25 June 2026

Inflation: the unseen tax that gradually erodes investors’ purchasing power

Investors have faced a raft of challenges over the past five years: tariffs, energy shocks, the pandemic, and geopolitical uncertainties. Many of these events have not only amplified market volatility but also increased already-elevated inflationary pressures. Indeed, at the same time, the prices of essential services such as education and health care are projected to go up.

With rising uncertainty, some investors have increased their cash holdings as insurance, particularly in bank deposits. This response is normal: tucking cash away for potential future expenses is good financial management.

However, there is a hidden cost – inflation – if too much cash is put into low-rate deposits, it may deter longer-term retirement goals. The impact of inflation may not be evident immediately, given that it “only” averages around 1% to 2% annually, but the accumulation over a longer 20 to 30-year period may significantly reduce investors’ purchasing power.

Financial advisors generally recommend that people keep at least three to six months of expenses in cash in case of an emergency. Families with more children or greater financial responsibilities might want to consider a larger financial cushion: six to twelve months.

These recommendations, however, are usually associated with savings outside of a defined retirement portfolio. That is, assets not allocated specifically for retirement. Evidence suggests that some individuals may be holding significant cash reserves for use in their later years.

The 2025 Hong Kong Deposit Survey, commissioned by the Hong Kong Deposit Protection Board, found that survey respondents of all ages are saving more:

Further, Manulife’s Asia Care Survey in 2025 shows that survey respondents in Hong Kong, on average, hold roughly 50% of their total savings and investments in cash and cash equivalents.

Holding such large cash balances beyond lower returns can have significant downsides. Some banks offer less-than-attractive rates that change quickly, particularly when interest rates are falling. Additionally, long-term deposits are illiquid, and the depositor usually must pay a penalty to withdraw early.

With persistent inflation expected in the near term, investors may benefit from allocating their cash to other opportunities that offer liquidity and potentially greater protection against higher prices.

In particular, a blend of short-term USD deposits, money-market securities, and bonds may offer higher returns (to preserve and potentially enhance purchasing power) without significantly increasing risk. These opportunities include investments in government debt as well as in debt issued by large corporations or financial institutions.

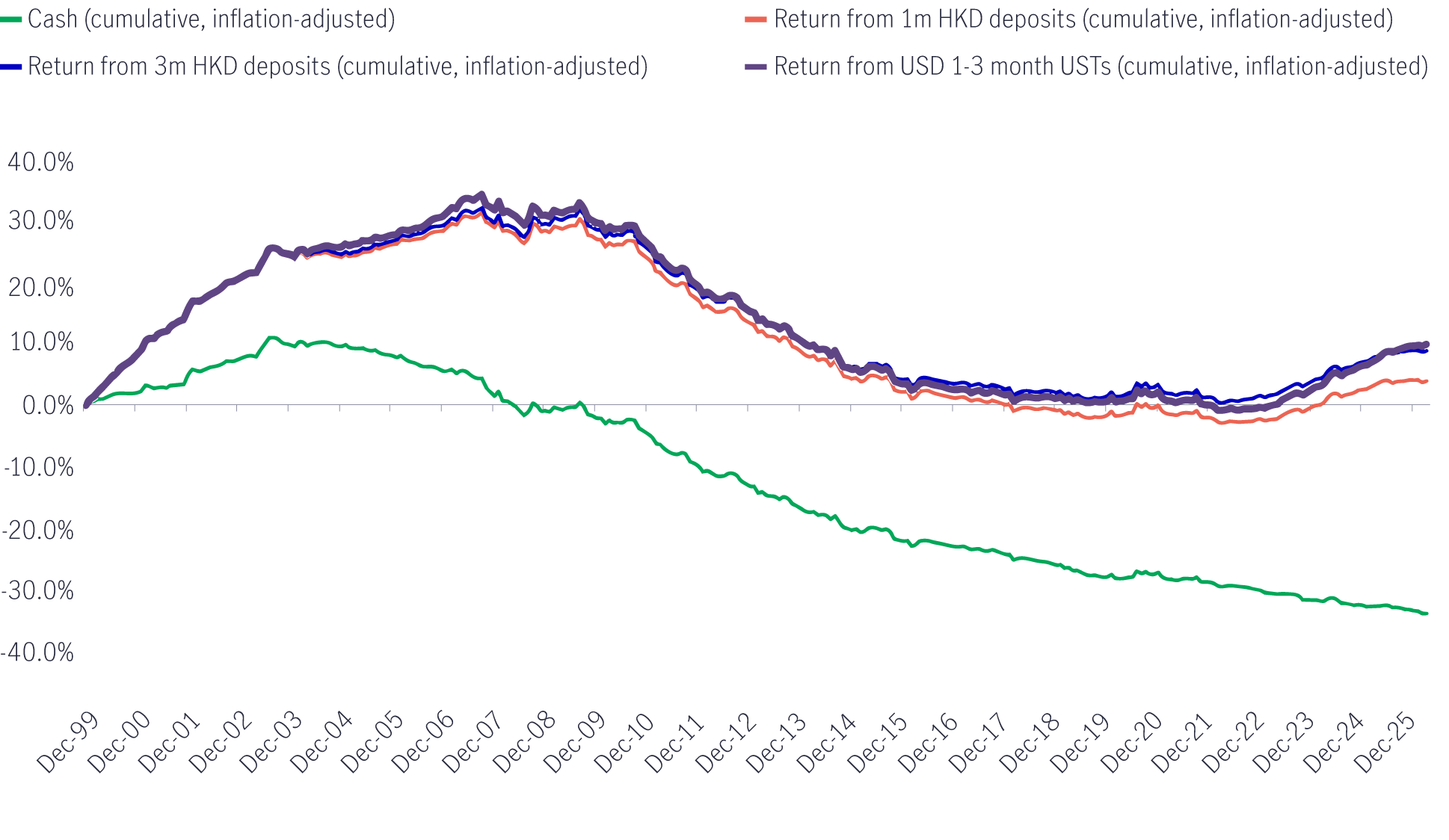

How have these investments performed over time versus holding cash?

Chart 1: Inflation-adjusted return (cumulative) from various short-term securities since 20001

Chart 1 shows that over the past 25 years, investing in short-term US Treasury Bills (one to three months) produced returns that were in line with, or slightly better than, short-term bank deposits, with the added benefit of instant liquidity (no lock-in periods).

More importantly, returns were able to at least keep up with inflation, on a cumulative basis. It should also be noted that the returns from short-term US Treasury bills are a conservative proxy for the money market securities and short-term bonds described above because corporate and financial debt, with lower credit ratings, typically offer higher interest rates.

With higher expected returns, investors may be concerned about the potential for greater risk. However, due to the short-term nature of these investments, as well as the quality of issuers, the risk of default is limited – for reference, the default rate on investment-grade debt with less than one year until maturity from 1981 to 2025 was only 0.08% . This low rate of default may even be overstated, as the figures include debt with slightly longer maturities than the instruments described above, which typically mature within a few months.

As Hongkongers know well: life is expensive. Additionally, Hong Kong boasts one of the longest life expectancies in the world: men live roughly 83 years, while women can expect to live almost 89 years. Many know that they risk outliving their assets (longevity risk) but may not know how to address it. Increasing one’s level of savings/investment into higher-yielding investments reduces the risk and turns it into a potential opportunity.

Indeed, an allocation to a mix of short-term USD deposits, money-market securities, and bonds may not only help put one’s money to work with the potential for higher returns, but also meaningfully contribute to funding a long, abundant retirement and life.

1 Source: Manulife Investment Management, Bloomberg, HK Census and Statistics Department, as of 31 March 2026. Chart interpretation: 0% represents that investment returns have kept up with inflation and that purchasing power has been maintained; a positive figure represents an increase in purchasing power over the time period, and vice-versa.

2 Standard and Poor’s ‘2025 Annual Global Corporate Default and Rating Transition Study’, as of 18 March 2026.

如何制定明智及有效的財務目標?

在之前的文章中,我們已探討過如何訂立自己的財務計劃,以及如何制定能反映你目前開支狀況的預算計劃。接下來的第三個步驟,是建立一套策略協助你實現短期或長期的財務目標。我們將透過實際的財務目標例子,並介紹「 SMART」 原則(具體、可衡量、可行、相關性、具時限),幫助你清晰地制定未來希望達成的財務目標。

認識5種預算計劃 助你管理個人財務

我們大概都清楚自己每個月需要花費幾多,但如果缺乏清晰的預算與消費策略,除了未能有效累積儲蓄,亦可能出現日常現金流不足的情況,甚至在面對突發開支時影響整體財務安排。因此,制定一個有效的預算計劃,對於掌控個人財務狀況至關重要。

分散投資:何謂多元化投資及其運作方式?

2026年下半年前景展望:大中華股票

2026年上半年,大中華股票市場表現個別發展。受惠於環球人工智能(AI)需求帶動科技產品出口表現強勁,中國A股及台灣加權指數錄得顯著升幅。另一方面,MSCI明晟中國指數出現回調,主要受外賣市場激烈競爭下商業補貼增加,以及AI資本開支上升所拖累,但我們認為相關因素已反映於市場價格中。在今次下半年展望中,我們將重點分析推動中國及香港股票市場於2026年下半年表現的五大利好因素。此外,投資團隊亦闡釋其看好台灣地區科技產業增長趨勢有望延續的原因。

2026年下半年前景展望:環球半導體

半導體產業作為全球經濟的重要推動力,持續為人工智能(AI)、雲端運算及電氣化等長期增長趨勢提供關鍵技術支援。正如我們早前的觀點中提及,半導體是一個由結構性需求及實質基建投資所驅動的完整生態系統。隨著行業於2026年上半年錄得亮麗表現,我們對後市展望仍然正面,認為在盈利增長強勁、資本投資持續增加,以及企業AI使用率仍處於起步階段的支持下,行業升勢有望延續至2026年下半年,並進一步推進至2027年。

2026年下半年前景展望:環球股票多元入息

在2026年上半年高度不確定的市場環境中,宏利環球股票多元入息(GEDI)基金(「本基金」)表現穩健 ,並展現出相對較低的波動性。此成果主要來自本基金的四大投資支柱,採取以收益為核心的策略,並在全球多元分散配置增長型、價值型及收益型股票。在《2026年下半年展望》中,亞洲區多元資產執行總監、客戶投資組合管理主管高沛樂闡釋了本基金的獨特架構,如何在市場周期中提供穩定收益及捕捉潛在上升潛力,並同時指出下半年值得關注的主要機遇與風險。

![]()