19 January 2026

The global semiconductor industry remains strong – arguably the most robust we have seen in over three decades. This strength is supported by cutting-edge innovation, rising revenues and robust capital spending. While risks remain, the outlook for 2026 appears constructive, with demand for artificial intelligence (AI) applications showing few signs of slowing. Beyond AI, the non-AI markets could be poised for positive revisions as cyclical recovery gains traction after several years of consolidation.

The semiconductor market is valued at over US$500 billion1 and is projected to surpass US$1 trillion by 20302. Growth is being fuelled primarily by AI, especially in data centres, alongside accelerating demand from automotive and industrial sectors. Regionally, the focus is on Asia Pacific, which has the largest market share.

While fluid as more companies update their plans, capital expenditure among major data-centre hyperscalers is forecast to rise 30% in 2026 and 15% in 20273, supported by strong free cash flow generation, healthy earnings and favourable returns on investment (ROI). This trend suggests continued momentum for the industry.

The PHLX Semiconductor Sector Index (SOX) experienced sharp declines in April 2025 following tariff-related uncertainty, but the recovery was swift. Historically, when the SOX bottoms, it has outperformed the S&P 500 over one- and two-year periods – a pattern worth noting for long-term investors4.

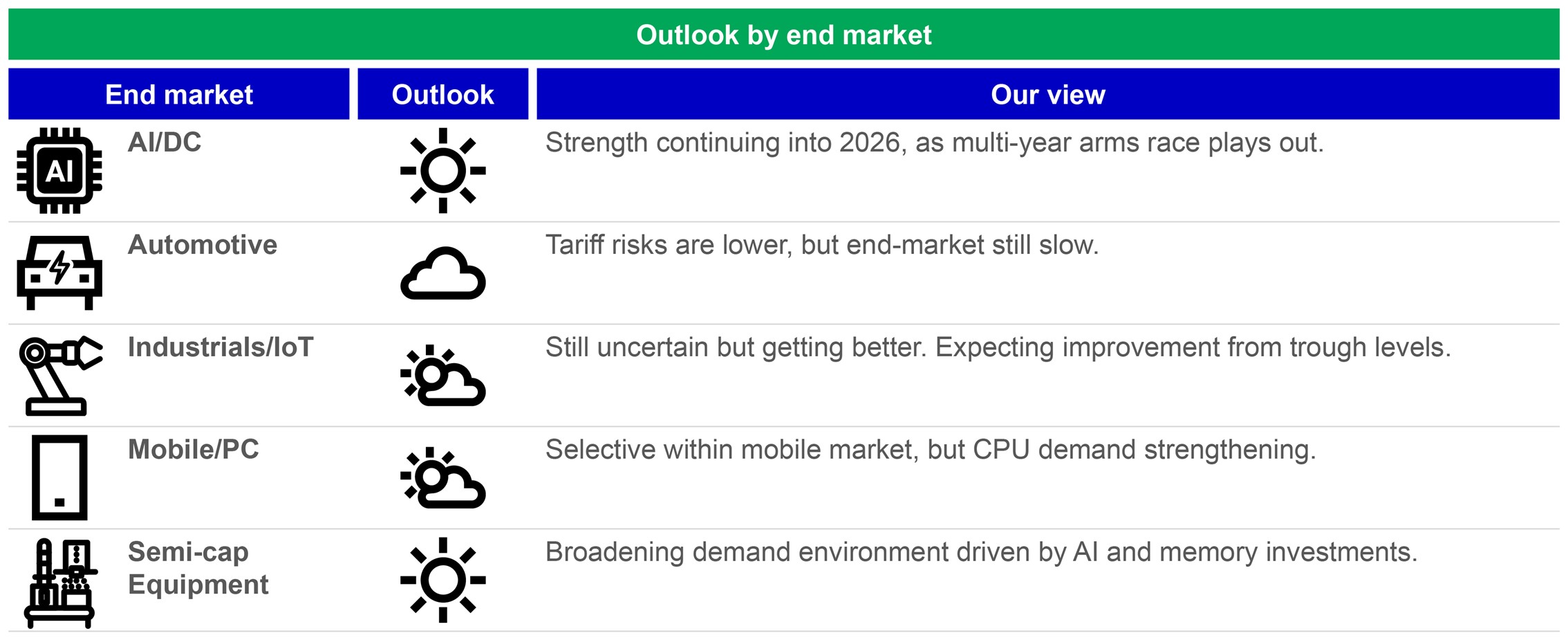

Current “weather outlook” for semiconductors and AI-related industries

For illustrative purposes only.

AI-driven demand is broad-based and shows little sign of slowing, even as we stay mindful of risks such as supply-chain constraints and evolving regulations.

We also continue to see multi-year tailwinds for AI beneficiaries outside of the semiconductor space. Within advertising, AI is being leveraged to expand monetization and create more efficient campaigns. Hyperscale companies report record backlogs as enterprises sign larger and longer deals to support internal AI efforts. Consumer applications like ChatGPT and Gemini should continue to see more usage, while enterprise use-cases should help to push ROI even higher in 2026 and beyond. More broadly, AI is expected to drive an explosion of data over the next decade, driving demand for solutions to manage data in a secure way. Overall, we see increasing opportunities for AI beneficiaries as the technology proliferates further into day-to-day life.

While we believe the outlook for the semiconductor and AI beneficiary industries remains positive, several challenges warrant attention:

Power management

Data centres consume vast energy, raising efficiency concerns. AI generates large datasets, requiring robust safeguards for data security. Moreover, rapid factory expansion in lightly regulated regions could pose sustainability issues.

Debt capital

We expect an increase in debt issuance to finance capital spending through 2026. While overall leverage remains reasonable, and we do not anticipate significant changes, we continue to monitor developments.

Trade tensions

Recent signs of easing between the US and China are encouraging. Our globally diversified exposure provides flexibility to adjust allocations should conditions change.

While global growth concerns and geopolitical risks remain on the radar, they key uncertainty heading into 2026 could be investor sentiment toward semiconductors if AI momentum slows. That said, we expect company fundamentals to stay resilient throughout the year. Our long-term view remains constructive on the extended semiconductor industry and on sectors benefitting from AI adoption.

1 Source: Bloomberg, NXP Semiconductor company reports, and Manulife Investment Management, data as of November 2025.

2 Source: Bloomberg, NXP Semiconductor company reports, and Manulife Investment Management, data as of November 2025.

3 Source: Hyperscale capital expenditure forecasts; FactSet and Manulife Investment Management, data as of November 2025.

4 Source: SOX historical outperformance before and after major declines; SOX outperformance relative to S&P 500; Manulife Investment Management and FactSet Research Systems, data as of November 2025.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited