10 October 2023

Murray Collis, Chief Investment Officer, Fixed Income (Asia Ex-Japan)

On 21 September 2023, JPMorgan announced that Indian government bonds would be included in the company’s Government Bond Index-Emerging Markets (GBI-EM) Global index suite starting in June 2024. In this investment note, Murray Collis, Chief Investment Officer, Fixed Income (Asia Ex-Japan), examines the short- and long-term implications of this significant decision for the Indian bond market, including how it could attract greater foreign investment and may bolster the country’s long-term position in Asia’s fixed-income universe.

After several years of reform, it has now been confirmed that India will be included in the JPMorgan GBI-EM Global index suite starting in June 2024, representing a significant milestone in the development of the Indian bond market.

This comes after India was placed on ‘watch positive’ for index inclusion in 2021 after the Indian government announced the removal of restrictions for foreign investors in the sovereign bond market in 2020. JPMorgan’s recent decision also considered investors’ opinions that India’s inclusion would result in a more diverse and representative index by reducing concentration among greater-weighted countries.

As a result, starting in June 2024, India will join the flagship JPMorgan GBI-EM Global Diversified index with a 1% weight. At this point, only FAR (Fully Accessible Route)- designated Indian government bonds with a notional value of US$1 billion or more and at least a remaining maturity of 2.5 years will be allowed to join the index1. Currently, 23 bonds with a notional bond value of US$330 billion are eligible for the index.

Over time, the country’s weight will increase by one percentage point each month until it reaches its final index weighting of 10% in April 2025, on par with China and Indonesia, the largest expected country weights of the revised index.

After full inclusion, India will be the second biggest EM country in the index after China. Asia will compose roughly 50 percent of the index. Overall, inclusion gives investors access to the second-largest bond market and the highest-yielding market in the region.

Over the short term, inclusion is expected to increase passive capital flows linked to the index significantly.

Roughly US$236 billion of global funds is benchmarked to the GBI-EM Global index suite. Once inclusion starts, inflows into the country’s government bonds are expected to total around US$30 billion, or US$3 billion per month, until India reaches its final weight2. Related buying should be most supportive for the long end of the curve with maturities greater than five years.

From a macro perspective, increased capital inflows should help narrow the country’s marginal current account deficit (-0.2% of GDP- Q1 2023) or even flip it into surplus, which should support the rupee.

The initial response from the market to the index inclusion news has been positive: Indian bonds have outperformed other Asian local markets month to date by around 10-15 basis points3.

Over the longer term, the implications should be more transformative, including greater foreign investor participation while the government bond market and the Indian bond asset class continues to develop and mature structurally.

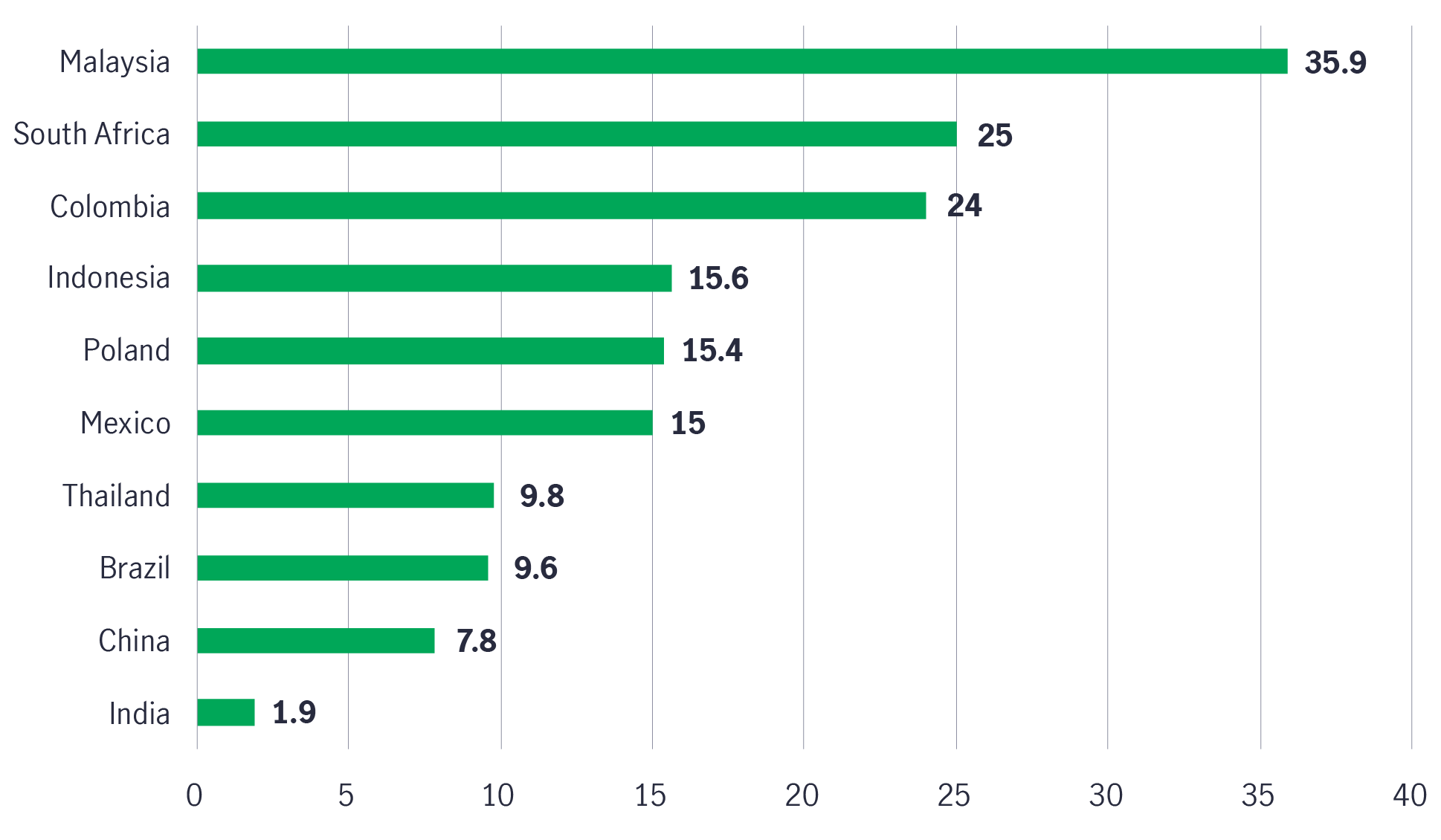

Around 1.9% of the country’s government bond market is currently owned by foreign investors (Chart 1), significantly below other emerging markets, particularly when accounting for India’s economic size as the world’s fifth-largest economy.

Chart 1: Foreign ownership of government bonds in key emerging markets (%)4

JPMorgan’s decision may also spur further foreign investment through knock-on effects and the inclusion of Indian government bonds in other major global sovereign bond indices:

The impact of greater foreign investment could lead to numerous structural changes in the government bond market, such as an increase in the number of potential buyers, a potential improvement in overall market liquidity, and a central government that may be more fiscally prudent due to greater external scrutiny.

Ultimately, the potential benefit for foreign investors is that index inclusion will garner more attention and raise the profile of the high-yielding bond market of the world’s fifth-largest economy.

The inclusion also does not come without long-term risks, as India remains an emerging market. Most prominently, substantial inflows into the government bond market may lead the Reserve Bank of India or the government to smooth out its market impact via intervention. Furthermore, it could result in the government increasing net market borrowing and will likely subject the local bond market to greater exposure to changes in global financial conditions.

Investors should remain vigilant and seek out fund managers with experience in the burgeoning but volatile Indian bond market.

Manulife Investment Management has been investing in onshore Indian bonds in its flagship pan-Asian fixed income strategy since 2016.

In 2020, Manulife Investment Management also created a joint venture (JV) with Mahindra Finance in India6. As one of the few global financial institutions with a presence in India, the JV gives us a distinctive onshore presence with an experienced team of fixed income portfolio managers, analysts, and traders to leverage local market insights and analysis into informed investment decisions.

Having on-the-ground expertise and extensive experience investing in India gives us an edge navigating access to the onshore market on behalf of foreign investors as structural barriers around administrative and settlement-related issues remain for now.

We believe JPMorgan’s index inclusion decision is a welcome first step for India’s fixed income market to attract greater international attention and foreign investment. Indeed, not only should it help bolster India’s already robust macro credentials over the short-term, but also assist the government bond market’s development over the long-term.

With the inclusion of Indian government bonds in other major global bond indices over time, the market should gradually become a key one to watch in Asia’s fixed income universe.

1 JPMorgan report issued on 21 September 2023.

2 JPMorgan report issued on 21 September 2023.

3 Bloomberg, as of 28 September 2023.

4 Morgan Stanley report, as of 22 September 2023.

5 Bloomberg, 22 September 2023.

6 On 29 April 2020, Mahindra & Mahindra Financial Services Limited (Mahindra Finance) completed the proceedings for divestment of 49 percent stake in its wholly-owned subsidiary, Mahindra Asset Management Company Private Limited (Mahindra AMC), to Manulife, a leading global financial services group. Manulife has invested US$ 35 million (~INR 265 crore) in the 51:49 joint venture, which aims to expand its fund offerings, drive fund penetration, and achieve long term wealth creation in India. https://www.manulife.com/en/news/manulife-investment-management-acquires-49-percent-in-mahindra-asset-management.html.

Key takeaways from Chinese mainland NPC meeting

The annual meeting of Chinese mainland’s National People’s Congress (NPC) is concluding this week. The China equity team shares its latest views on key policy developments and analyses the main growth engines supporting high quality growth.

Latest asset allocation views amid latest Middle East developments

Against a backdrop of elevated uncertainty, the Multi Asset Strategy Team (MAST) summarizes key market moves, and the potential cross-asset implications.

Middle East developments - Implications for Asian equities and fixed income

The Asian Equities and Asian Fixed Income team assess the recent Middle East developments and implications for Asia asset classes.

Key takeaways from Chinese mainland NPC meeting

The annual meeting of Chinese mainland’s National People’s Congress (NPC) is concluding this week. The China equity team shares its latest views on key policy developments and analyses the main growth engines supporting high quality growth.

Latest asset allocation views amid latest Middle East developments

Against a backdrop of elevated uncertainty, the Multi Asset Strategy Team (MAST) summarizes key market moves, and the potential cross-asset implications.

Middle East developments - Implications for Asian equities and fixed income

The Asian Equities and Asian Fixed Income team assess the recent Middle East developments and implications for Asia asset classes.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited