23 November, 2020

Endre Pedersen, Chief Investment Officer Fixed Income, Asia ex-Japan

Murray Collis, Deputy Chief Investment Officer Fixed Income (Asia ex-Japan)

On Tuesday 3 November 2020, US voters decided who holds the balance of power in Washington. President-elect Joe Biden was declared the winner of the election (7 November (ET). At the time of writing (16 November, HKT), President Trump has not formally conceded defeat1. In this investment note, Endre Pedersen, Chief Investment Officer, Fixed Income, Asia (ex-Japan) and Murray Collis, Deputy Chief Investment Officer, Fixed Income, Asia (ex-Japan), analyse the impact of the US election on Asian fixed income, examining how a potentially favourable macro backdrop may amplify the strong fundamentals of the asset class.

Overall, assuming the current base case holds, i.e., a Biden presidency and balanced US Congress, we believe the outcome of the US presidential election should be constructive for Asian fixed income.

After months of non-stop campaigning and a hard-fought election, we believe that clarity is one of the greatest benefits to markets. Indeed, there was substantial volatility and uncertainty in the run-up to early November, and the election outcome has catalysed a rally in risk assets. We expect this to continue over the short-term, and it should particularly benefit emerging market (EM) assets, including Asian fixed income.

For Asia, we envisage that a Biden administration might bring greater policy consistency. Over the past four years, Sino-US relations have progressively worsened, particularly economically, punctuated by a prolonged trade dispute with unexpected policy changes that fuelled bouts of market volatility. Although we do not expect a significant improvement in the Sino-US bilateral relationship over the near-term, we believe the possibility exists for more stable, consistently communicated foreign and economic policy coming out of Washington, DC. This should be positive for Asian fixed income markets that previously suffered from volatile policy swings and uncertainty over future actions.

This more favourable macro backdrop for Asian fixed income should be underpinned by accommodative monetary policy globally and a weaker US dollar. In the aftermath of the COVID-19 pandemic, global central banks slashed interest rates to cushion the impact of the economic downturn. We expect monetary policy in developed markets to remain accommodative over the near-term, particularly in the US where a recent Federal Reserve (Fed) revision of its inflation-targeting framework resulted in a projection that interest rates should remain near zero over the next two-to-three years2.

An expansionary Fed will likely be coupled with more active US fiscal policy. While the ultimate scope and quality of stimulus will depend on President-elect Biden’s relationship with Congress, additional federal spending (and an escalating federal deficit) with lower interest rates should put pressure on the US dollar to weaken. We believe that selective Asian currencies, such as the Chinese renminbi and South Korean won, may benefit from this dynamic.

In a post- US election world, the fundamentals of Asian fixed income remain intact: diversified economic growth, resilient credit performance, and relatively attractive nominal and real yields.

The outbreak of COVID-19 dented economic prospects and roiled financial markets across the globe. Asia was no exception, as regional economies contracted in the second quarter due to administrative lockdowns and reduced consumption in Western markets. In our opinion, the region, still boasts some of the best economic prospects globally due to its economic heterogeneity and diversified growth models.

According to the latest IMF forecasts, although Asia’s GDP is expected to experience its worst recent downturn, surpassing even the Asian Financial Crisis (1997–1998), the rate of its contraction is the smallest projected of all major regions, and it is expected to have the strongest economic rebound globally in 20213.

This economic performance, coupled with the region’s unique credit structure, are reasons that Asian credit has remained relatively resilient.

During the first quarter of 2020, when global markets experienced sharp volatility, Asian investment-grade (IG) credit only fell 0.50%, while US (-4.1%) and EM (-8.6%) IG credit posted larger losses4.

Asia’s unique IG structure is one plausible explanation for this divergence in performance. The J.P. Morgan Asian Credit Index (JACI) is largely composed of IG credits (77%). Furthermore, a significant component of the Asian credit market (c. 40%) are state-owned enterprises and quasi-sovereign entities that have access to greater economic resources, including government support and bank loans.

Overall, we believe that Asia will not be immune from the general trend of credit deterioration globally; rating downgrades and defaults are expected to gradually rise over the next two years, although at a relatively lower level in Asia than other regions5. The risk of fallen angels (credits downgraded from investment-grade to non-investment grade) in Asia, although present, should also be more subdued when compared to other global markets6.

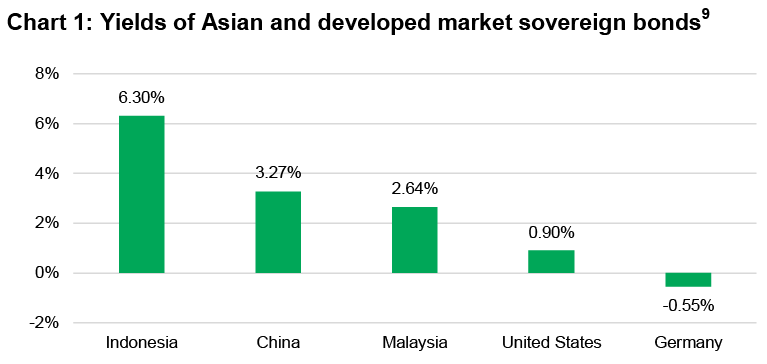

Finally, Asian bonds can offer relatively attractive nominal and real yields compared to their developed-market counterparts. US Treasuries and European sovereign debt currently have nominal yields below 1%, with some returning negative real yields7. In contrast, sovereign bond yields across Asia remain higher, such as in China, Malaysia, and Indonesia, with limited levels of inflation (see Chart 1)8.

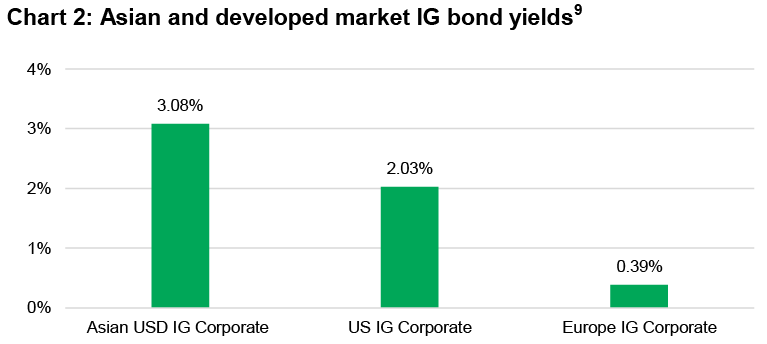

The Asian yield premium can also be observed when comparing USD Asian IG corporate bonds with US and European IG corporate bonds (see Chart 2).

Turning to the other side of the same coin, higher real interest rates could imply that there may be room for monetary easing. With inflation at bay, nominal interest rates in select parts of Asia could do with further monetary easing, which is supportive of select bond prices.

Assuming the current base case for the US presidential election plays out, we envisage a positive impact on Asian fixed income. The clarity of the results, coupled with the possibility of improved policy consistency out of Washington, should be well received by markets as investors can focus on fundamentals and take advantage of the growth and rate differentials uniquely presented in Asia.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

1 On Saturday 7 November 2020, Biden captured the presidency when The Associated Press declared him the victor in his native Pennsylvania at 11:25 a.m. EST. That victory won him the state’s 20 electoral votes, which pushed him over the 270 electoral-vote threshold needed to prevail; Bloomberg: “Biden declares victory, calls on Americans to mend divisions”, 8 November 2020; The Guardian: “Donald Trump refuses to concede defeat as recriminations begin”, 7 November 2020.

2 WSJ, “Fed signals low rates likely to last several years”. 16 September 2020.

3 IMF 2020 Outlook (October version): “Asia and emerging Asia” is forecast to contract by 1.7% in 2020, the smallest rate of contraction among global regions. ‘Low income developing countries’ is forecast to contract less at 1.2%, but this category is combined of markets aggregated from across the world. In 2021, ‘Asia and emerging Asia’ is projected to grow 8.0% in 2021- the highest rate of any region.

4 The J.P. Morgan Asia Credit Index (JACICTR) represents Asia IG credit performance, while the JP Morgan Corporate Emerging Market Bond Index (JCMBCOMP) represents EM fixed income performance, and the ICE B of A US Corporate Index represents US IG credit performance.

5 Moody's baseline scenario predicts a trailing 12-month APAC high-yield nonfinancial corporate default rate of 6.0% in 2020, up from 1.1% in 2019.

6 Standard and Poor’s, as of 30 June 2020. APAC only recorded one fallen angel thus far through the first half of 2020.

7 The 10-year US Treasury boasted a yield of 0.90% as of 13 November 2020.

8 The Indonesian 10-year government bond yielded 6.30% as of 13 November 2020.

9 Bloomberg, as of 13 November 2020.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited