25 June 2026

Inflation: the unseen tax that gradually erodes investors’ purchasing power

Investors have faced a raft of challenges over the past five years: tariffs, energy shocks, the pandemic, and geopolitical uncertainties. Many of these events have not only amplified market volatility but also increased already-elevated inflationary pressures. Indeed, at the same time, the prices of essential services such as education and health care are projected to go up.

With rising uncertainty, some investors have increased their cash holdings as insurance, particularly in bank deposits. This response is normal: tucking cash away for potential future expenses is good financial management.

However, there is a hidden cost – inflation – if too much cash is put into low-rate deposits, it may deter longer-term retirement goals. The impact of inflation may not be evident immediately, given that it “only” averages around 1% to 2% annually, but the accumulation over a longer 20 to 30-year period may significantly reduce investors’ purchasing power.

Financial advisors generally recommend that people keep at least three to six months of expenses in cash in case of an emergency. Families with more children or greater financial responsibilities might want to consider a larger financial cushion: six to twelve months.

These recommendations, however, are usually associated with savings outside of a defined retirement portfolio. That is, assets not allocated specifically for retirement. Evidence suggests that some individuals may be holding significant cash reserves for use in their later years.

The 2025 Hong Kong Deposit Survey, commissioned by the Hong Kong Deposit Protection Board, found that survey respondents of all ages are saving more:

Further, Manulife’s Asia Care Survey in 2025 shows that survey respondents in Hong Kong, on average, hold roughly 50% of their total savings and investments in cash and cash equivalents.

Holding such large cash balances beyond lower returns can have significant downsides. Some banks offer less-than-attractive rates that change quickly, particularly when interest rates are falling. Additionally, long-term deposits are illiquid, and the depositor usually must pay a penalty to withdraw early.

With persistent inflation expected in the near term, investors may benefit from allocating their cash to other opportunities that offer liquidity and potentially greater protection against higher prices.

In particular, a blend of short-term USD deposits, money-market securities, and bonds may offer higher returns (to preserve and potentially enhance purchasing power) without significantly increasing risk. These opportunities include investments in government debt as well as in debt issued by large corporations or financial institutions.

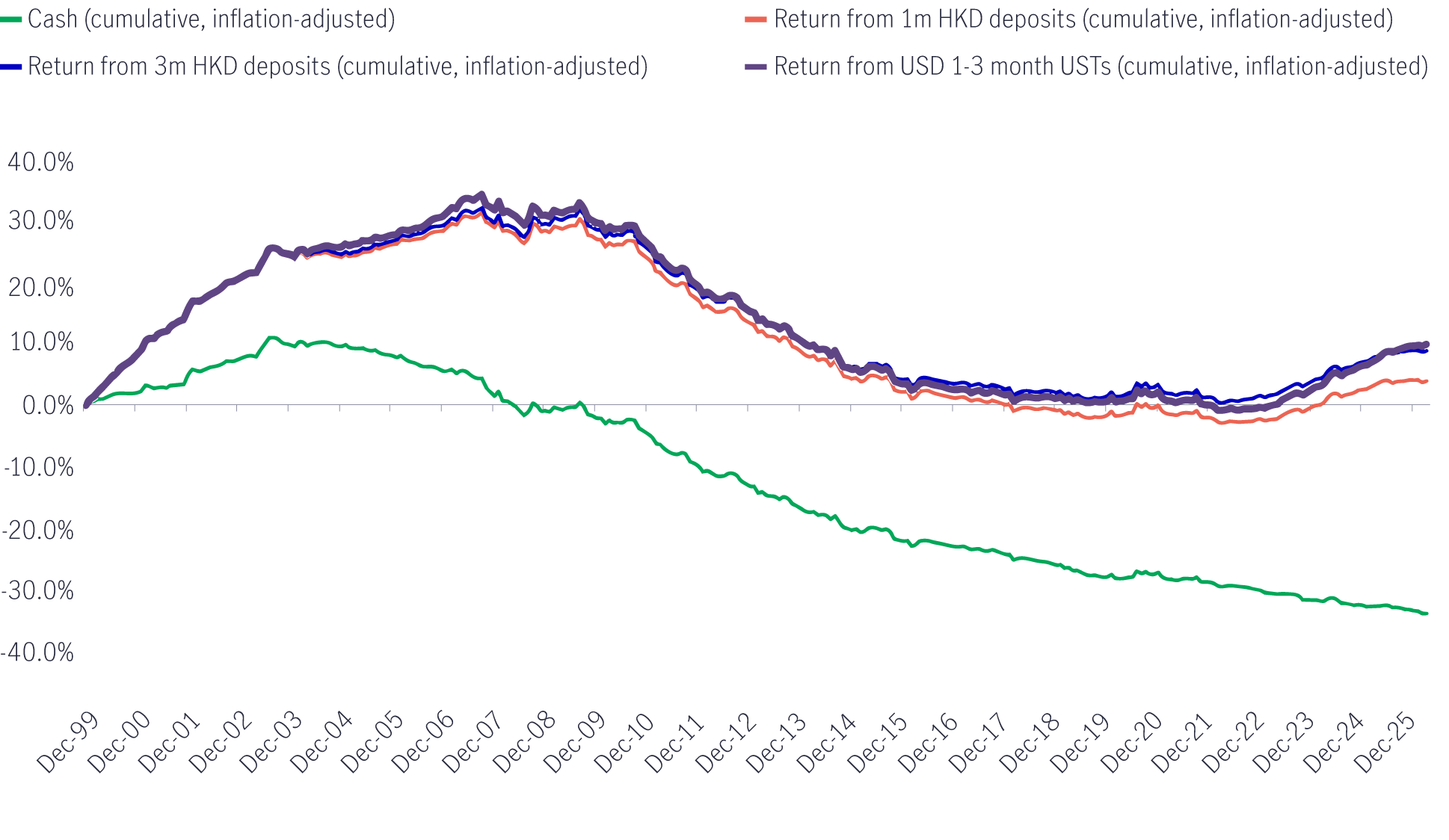

How have these investments performed over time versus holding cash?

Chart 1: Inflation-adjusted return (cumulative) from various short-term securities since 20001

Chart 1 shows that over the past 25 years, investing in short-term US Treasury Bills (one to three months) produced returns that were in line with, or slightly better than, short-term bank deposits, with the added benefit of instant liquidity (no lock-in periods).

More importantly, returns were able to at least keep up with inflation, on a cumulative basis. It should also be noted that the returns from short-term US Treasury bills are a conservative proxy for the money market securities and short-term bonds described above because corporate and financial debt, with lower credit ratings, typically offer higher interest rates.

With higher expected returns, investors may be concerned about the potential for greater risk. However, due to the short-term nature of these investments, as well as the quality of issuers, the risk of default is limited – for reference, the default rate on investment-grade debt with less than one year until maturity from 1981 to 2025 was only 0.08% . This low rate of default may even be overstated, as the figures include debt with slightly longer maturities than the instruments described above, which typically mature within a few months.

As Hongkongers know well: life is expensive. Additionally, Hong Kong boasts one of the longest life expectancies in the world: men live roughly 83 years, while women can expect to live almost 89 years. Many know that they risk outliving their assets (longevity risk) but may not know how to address it. Increasing one’s level of savings/investment into higher-yielding investments reduces the risk and turns it into a potential opportunity.

Indeed, an allocation to a mix of short-term USD deposits, money-market securities, and bonds may not only help put one’s money to work with the potential for higher returns, but also meaningfully contribute to funding a long, abundant retirement and life.

1 Source: Manulife Investment Management, Bloomberg, HK Census and Statistics Department, as of 31 March 2026. Chart interpretation: 0% represents that investment returns have kept up with inflation and that purchasing power has been maintained; a positive figure represents an increase in purchasing power over the time period, and vice-versa.

2 Standard and Poor’s ‘2025 Annual Global Corporate Default and Rating Transition Study’, as of 18 March 2026.

How to Set Smart and Effective Financial Goals

In previous episodes, we have explored creating a financial plan and establishing a budget that accounts for your current expenditure. The third step is to build a strategy that will help you accomplish either a short-term or a long-term financial goal. We will guide you on your path by providing financial goal examples and introducing SMART (specific, measurable, attainable, relevant, time-based) objectives that help clearly define what you want to achieve in the years ahead.

5 ways a budget plan can help you manage your finances

We all know approximately how much money we need each month. However, without a clear spending strategy, you could see a shortfall in savings, face a lack of day-to-day cash, or be caught off guard by unexpected costs. That’s why it’s important to have an effective budget plan that will give you control over your finances.

Risk Diversification

There is no free lunch. But Risk Diversification comes close in investing. A diversified portfolio was shown to optimize returns with lower volatility in the long run.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited