23 January 2025

Murray Collis, Chief Investment Officer, Fixed Income (Asia ex-Japan)

Following the decline in Asian dollar-bond issuance in recent years due to the higher funding cost environment -- in addition to net redemptions -- investors have started to consider the broader Asia-Pacific dollar-bond market, which includes markets such as Japan and Australia.

Historically, Asia-Pacific dollar bonds (Asia-Pacific bonds) have been an excellent diversifier and can greatly reduce overall portfolio volatility. Given their emphasis on providing stable income and the generally higher quality of companies issuing bonds, Asia-Pacific bonds have produced attractive returns (4.5% p.a. since Oct. 2005) with relatively low volatility (5.0% p.a. standard deviation) compared with Asia-Pacific equities, which returned 5.4% p.a. but with a much higher volatility of 16.4% p.a. over the same period.

Similarly, if we look at the maximum drawdown (i.e. the maximum loss from a peak to a trough) for both asset classes over this period, the worst drawdown for Asia-Pacific bonds was -17.3%, which occurred in October 2022 due to the combined effects of a spike in US interest rates while credit spreads widened due to defaults in the China property space. Asia-Pacific equities experienced its worst drawdown of -54.5% in February 2009 as global risk assets sold off dramatically due to the global financial crisis.

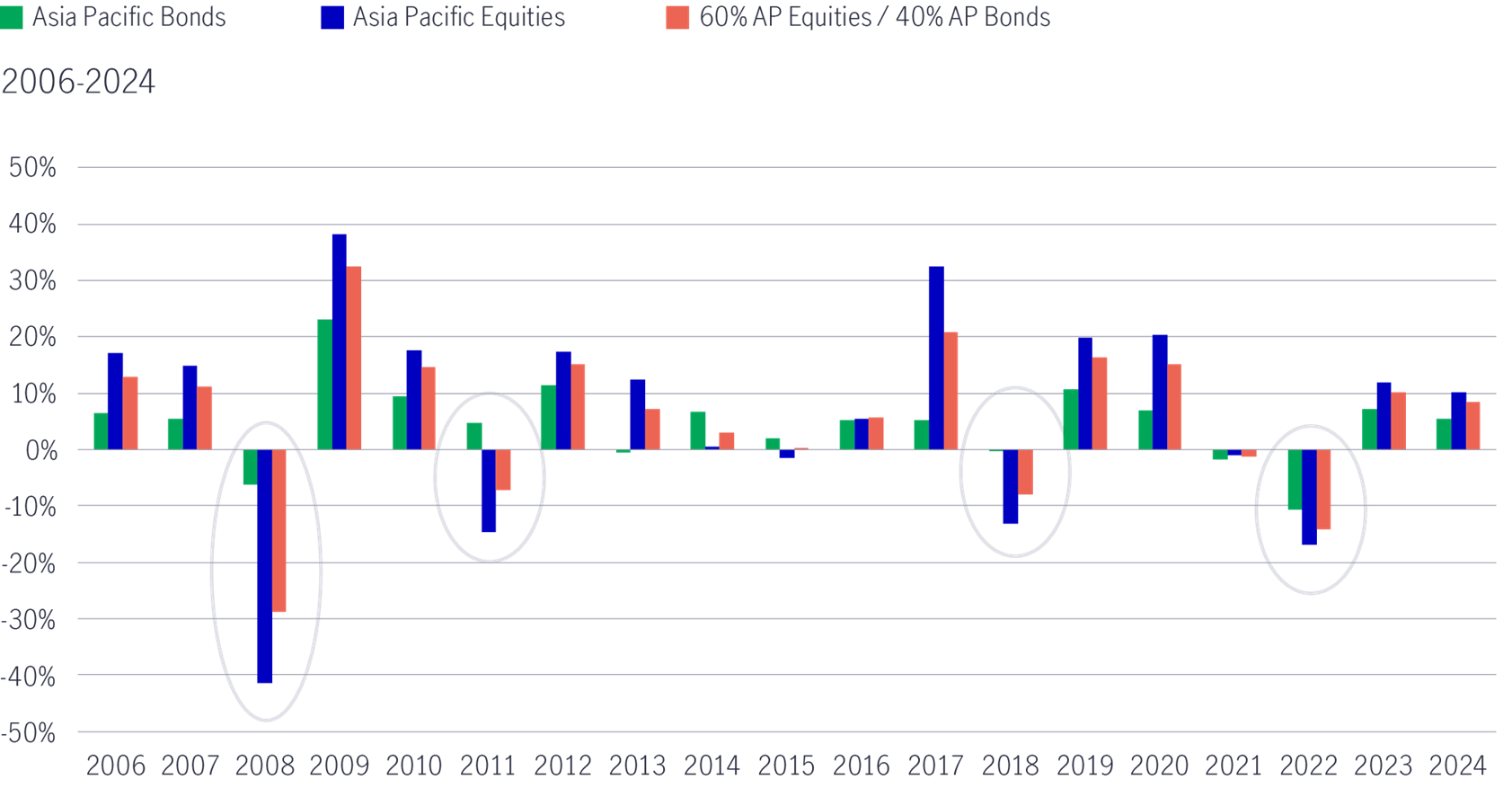

Looking at calendar year returns since 2006, Asia-Pacific bonds only experienced one year where returns were below -10% compared with Asian equities, which experienced returns below -10% four times. Again, to emphasise the crucial role bonds play in providing stable income and acting as a diversifier to reduce overall portfolio volatility, a diversified portfolio comprising 60% Asia-Pacific equities and 40% Asia-Pacific bonds would have produced annual returns of 5.3% p.a. and a much lower standard deviation of 11.2% p.a. (compared with Asia-Pacific equities which had a total return of 5.4% p.a. and a standard deviation of 16.4% p.a.) over the period from October 2005 to December 2024. The 60/40 portfolio experienced a much lower maximum drawdown of -38.2% and experienced two calendar years of returns below -10% compared with the maximum drawdown of -54.5% and four calendar year returns below -10% for Asia-Pacific equities.

As the global economy enters a period of increased uncertainty due to potential changes in trade policy and US equity markets see much richer valuations, Asia-Pacific bonds have a clear role to play in adding stability and reducing overall risk in investment portfolios.

Chart 1: Returns comparison among Asia Pacific Bonds, Asia Pacific Equities and a 60/40 portfolio

Source: Manulife Investment Management, Bloomberg as of 31 December 2024.

Chart 2: Adding Asia Pacific Bonds could significantly reduce portfolio risk

Source: Manulife Investment Management, Bloomberg as of 31 December 2024.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited