13 June 2023

Murray Collis, Chief Investment Officer, Fixed Income (Asia Ex-Japan)

Alvin Ong, Head of Fixed Income, Singapore

Esther Koon, Portfolio Manager, Asia Fixed Income

Over the past two years, surging inflation and rising interest rates have presented investors with challenges and opportunities. As the macro landscape evolves in 2023, many are looking for investment options to put their excess cash to work. In this investment note, Murray Collis, Chief Investment Officer, Fixed Income (Asia Ex-Japan), Alvin Ong, Head of Fixed Income, Singapore, and Esther Koon, Portfolio Manager, Asia Fixed Income, explain how short-duration Asian bonds can be an attractive option – offering a competitive yield, the potential for long-term capital appreciation, and a lower volatility profile relative to other fixed-income investments.

After a tumultuous 2022 punctuated by surging inflation and interest rates, we believe that fixed-income assets are nearing an inflection point.

Indeed, the US Federal Reserve (Fed) has raised the federal funds rate to a range of 5.00%-5.25% since March 2022, while 10-year US Treasuries have shown great volatility, rising roughly 225 basis points (bps) since the start of last year. As a result, fixed income posted negative returns in 2022, prompting many investors to place their excess cash in bank deposits to escape market volatility.

However, the global macro landscape is changing. Inflation in the US has gradually decelerated but remains high in 2023: from 6.4% (year-on-year) in January to 4.9% in April. Fed Chair Jerome Powell also recently stated that continued volatility in the nation’s banking sector might further tighten credit conditions, via lower lending levels, allowing the US central bank to halt rate increases at a lower level than previously envisaged.

While the Fed monetary tightening cycle might not be over, we believe that we are closer to the end of the cycle than we are to the beginning. Furthermore, the potential upcoming pivot in Fed policy offers opportunities for fixed-income investors.

Interest rates should remain higher over the short term due to sticky inflation that remains above the Fed’s target of 2%. Yet, significant additional rate hikes seem unlikely amid lower inflation, as well as first-quarter GDP and recent monthly retail sales data that suggest a decelerating US economy.

Thus, fixed-income investors have an attractive entry point: they receive current elevated yields, while also potentially benefitting long-term from capital appreciation if interest rates gradually move lower. In contrast, bank depositors may face reinvestment risk to achieve the same level of returns once their deposits mature after the Fed’s pivot.

With this changing macro backdrop in mind, investors would be well-served to understand how Asian short-duration investment-grade (IG) US-dollar bonds (USD bonds) can maximize opportunity in the current environment.

There are benefits to investing in Asian USD bonds. With our strategy primarily focusing on Asian short-duration (0-3 years) IG corporate bonds, we will explore the advantages of this bond category.

Credit risk can be mitigated by Asia’s stable macroeconomic environment: On the fundamental side, investors are rightly concerned about the credit quality of fixed-income investments in the current uncertain macroeconomic environment. We believe Asian USD bonds are arguably well positioned to navigate market volatility due to the region’s economic strength, which may help support corporate cash flows and profitability.

Indeed, the IMF recently upgraded its growth forecast for Asia-Pacific economies to 4.6% - the fastest rate among regions globally. Moreover, China and India are estimated to account for roughly 50% of global growth in 2023, while the region should compose around 70%. This should provide ample support for Asia’s corporates, particularly as China’s economic reopening may offer positive spillover effects to Asian economies in a varying degree, such as trade and tourism channels.

High-quality regional companies with deep market liquidity: We believe many high-quality regional companies choose the Asian USD bond market to reach international investors, diversify their borrowing portfolio, and tap deeper capital markets. Because these bonds are USD denominated, their market fundamentals are tied to generally more stable US interest-rate dynamics rather than local-currency markets.

Arguably, the asset class also boasts a high level of liquidity, particularly for emerging markets. Over the past five years, the USD bond market in Asia has surpassed USD 1 trillion1, making it one of the most liquid fixed-income markets globally.

A potentially lower volatility profile versus peers: Although emerging-market debt generally possesses a volatile risk profile, Asian USD bonds, especially short-duration IG bonds, may benefit from two factors that could dampen overall risk.

First, the emergence of a robust regional institutional investor base provides demand for USD bonds and a potential secondary cushion for prices during risk-off periods. Indeed, over the past ten years (2014-2022), regional investors accounted for roughly 70% of Asian USD bond allocation2 - the largest buying segment of the asset class.

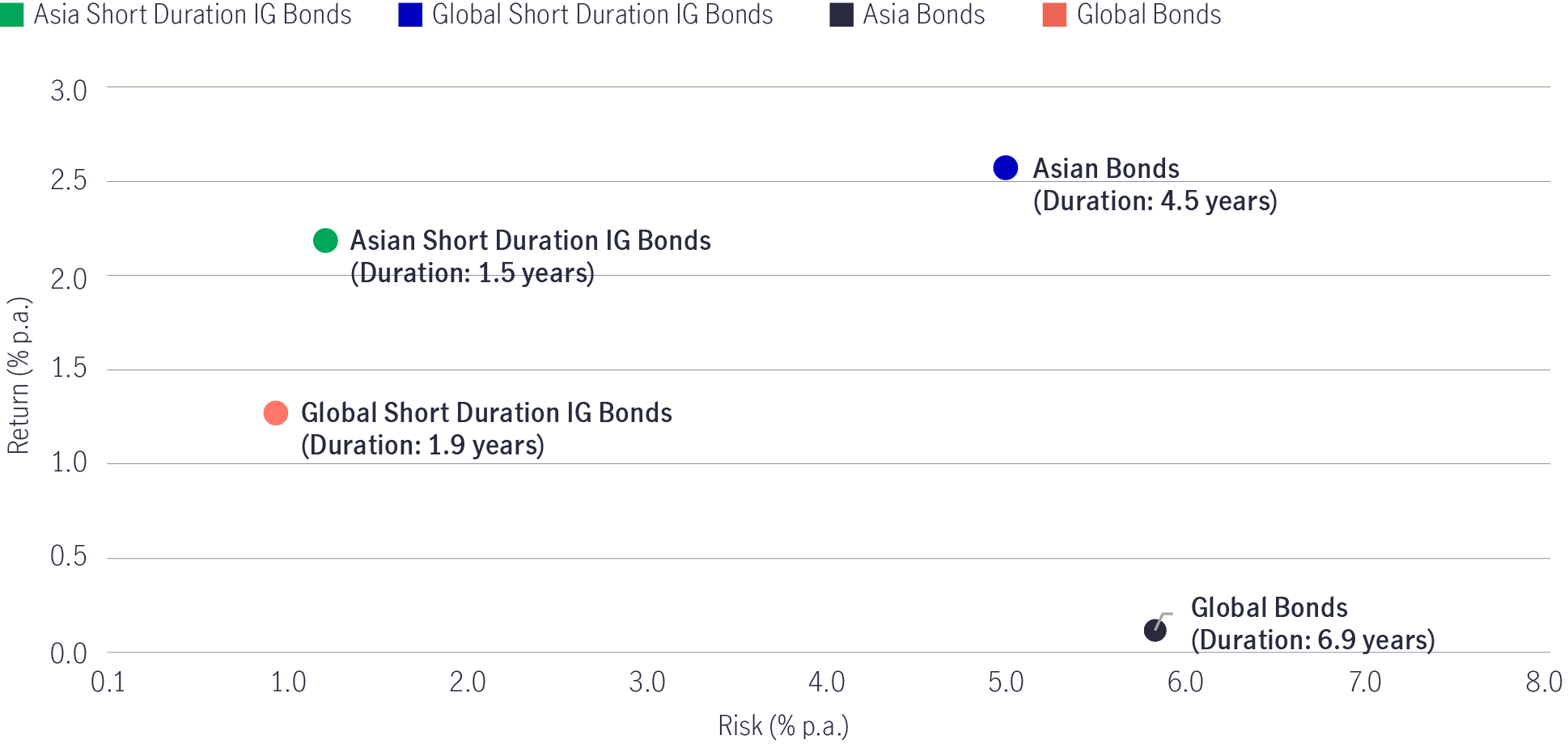

At the same time, if US Treasuries remain volatile due to Fed policy, the short-duration focus may make performance more resilient.

This is because shorter duration bonds are less sensitive to movements in interest rates. Asian short-duration IG USD bonds traditionally have a lower duration profile than the general Asian and global bond universes (see Chart 1). They also possess only marginally higher volatility (1.2% versus 0.9%) than global short duration IG bonds over the past decade.

Chart 1: Asian short-duration bond profile has dampened volatility over the past decade

Source: Bloomberg, as of 31 March 2023. Asian short duration IG bonds represented by JACI Investment Grade 1-3 Year Total Return Index. Global bonds represented by Bloomberg Barclays Global Aggregate Bond Index. Asian Bonds represented by JACI Composite Total Return Index. Global short duration IG bonds represented by Bloomberg Barclays Global Aggregate 1–3-year Bond Index. Past performance is not indicative of future results. It is not possible to invest directly in an index.

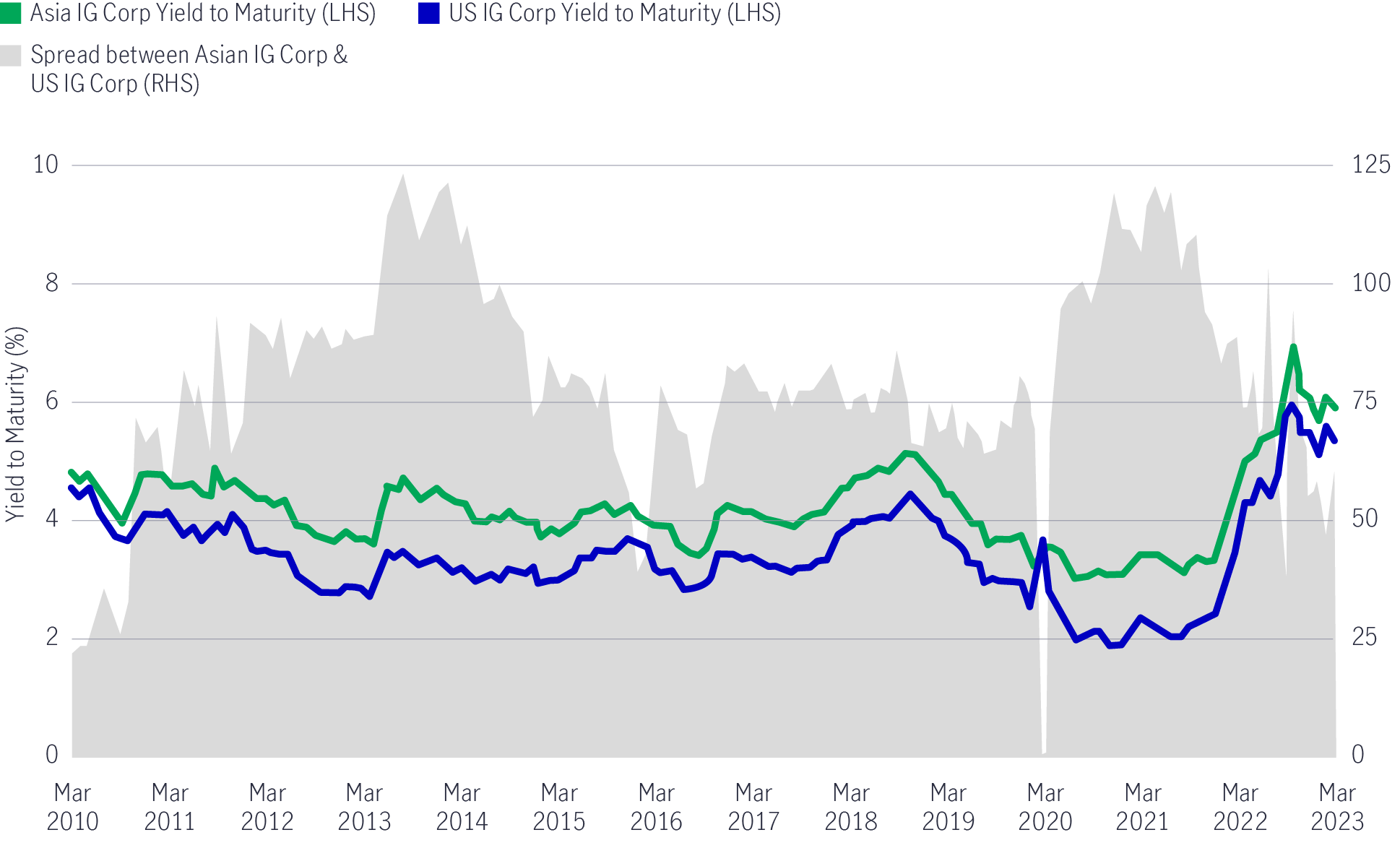

Historical comparable yield premium and attractive returns over peers: Historically, investors in Asian IG USD bonds have received a spread premium over those holding US IG corporate debt (see Chart 2). As of 31 March 2023, the premium was 60 bps, with an average over the past 10 years of 83 bps. The premium means that investors in Asian IG USD debt effectively receive a higher yield for holding companies with roughly the same credit profile and risk level as their peers.

Chart 2: Asian IG historical spread premium over US IG

Source: Bloomberg, BofA Merrill Lynch and JP Morgan indices. as of 31 March 2023.

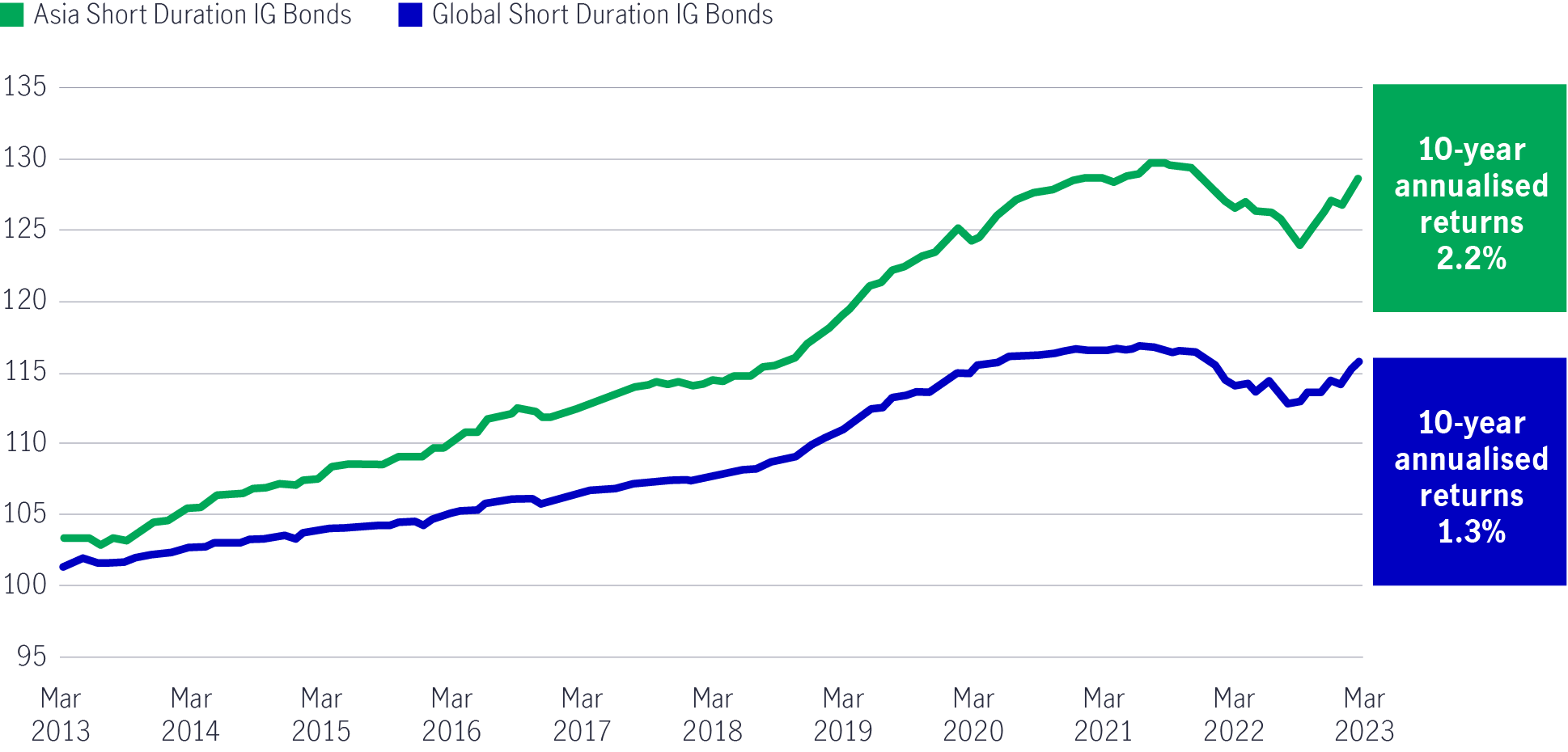

From an overall performance perspective, investors should not only pay attention to yield, but also to an asset class’s total return over time.

Versus global short-duration bonds: Asian short-duration IG bonds have outperformed their global peers on an annualised basis for the past decade (see Chart 3). This is supported by the relatively higher yields and coupons offered by Asian short-duration IG bonds compared to global corporates.

Versus bank deposits: While investors have utilised bank deposits over the past two years to shelter from market volatility, the Fed’s changing monetary policy stance may put this strategy at risk. Indeed, research indicates that current USD three-month (promotional) time deposits in Singapore earn roughly 3.7% versus a yield-to-maturity of 5.6% for Asian short-duration IG USD bonds3.

With the market’s expectation for a Fed pause in rates over the near-term and potential cuts over the longer term, investors may face significant reinvestment risk when deposits mature at potentially lower interest rates in the future.

Chart 3: Asian short-duration IG performance versus global peers

Source: Bloomberg, 30 June 2012 to 30 June 2022. Asian short duration IG bonds represented by JACI Investment Grade 1-3 Year Total Return Index. Global short duration IG bonds represented by Bloomberg Barclays Global Aggregate 1–3-year Bond Index (hedged USD). Past performance is not indicative of future results. It is not possible to invest directly in an index.

For the remainder of 2023, we are constructive on national champions and credits in China:

National champions: The significant percentage of state-owned enterprises (SOEs) is a unique feature of the Asian IG bond universe. SOEs tend to have more stable cash flows and market positions due to their ties to the government, while offering lower volatility at attractive yields. Also, new issuance activities from private national champions, such as the banks and electric vehicle battery producers, have picked up in 2023 providing further opportunities.

China credits: With China’s reopening continuing, we remain constructive on the country’s credits. While we do not expect a ‘V-shaped’ economic recovery, over time, we believe the country’s reopening should support domestic companies and those particularly in Southeast Asia, which could benefit from a pickup in trade and tourism activities.

Over the past two years, investors looking to earn returns on excess cash have primarily chosen bank deposits to escape market volatility. Moving forward, we believe that changes in the macro landscape, particularly a Fed policy pivot, may offer more profitable options.

Indeed, Asian short-duration IG USD bonds offer a competitive yield and may provide capital appreciation upside over the long term when rates gradually move lower. Coupled with a lower volatility profile and exposure to stable regional macroeconomic fundamentals, we believe investors should pay greater attention to the benefits of the asset class in the current market environment.

1 The USD $1 trillion market is primarily composed of investment-grade (84%) credits, but also includes high-yield (16%).

2 Manulife Investment Management Research.

3 Manulife Investment Management Research. Rate quoted applies to USD deposits exceeding USD 3 million. YTM taken from JACI IG 1-3 years Index as of 31 March 2023.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited