![]()

New customers - Open an account Existing customers - Register now

14 May 2026

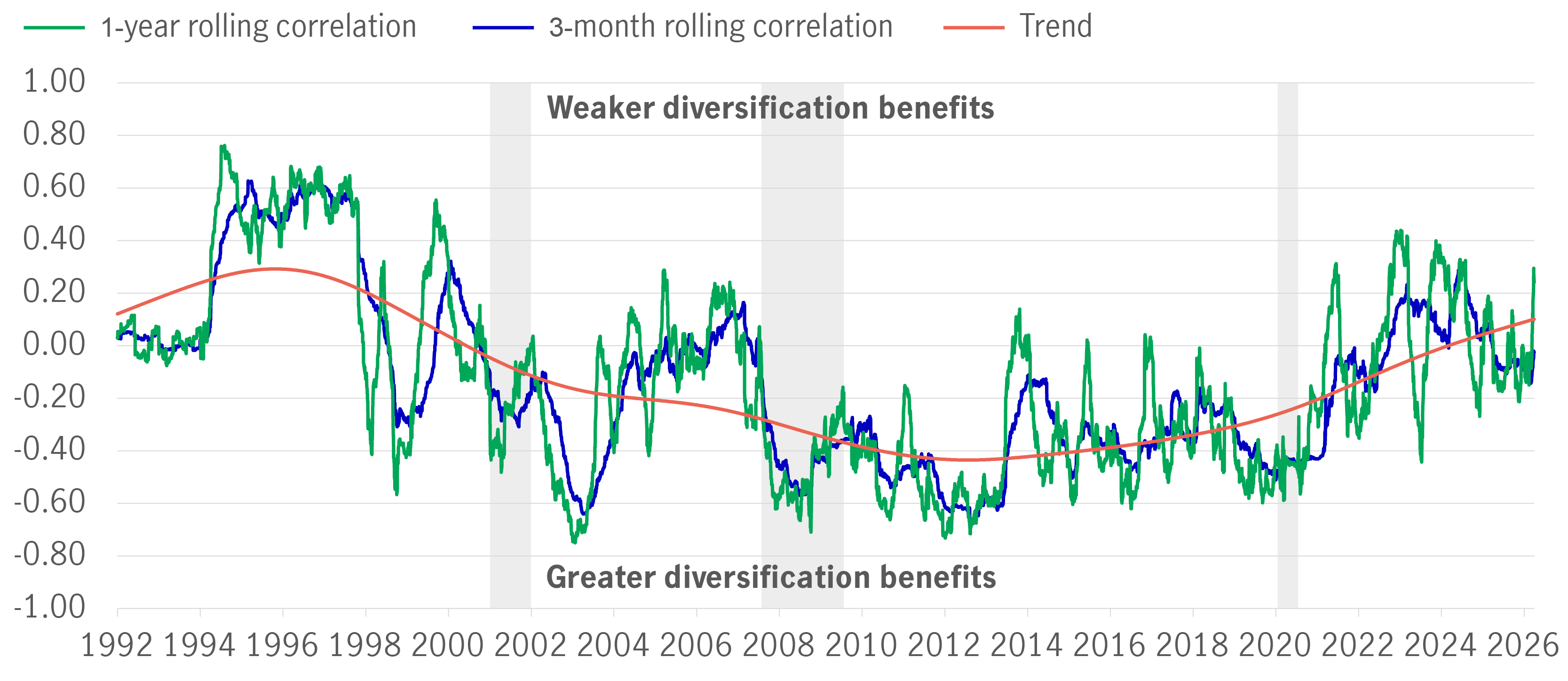

As stock-bond correlations rise, a wider toolkit can help investors navigate a shifting macro landscape

Equity and bond correlations have trended higher as inflation persists, long-term yields remain elevated, and structural forces such as deglobalisation, geopolitical tensions, fiscal expansion, and tariff policies exert pressure. This shift reduces the reliability of traditional diversification and heightens the need for broader sources of portfolio resilience.

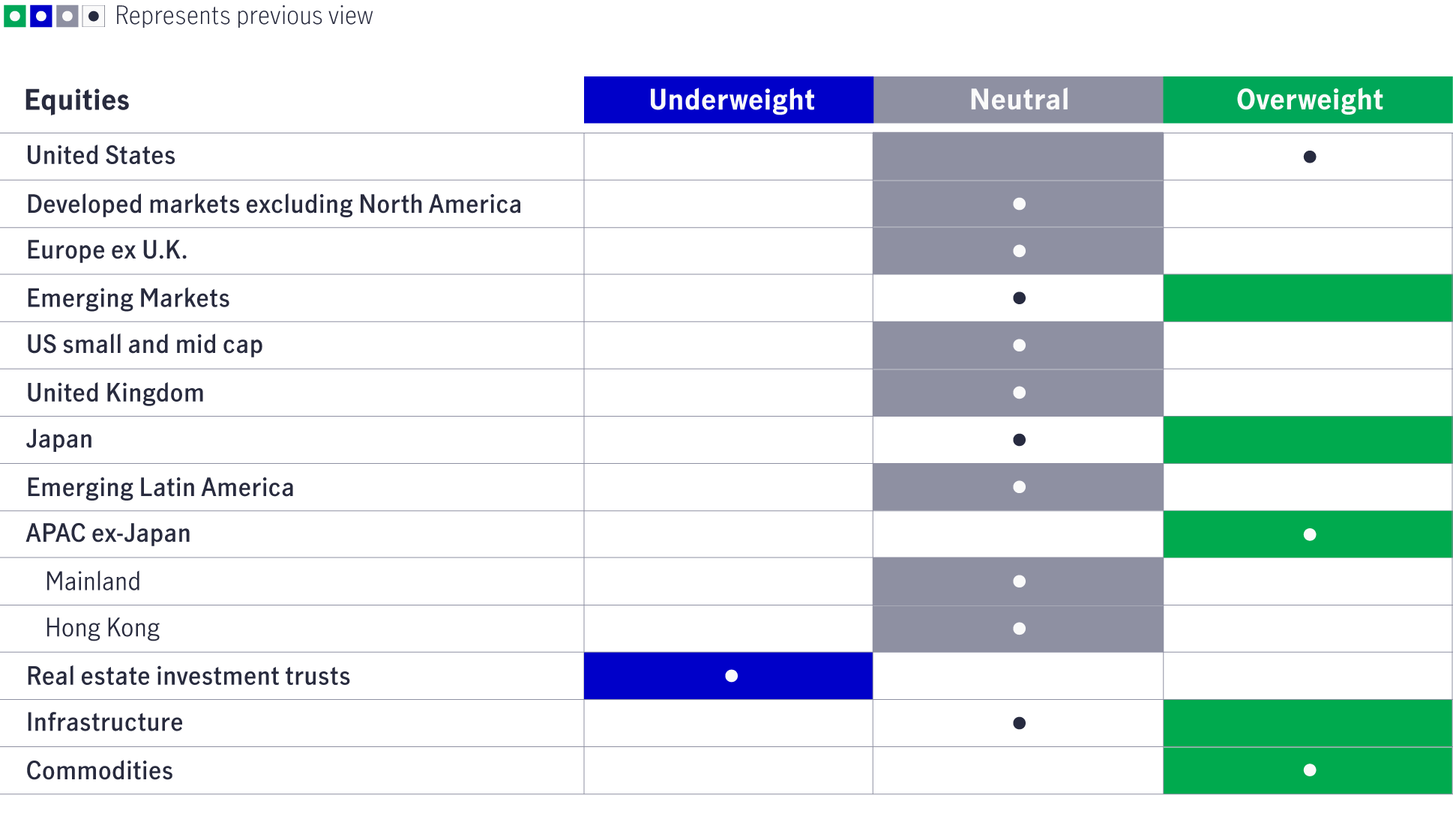

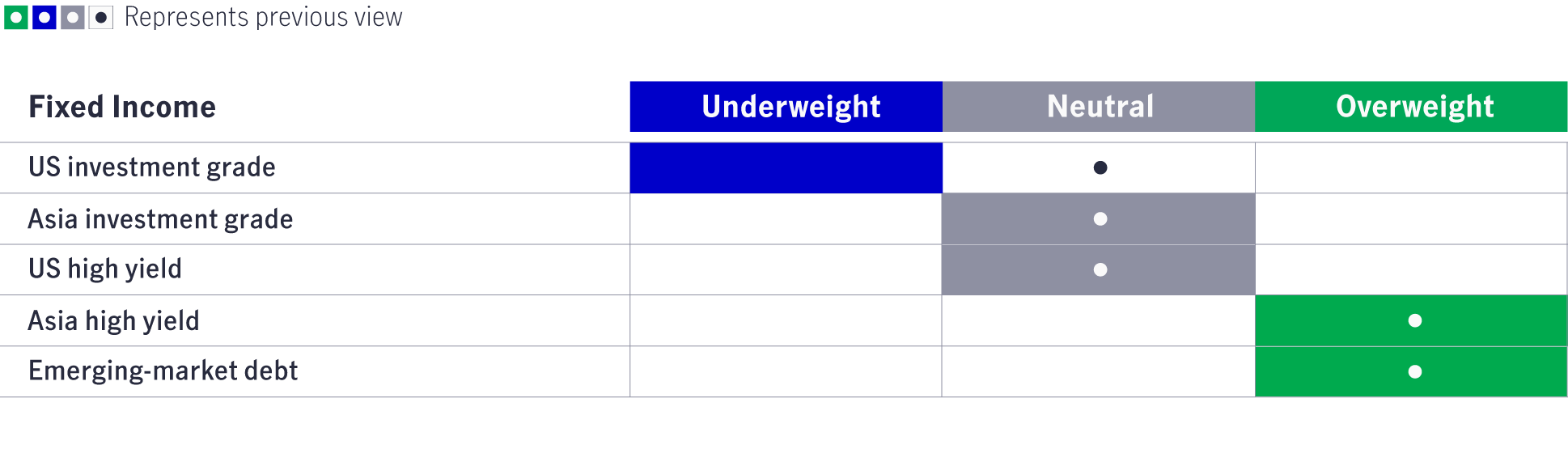

Commodities can offer meaningful diversification, supported by structural strengths in both precious and base metals. Gold benefits from central bank and investors diversification demand, along with supportive currency and policy dynamics. Copper and aluminum should see long-term support from constrained supply, rising strategic importance, and demand tied to electrification, data centers, and industrial substitution. Oil, while structurally challenged, presents a tactical opportunity so long as disruptions in the Strait of Hormuz continue to restrict global flows.

Alternatively, a more diversified mix of real assets, spanning real‑asset‑linked equities, inflation‑linked bonds, and commodities, can help investors weather structurally higher inflation, supply disruptions, and geopolitical fragmentation. Chronic underinvestment and rising long‑term demand from AI, electrification, and the energy transition further reinforce the case for these assets, which can also provide low correlations and durable income.

Liquid alternatives, including strategies like long‑short equity, market neutral, managed futures, and absolute return strategies, can complement equities and bonds by relying less on market direction and more on alpha, trend, and volatility dynamics. These strategies can help manage interest‑rate and equity‑market risk, improve drawdown resilience, and provide a smoother path of returns during periods of heightened uncertainty.

US Stock-Bond Correlation4

1 Source: Manulife Investment Management, 31 March 2026. Projections or other forward-looking statements regarding future events, targets, management discipline or other expectations are only current as of the date indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different than that shown here. .No forecasts are guaranteed. These views are updated on a quarterly basis. This commentary is provided for informational purposes only and is not an endorsement of any security, mutual fund, sector, or index. Diversification does not guarantee a profit or eliminate the risk of a loss.

2 Source: Multi-Asset Solutions Team (MAST), as of 31 March 2026. Projections or other forward-looking statements regarding future events, targets, management discipline or other expectations are only current as of the date indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different than that shown here. Information about asset allocation view is as of issue date and may vary. Active asset allocation views will be updated on a quarterly basis.

3 Source: Multi-Asset Solutions Team (MAST), as of 31 March 2026. Projections or other forward-looking statements regarding future events, targets, management discipline or other expectations are only current as of the date indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different than that shown here.

4 Source: Bloomberg, Macrobond, Manulife Investment Management, as of 19 March 2026. Note: Shaded areas denote US recessions. Stocks are represented by the S&P500 Total Return Index. Bonds are represented by the Bloomberg US Treasury Total Return Index.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited