1 March, 2021

Sue Trinh, Senior Macro Strategist

Global stock markets corrected last week (as of 26 February) as the 10-year US Treasury yield climbed to its highest level since February 20201. The rise unnerved investors who fear that higher inflation will spur an-earlier-than-indicated rate hike from the US Federal Reserve (the Fed). In this note, we share our thoughts on rising bond yields, global liquidity, and the implication for equities.

Market focus has concentrated on rising bond yields and fears that higher inflation will spur the Fed to raise interest rates. However, as our Chief Economist Frances Donald mentioned in her earlier note, we believe that markets have been overemphasising the inflation aspect of the Fed's mandate. This is why we are skeptical that the US central bank will taper its quantitative-easing measures any time soon. Indeed, in our view, the employment side of the mandate will restrain the tapering conversation until at least the third quarter.

It’s also worth noting that although the Fed has signaled it’s unlikely to add any additional easing aimed at the real economy, the Bank of England, the European Central Bank, and the Bank of Canada have all made it clear that rate cuts remain on the table. While we don’t expect these central banks to cut rates, we believe that relative monetary policy divergences between the Fed and other major central banks are only going to get wider. The one exception here being the People’s Bank of China, which is in tightening mode.

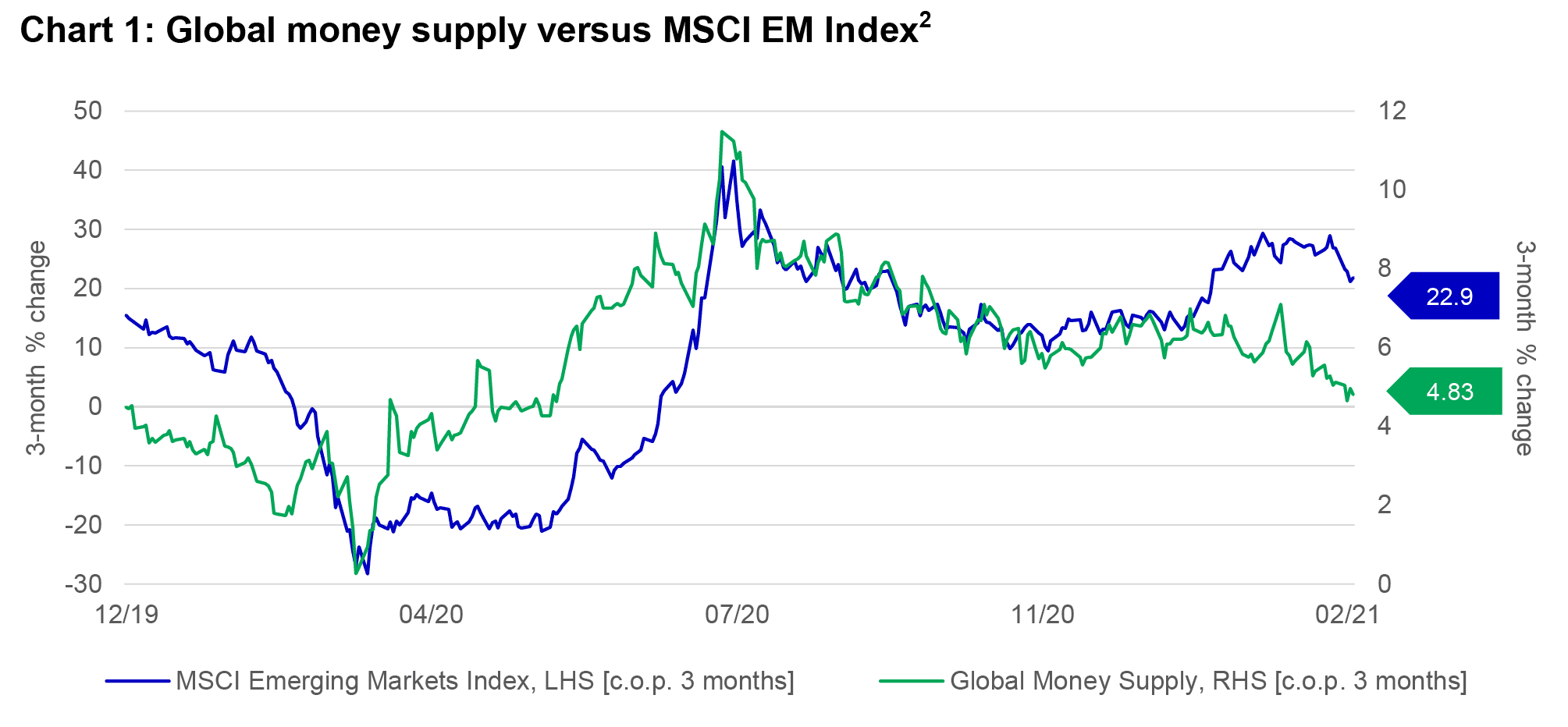

That said, we have been closely watching the slowdown in global liquidity growth. In level terms, global liquidity (proxied by global money supply) has topped out in 2021, flat-lining around US$96 trillion year-to-date . Importantly, the growth in global liquidity has slowed markedly, from 40%+ to 4.8% on a three-month percentage-change basis, with slowing balance-sheet expansion from the Fed and the People’s Bank of China (PBOC), as the major drivers of this dynamic.

Chart 1 shows the three-month growth in global liquidity (green line) against the three-month change in MSCI EM equities. In our view, the chart has been flashing a warning sign in that EM equities had become overextended relative to global liquidity growth.

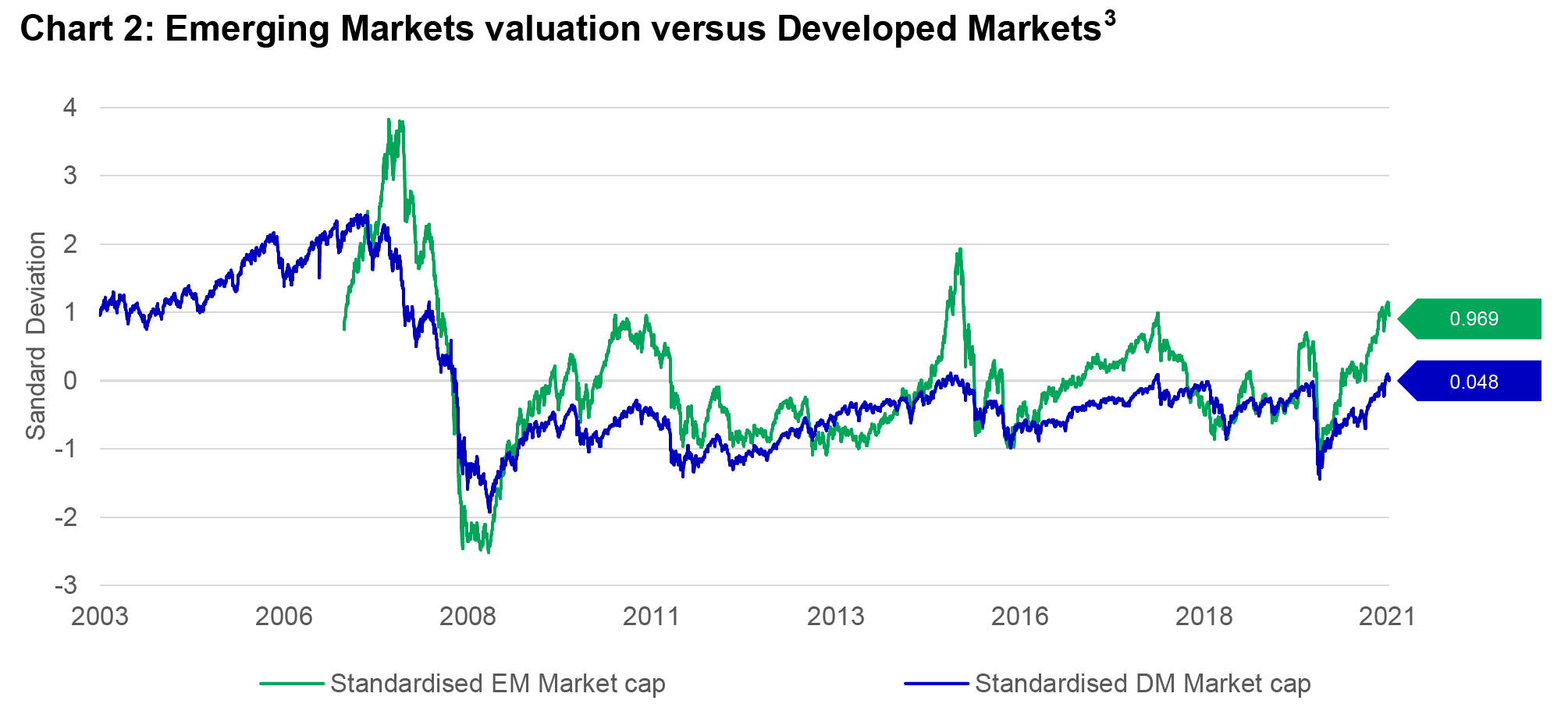

This is corroborated by Chart 2, where we adjust and normalise the market capitalisation of developed markets (DM) and EM equities for global liquidity. By this metric, the market cap of EM is running over 1 standard deviation above its long-term average. In contrast, the market cap of DM is not stretched.

Taken together, this suggests that after the recent strong price recovery, EM may be stretched vis-à-vis DM. At the very least, it implies near-term consolidation. Longer-term, we remain bullish on EM equities, particularly in Asia, and would view any correction as an opportunity. Meanwhile, on a global basis, the largest central banks have likely hit peak liquidity. In our view, the respective biases of the various major central banks strengthen our belief that the US dollar could experience some countertrend rallies in the short term, which tend to be supportive of US equities.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

1 Bloomberg, as of 26 February 2021.

2 Bloomberg, Macrobond, Manulife Investment Management, as of 25 February 2021.

3 Bloomberg, Macrobond, Manulife Investment Management, as of 26 February 2021.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited