) is often positioned as a story of models and applications, but its growth depends heavily on something far more tangible. Real assets such as data centres, power grids, and raw materials form the physical that supports AI development. As structural forces reshape the investment landscape, real assets are emerging as an enabler of the AI buildout.

The engine behind AI: Semiconductors are fuelling the next era of technology

Semiconductors belong to one of the most specialised yet globally integrated industry chains. From design, equipment, and materials to manufacturing and commercialisation, the production of a smartphone chip alone spans many countries across continents, creating tremendous opportunities for companies, consumers, and investors. With semiconductors increasingly becoming the backbone of an artificial intelligence (AI) race few are prepared for, understanding this sector is key to unlocking where the next wave of technology competition is heading.

AI innovation: Asia helps build many of the world’s technologies behind it

When electricity first arrived, the world built the necessary infrastructure – power plants, transmission lines – before the real transformation could take hold. A similar process is happening with artificial intelligence (AI). Today's massive investment in chips, data centres, and power grids is laying the foundation for a potential expansion in AI application that could take years to develop. In our view, the discussion is increasingly shifting from whether AI adoption will continue to how the enabling infrastructure is being built. Asia appears to be playing an important role in that development.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited