5/2/2026

Alvin Ong, Head of Singapore Fixed Income

Esther Koon, Portfolio Manager

Joshua Phoon, Portfolio Manager

Singapore bonds posted strong performance in 2025 amid a raft of global challenges on the back of structural inflows and sovereign strength. In this 2026 Outlook, the Singapore Fixed Income team outlines the underlying fundamentals and catalysts supporting positive momentum for the asset class in the new year and why the market is increasingly seen as a sanctuary for investors in uncertain times.

The Singapore bond market enters 2026 on a solid footing, having delivered robust returns in 2025 amid a complex global environment of elevated uncertainty.

The iBoxx Singapore index, which tracks the asset class, posted a strong gain of +7.65% (in Singapore Dollars) last year, reflecting resilient investor demand and the safe-haven status of Singapore bonds.

This positive momentum is expected to continue over the upcoming year, supported by structural inflows, sound sovereign fundamentals, and a dynamic credit landscape.

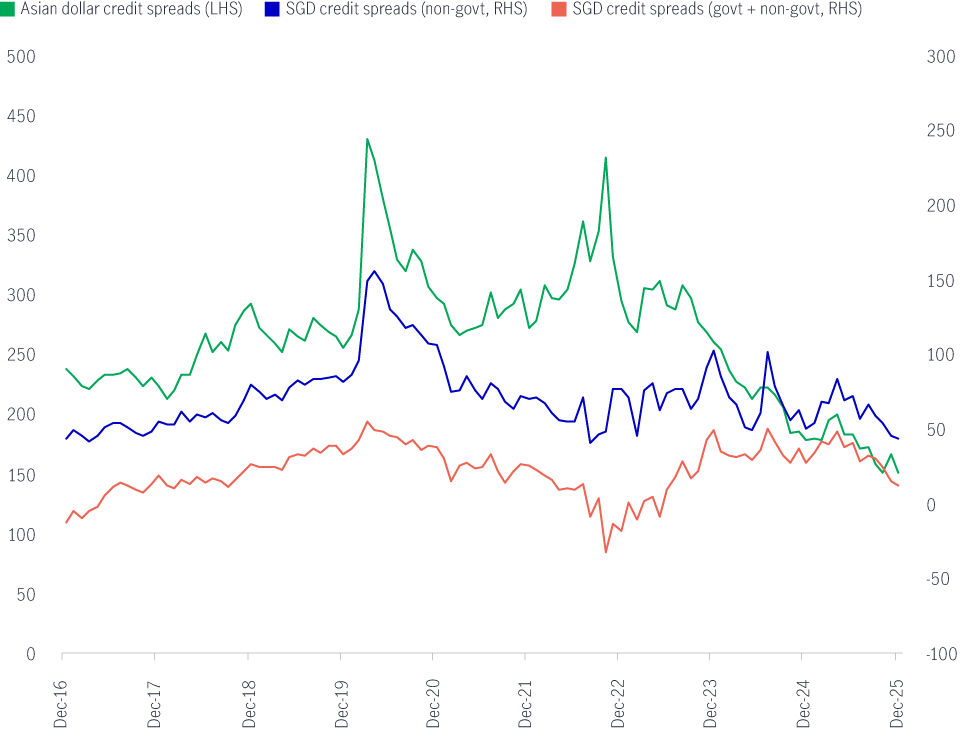

A key driver of recent performance has been the broad de-dollarisation trend, which has channelled significant inflows into Singapore Government Securities (SGS) and Singapore dollar credit throughout 2025.

The visibility and accessibility of the Singapore dollar bond market have increased as global investors seek diversification away from US dollar assets. This trend is likely to persist into 2026, sustaining demand for both SGS and local corporate bonds.

Singapore’s sovereign strength remains a cornerstone of market stability. The country is the only one in Asia to hold AAA ratings from all three major credit rating agencies—a distinction shared by only nine countries globally.

This gold-standard credit quality is underpinned by Singapore’s constitutional requirement for balanced budgets, which reinforces fiscal discipline and investor confidence. In addition, many high-quality Singapore corporates maintain close links to the sovereign and major local banks, underpinning the Singapore bond market’s resilience.

The Monetary Authority of Singapore (MAS) eased policy twice in 2025, responding to a global environment marked by shifting trade dynamics and increasing protectionist measures.

While Singapore’s growth exceeded expectations last year, growing 4.8% (year on year), export momentum is likely to moderate in 2026 as global trade faces new tariff threats. Nevertheless, Singapore’s resilient services segment and ongoing public sector projects should help cushion any negative impact. Capital expenditure on artificial intelligence is poised to support export growth and investment activity further.

Inflation in Singapore appears to be bottoming out. MAS has recently revised its headline and core inflation forecasts to 1.0-2.0%, from the previous range of 0.5-1.5%. However, core inflation is still projected to remain slightly below trend in 2026.

MAS is likely to retain its appreciating policy stance for now, though additional tightening remains possible if growth or inflation surprises to the upside.

Front-end rates such as SORA (Singapore Overnight Rate Average) declined sharply in 2025, driven by US Federal Reserve (Fed) rate cuts and abundant liquidity.

This spillover effect benefited the broader SGS curve, with SGS outperforming US Treasuries over the past year. Accommodative liquidity conditions are expected to persist over the forthcoming year, acting as a natural hedge against sharp rises in SGS yields and supporting Singapore’s safe-haven appeal. Continued capital inflows should help keep domestic interest rates low.

Nevertheless, we see less scope for SGS to outperform US Treasuries further in 2026. Current valuations make US Treasuries relatively attractive, though Singapore investors should consider the high cost of currency hedging when expressing this view.

While the rate differential between SGS and US Treasuries has narrowed, it remains wide by historical standards, suggesting only modest potential for further SGS gains. The cost of currency hedging is likely to decline gradually as US front-end rates fall in response to ongoing Fed easing.

As developed fixed-income markets experience potential steepening pressures amid deteriorating fiscal and budget dynamics, we believe investors are likely to rotate toward sovereign markets with stronger macro fundamentals, including SGS.

In contrast with other markets, steepening pressure on the long end of the SGS curve is likely to be contained in 2026. The regular issuance calendar does not include a 50-year bond, and only one 30-year bond is scheduled for issuance in the first quarter of the new year.

Overall, the duration or average maturity of SGS new issues will be reduced relative to 2025, which should support the longer end of the curve. Notably, a new 20-year green SGS is planned for issuance in the second half of 2026 via syndication, further supporting Singapore’s leadership in sustainable finance.

As cash rates decline, investors will likely need to move away from cash and short-dated instruments into longer-duration credit to achieve higher-yielding portfolios.

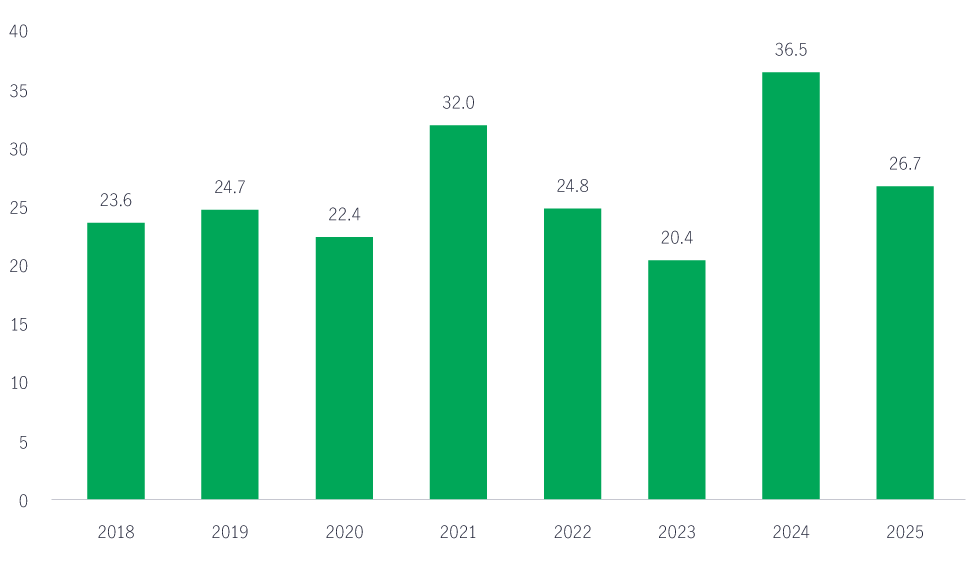

The Singapore dollar credit market is expected to remain well-supported in 2026, underpinned by strong market technicals—robust investor demand and limited new supply.

Recently, MAS provided clarity regarding the treatment of Singapore AT1 (Additional Tier 1) and Tier 2 bank and insurance papers and has decided against a more punitive approach that would restrict retail investors’ exposure to such instruments.

These clarifications have removed uncertainty, which should benefit the financial sector. High-quality, sovereign-linked issuers of SGD credit are expected to provide stable carry, while foreign issuers may offer pockets of alpha-generation opportunities through new issue concessions and yield enhancements.

Further, sustainability-related issuance of SGD corporate bonds is projected to rise, reflecting growing demand for sustainable finance and strong domestic policy support. The increasing ease with which global issuers can tap the SGD market for funding also broadens the investment universe and enhances market liquidity.

Chart 1: Credit spread of SGD bonds versus Asian dollar bonds1

Chart 2: Historical SGD bond issuance (SGD bn)2

While the outlook for the Singapore bond market remains constructive, investors should remain vigilant for signs of liquidity withdrawal, particularly if economic growth and inflation exceed expectations.

Such developments could put selling pressure on SGS and Singapore dollar credit. Additionally, global policy uncertainty—especially around US fiscal and trade policies—may continue to influence investor sentiment and contribute to market volatility.

That said, a combination of sovereign strength, robust technicals, and increasing sustainability-related issuance positions the Singapore bond market as a compelling choice for investors seeking stability, diversification, and sustainable income in 2026 amid heightened uncertainty in global markets.

1 Source: Bloomberg, as of December 31, 2025.

2 Source: Bloomberg, as of December 31, 2025.

2026年下半年前景展望:大中華股票

2026年上半年,大中華股票市場表現個別發展。受惠於環球人工智能(AI)需求帶動科技產品出口表現強勁,中國A股及台灣加權指數錄得顯著升幅。另一方面,MSCI明晟中國指數出現回調,主要受外賣市場激烈競爭下商業補貼增加,以及AI資本開支上升所拖累,但我們認為相關因素已反映於市場價格中。在今次下半年展望中,我們將重點分析推動中國及香港股票市場於2026年下半年表現的五大利好因素。此外,投資團隊亦闡釋其看好台灣地區科技產業增長趨勢有望延續的原因。

2026年下半年前景展望:環球半導體

半導體產業作為全球經濟的重要推動力,持續為人工智能(AI)、雲端運算及電氣化等長期增長趨勢提供關鍵技術支援。正如我們早前的觀點中提及,半導體是一個由結構性需求及實質基建投資所驅動的完整生態系統。隨著行業於2026年上半年錄得亮麗表現,我們對後市展望仍然正面,認為在盈利增長強勁、資本投資持續增加,以及企業AI使用率仍處於起步階段的支持下,行業升勢有望延續至2026年下半年,並進一步推進至2027年。

2026年下半年前景展望:環球股票多元入息

在2026年上半年高度不確定的市場環境中,宏利環球股票多元入息(GEDI)基金(「本基金」)表現穩健 ,並展現出相對較低的波動性。此成果主要來自本基金的四大投資支柱,採取以收益為核心的策略,並在全球多元分散配置增長型、價值型及收益型股票。在《2026年下半年展望》中,亞洲區多元資產執行總監、客戶投資組合管理主管高沛樂闡釋了本基金的獨特架構,如何在市場周期中提供穩定收益及捕捉潛在上升潛力,並同時指出下半年值得關注的主要機遇與風險。

2026年下半年前景展望:大中華股票

2026年上半年,大中華股票市場表現個別發展。受惠於環球人工智能(AI)需求帶動科技產品出口表現強勁,中國A股及台灣加權指數錄得顯著升幅。另一方面,MSCI明晟中國指數出現回調,主要受外賣市場激烈競爭下商業補貼增加,以及AI資本開支上升所拖累,但我們認為相關因素已反映於市場價格中。在今次下半年展望中,我們將重點分析推動中國及香港股票市場於2026年下半年表現的五大利好因素。此外,投資團隊亦闡釋其看好台灣地區科技產業增長趨勢有望延續的原因。

2026年下半年前景展望:環球半導體

半導體產業作為全球經濟的重要推動力,持續為人工智能(AI)、雲端運算及電氣化等長期增長趨勢提供關鍵技術支援。正如我們早前的觀點中提及,半導體是一個由結構性需求及實質基建投資所驅動的完整生態系統。隨著行業於2026年上半年錄得亮麗表現,我們對後市展望仍然正面,認為在盈利增長強勁、資本投資持續增加,以及企業AI使用率仍處於起步階段的支持下,行業升勢有望延續至2026年下半年,並進一步推進至2027年。

2026年下半年前景展望:環球股票多元入息

在2026年上半年高度不確定的市場環境中,宏利環球股票多元入息(GEDI)基金(「本基金」)表現穩健 ,並展現出相對較低的波動性。此成果主要來自本基金的四大投資支柱,採取以收益為核心的策略,並在全球多元分散配置增長型、價值型及收益型股票。在《2026年下半年展望》中,亞洲區多元資產執行總監、客戶投資組合管理主管高沛樂闡釋了本基金的獨特架構,如何在市場周期中提供穩定收益及捕捉潛在上升潛力,並同時指出下半年值得關注的主要機遇與風險。

![]()