4 June 2026

Paula Chan, Head of Hong Kong Fixed Income, Senior Portfolio Manager

Isaac Meng, Portfolio Manager

After a prolonged period of deflation, China’s economy is turning the corner towards inflation. In this investment note, the China Fixed Income team analyses why this reflationary transition is important for China bonds and offers implications for investors in government policy, rates, and the renminbi.

China has experienced a prolonged period of deflationary pressure over the past three years. Recent data indicate that pricing dynamics are improving, with early signs of a reflationary impulse emerging. Producer price inflation has turned positive for the first time since late 2022, while core consumer inflation has stabilised at modestly positive levels.

These developments point to a meaningful shift in momentum and suggest that China may be moving away from a deflationary regime toward a more benign inflationary environment.

For markets, this transition represents an inflexion in the macro backdrop. We expect policy to remain broadly accommodative, and government bond yields to be range-bound, and the renminbi to exhibit a gradual appreciation bias.

In this context, China fixed income continues to offer attractive diversification characteristics supported by stable carry, a steep curve, low correlation to global rates, and relatively predictable policy dynamics.

China’s recent deflationary phase has been shaped by both cyclical weakness and deeper structural imbalances. The downturn in the property sector—historically accounting for between 20 and 30 per cent of economic activity—has significantly weighed on domestic demand. At the same time, persistent industrial overcapacity and intense price competition have exerted downward pressure on producer prices. These domestic dynamics have been compounded by a challenging external environment, including trade frictions and uneven global demand.

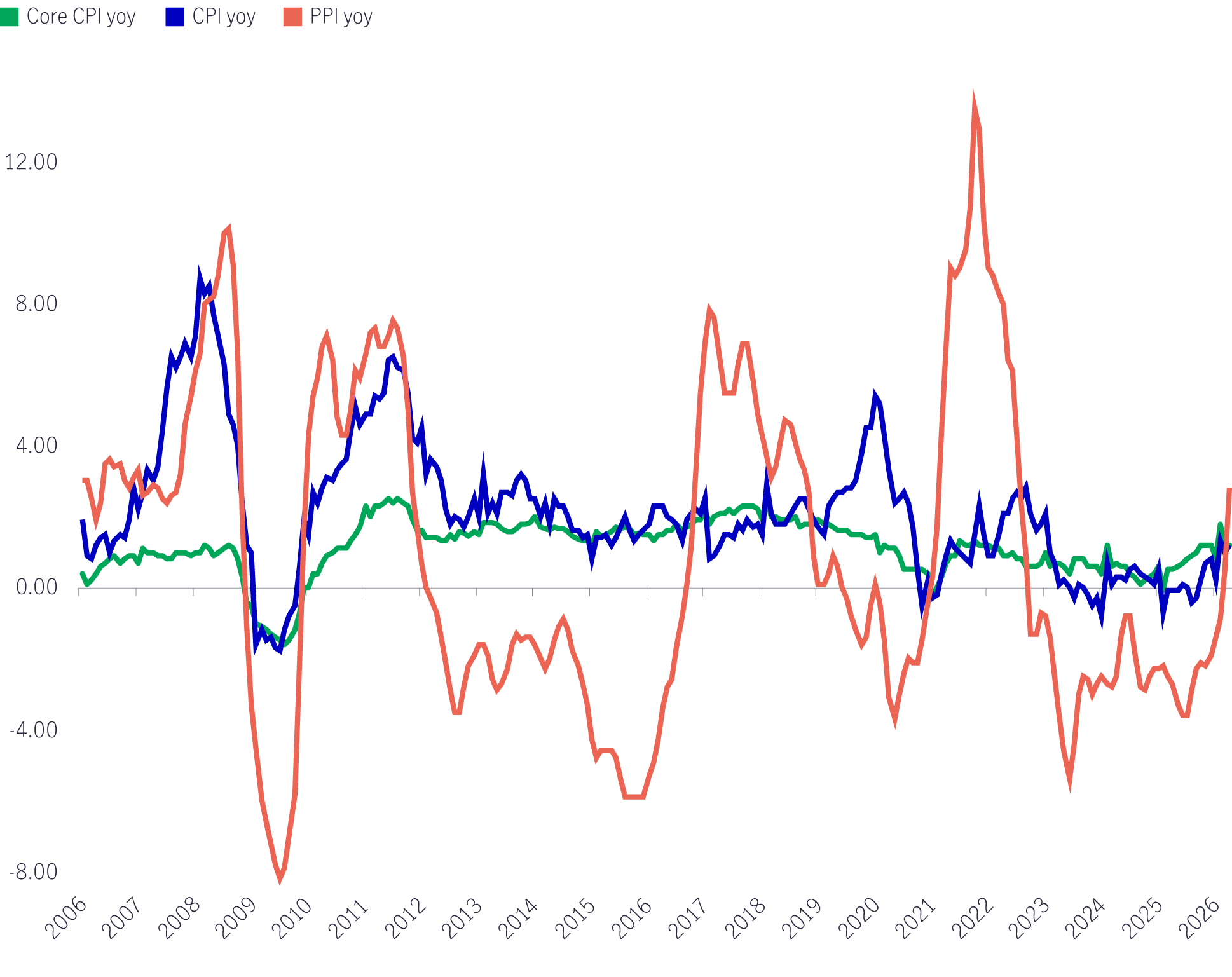

Recent data suggests that this period of persistent price weakness may be approaching an inflexion point. Producer price inflation, which has remained negative since October 2022, turned positive in March 2026 and strengthened further in April, with readings of +0.5 per cent year-on-year and +2.8 per cent year-on-year, respectively.

Consumer price inflation also accelerated to +1.2 per cent year-on-year, its fastest pace since early 2023, while core inflation, which excludes energy and food prices, has stabilised at around 1.2 per cent year-on-year, suggesting that the recent energy shock is not entirely driving inflation.

These developments point to visible improvement in pricing momentum and are consistent with the early stages of a transition from disinflation to a more stable inflation environment. Taken together, the latest inflation prints appear consistent with the Chinese economy successfully transitioning from disinflation towards benign reflation – where rising inflation is still within a comfortable range and is neutral for monetary policy.

Chart 1: Historical PPI, CPI, and Core CPI (%, Y/Y)1

The emerging reflationary impulse appears to be driven by a combination of external factors and sector-specific demand, rather than a broad-based recovery in domestic consumption.

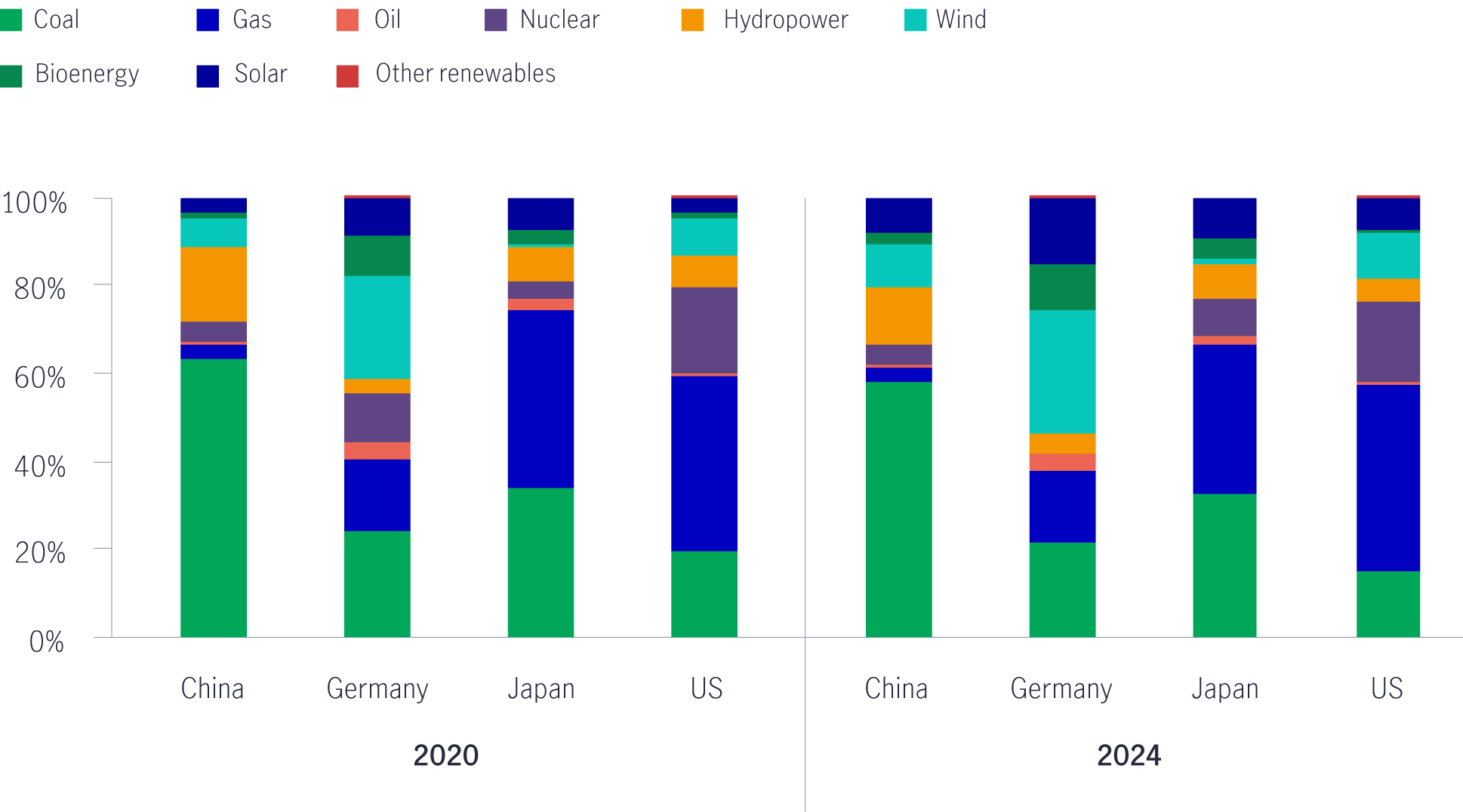

Part of the recent improvement reflects higher energy prices following developments in the Middle East, which have supported headline inflation. However, China’s structural shift toward renewable energy, electrification, and increased energy self-sufficiency suggests that the economy is less exposed to sustained energy shocks than in previous cycles. This implies that energy has acted more as a catalyst for reflation than a persistent driver.

External demand has also played an important role. Following a period of global inventory drawdowns, the international cycle has shifted toward restocking, supporting export volumes. At the same time, demand from high-growth sectors—particularly technology hardware, electric vehicles, batteries, and renewable energy equipment—has remained robust. These sectors are tied to ongoing investment cycles and policy-driven transitions, rather than purely cyclical consumption, and therefore provide a more durable underpinning to export activity.

Taken together, these dynamics imply that the current reflationary impulse remains uneven. It is still concentrated in upstream and tradable sectors, with limited transmission thus far into services, wages, or household demand. Whether this impulse broadens to the domestic economy will be the key determinant of macro policy direction.

Chart 2: China’s lower reliance on oil and gas for power generation2

A sustained shift away from deflation has important macro-financial implications. Stabilising prices support nominal gross domestic product (GDP) growth, which in turn strengthens corporate revenues, improves debt-servicing capacity, and reinforces fiscal dynamics. This helps reduce the risk of a debt-deflation feedback loop, in which falling prices increase the real burden of debt, forcing deleveraging and further weakening demand.

An improving inflation backdrop may also influence household behaviour. With deflation risks receding, precautionary savings could begin to decline at the margin, particularly if income expectations stabilise. Over time, this could support a gradual recovery in consumption, housing transactions, and broader risk sentiment. However, such effects are likely to be gradual and contingent on sustained improvements in labour market and income dynamics.

The transition toward a more stable inflation environment does not imply an imminent shift in monetary policy. Core inflation remains modest, and the recovery in domestic demand is still uneven. As a result, the People’s Bank of China will likely maintain a broadly accommodative stance, with policy priorities focused on improving credit transmission and maintaining financial stability, particularly in relation to property and local government balance sheets, as well as managing expectations around its currency.

Rather than tightening policy in response to improving inflation prints, China’s central bank is more likely to look through initial inflation rebound, and rely on liquidity operations and targeted measures to support the economy. This approach reflects the reality that reflation remains incomplete and the underlying demand environment has yet to fully normalise.

For rates, the shift in inflation dynamics does not necessarily imply a sustained upward move in yields. In the absence of a strong recovery in private credit demand, structural demand for high-quality assets is likely to remain strong. As a result, government bond yields are expected to remain broadly range-bound, with a 1.70%-1.90% range for 10-year China Government Bonds (CGBs), rather than entering a sustained sell-off.

A more pronounced steepening of the yield curve would likely require clearer evidence of a domestic demand recovery, including sustained improvement in credit growth and recovery in the property sector.

From a currency perspective, the end of deflation reduces the need for defensive positioning and, together with China’s strong external balances, supports a gradual appreciation bias in the renminbi. At the same time, policymakers are likely to continue managing the pace, suggesting that any appreciation path will be measured rather than abrupt.

DThe shift from persistent deflation toward a more stable pricing environment represents a meaningful improvement in China’s macroeconomic backdrop. However, the current reflationary impulse is driven primarily by external and upstream factors, rather than a broad-based recovery in domestic demand. This suggests that the adjustment will be gradual and highly dependent on whether reflation can be transmitted to consumption, wages, and credit growth.

In this environment, China fixed income remains an attractive component of global portfolios. Stable yields, an accommodative policy framework, and improving inflation dynamics combine to offer a supportive backdrop for investors seeking diversification and steep yield curve rolldown. While risks remain—particularly around global demand and the durability of the current impulse—the transition away from deflation marks an important turning point for the macroeconomic outlook. It strengthens the case for global investors to reassess their strategic allocations to China fixed income.

1 Source: Manulife Investment Management, Bloomberg, as of 30 April 2026.

2 Source: Barclays, as of November 2025.

AI innovation: Asia helps build many of the world’s technologies behind it

When electricity first arrived, the world built the necessary infrastructure – power plants, transmission lines – before the real transformation could take hold. A similar process is happening with artificial intelligence (AI). Today's massive investment in chips, data centres, and power grids is laying the foundation for a potential expansion in AI application that could take years to develop. In our view, the discussion is increasingly shifting from whether AI adoption will continue to how the enabling infrastructure is being built. Asia appears to be playing an important role in that development.

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

AI innovation: Asia helps build many of the world’s technologies behind it

When electricity first arrived, the world built the necessary infrastructure – power plants, transmission lines – before the real transformation could take hold. A similar process is happening with artificial intelligence (AI). Today's massive investment in chips, data centres, and power grids is laying the foundation for a potential expansion in AI application that could take years to develop. In our view, the discussion is increasingly shifting from whether AI adoption will continue to how the enabling infrastructure is being built. Asia appears to be playing an important role in that development.

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited