22 November, 2019

John Addeo, Chief Investment Officer, Global Fixed Income

After a decade of expansion following the Global Financial Crisis, the global economy once again finds itself at a pivotal moment. Facing a convergence of macroeconomic headwinds, growth is forecast to moderate over the next few years, with some economies potentially facing recession. Despite negative headlines, we still hold a positive bias towards risk assets, given the increasing commitment among central banks and governments to support growth and corporate earnings.

Several market headwinds are worth paying attention to – some are geopolitical, and others are fundamental changes in the growth profile. The trend in Europe, for example, is towards slower growth, while parts of Asia are being affected by the trade war. We still see positive growth in the US, and our view is that the general global trend will remain positive, although we are concerned that this trend may be slowing, which exposes us to the risk of shocks.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

In response to the threat of a slowdown, some central banks have again adopted a more accommodative monetary stance. The US Federal Reserve (Fed) retreated by cutting rates after nine increases between 2015 and 20181. The European Central Bank decided to reignite its QE programme less than a year after pausing it2 . The Bank of Japan reminded investors that its negative-rate policy could go beyond the current -0.1%3. The People’s Bank of China retained its policy benchmark rate at the 2015 level, but cut the Reserve Requirement Ratio to its lowest point since 20074.

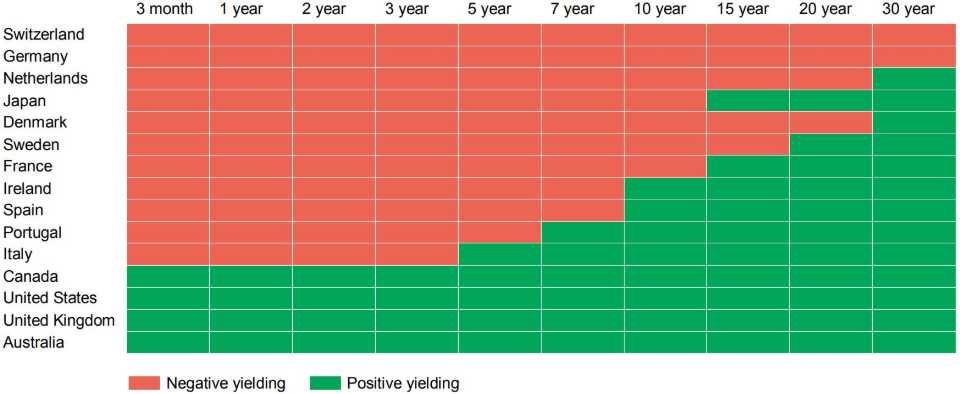

Further cuts to benchmark interest rates, and the anticipation of additional eductions have pushed an even greater share of developed-market sovereign bond yields into negative territory (Chart 1), which is likely to create a variety of long-term distortions. In the immediate term, however, increasingly low and negative rates imply that the search for yield will continue to be a dominant theme for income investors.

From a monetary-policy perspective, the “lower for longer” interest-rate environment means that it will become more difficult for central banks to stimulate economic growth by reducing rates. Quantitative measures could be utilised, but it is unlikely that central banks will want to follow that path again so soon. The risk with low rates is that they create a bubble environment and central banks have to balance this risk with a slowing underlying economy.

Source: Refinitiv Datastream, Manulife Investment Management, as of 19 September 2019.

In this low-rate environment, we believe that credit could be a bright spot: default rates remain low5, which is where we expect them to remain over the next 12 months, and the asset class is trending positively in a low-growth environment. Companies that continue to generate positive earnings and respective cashflows can reduce their debt burdens and enhance liquidity. Meanwhile, investors could see spreads over underlying government rates deliver rewarding income returns. We believe that income-generating strategies could perform well in this environment.

1 US Federal Reserve, as of September 2019.

2 Bloomberg, 12 September 2019: “ECB Cuts Rates, Revives QE to Lift Growth as Draghi Era Ends”.

3 Nikkei Asian Review, 9 September 2019: “Bank of Japan's “deeper” negative rates would hit consumers.”

4 Bloomberg, 6 September 2019: “China Ratchets Up Stimulus, Cutting Reserve Ratio to Lowest Level Since 2007.”

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited