16 January 2026

Global equity markets delivered strong returns in 2025, supported by steady economic growth, declining inflation, and robust corporate earnings. Aggressive interest rate cuts by central banks, especially the US Federal Reserve, added fuel to the rally. The excitement surrounding artificial intelligence was an additional tailwind for the markets, driving meaningful rally in the US mega-cap technology stocks that dominate global indexes. These positives helped offset concerns about the protectionist shift in US trade policy.

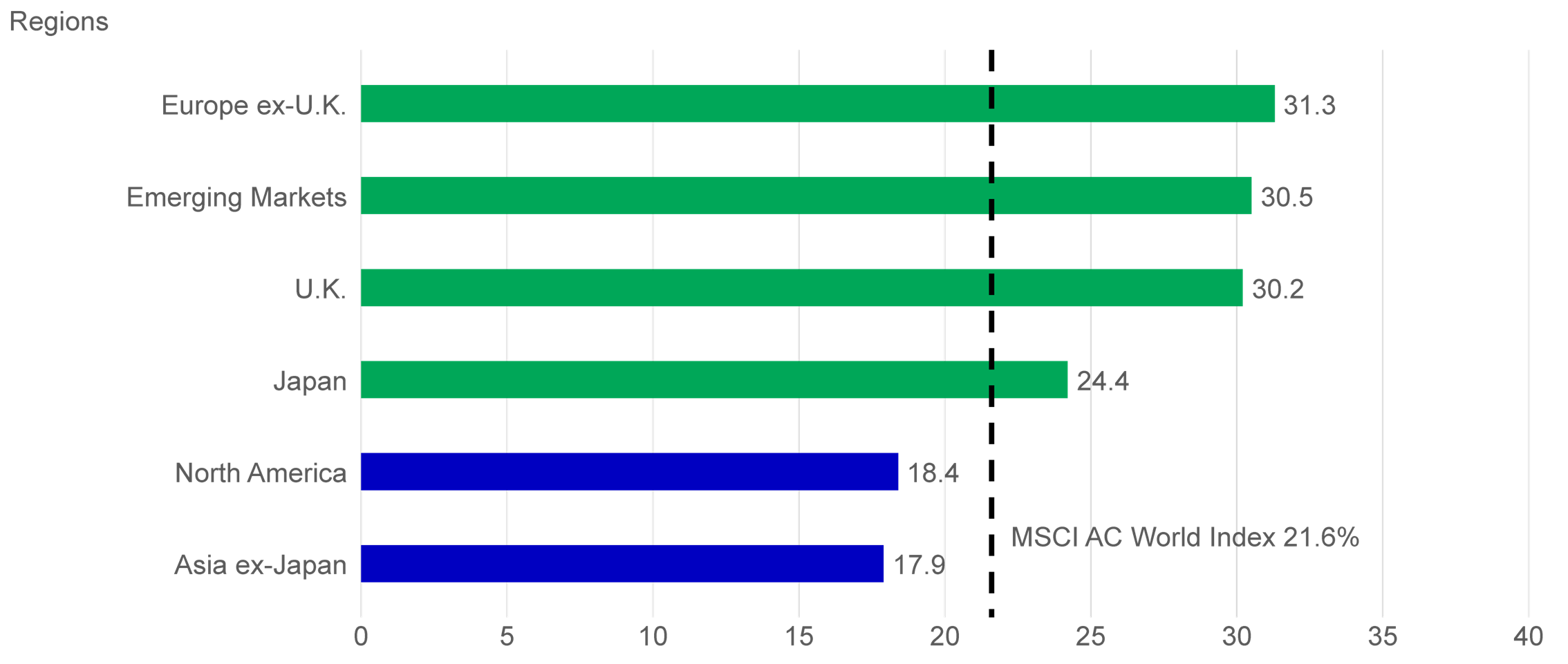

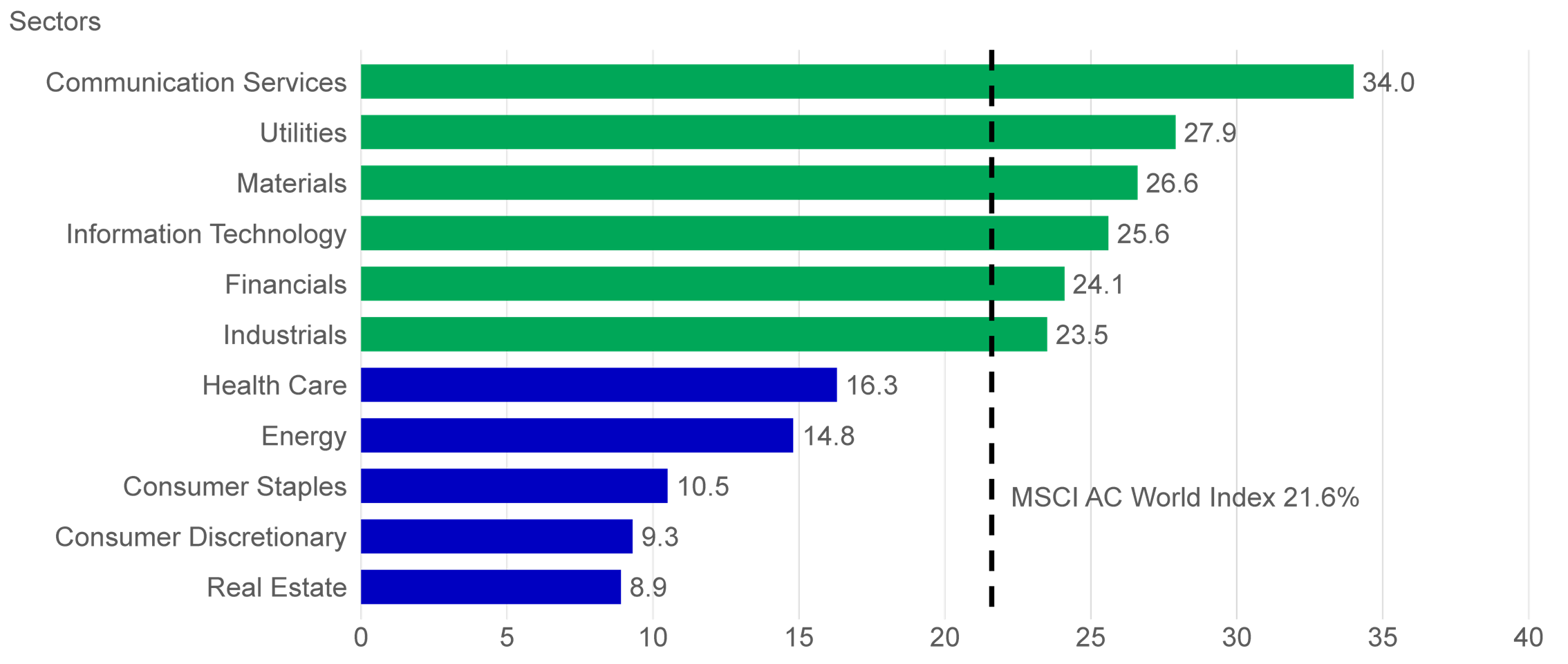

Europe led performance at the regional level, helped by optimism around the potential economic impact of lower interest rates and increased government spending. Emerging markets also outperformed developed markets, showing broad-based strength across regions. The US and developed Asia, posted gains but lagged global peers.

2025 January – November returns of MSCI ACWI regions and sectors

Source: Manulife Investment Management, FactSet Research Systems, data as of 30 November, 2025, in USD. Past performance is not an indicative of future performance. It is not possible to invest directly in an index.

Dynamic leaders are high-quality, industry-leading businesses with attractive growth profiles that have the potential to outpace the market and deliver strong profitability, revenue, earnings, and cash flow. We look for opportunities globally across sectors and markets. While sector weights can shift with valuations and opportunities, several themes guide our approach.

Sectors

Geographies

Company fundamentals and a supportive macro environment should continue to underpin global equities. Resilient economic data and good earnings growth have pushed valuations higher, lifting indexes to record highs. While tariff-related challenges could create short-term headwinds, we believe fiscal and monetary policies remain favourable.

As we enter 2026, we remain positive on equities. We expect opportunities beyond US markets should persist, and industry leaders are likely to strengthen their positions, offering higher return potential.

A continued broadening of market leadership should benefit active strategies like ours. Over the medium to long-term, we believe high-quality industry leaders with strong brands, sound balance sheets, and compounding earnings profiles should continue to deliver consistently solid financial results and share-price returns.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited