16 December 2021

Paula Chan, Senior Portfolio Manager, Fixed Income

Isaac Meng, Portfolio Manager, Fixed Income

In this 2022 outlook, Paula Chan, Senior Portfolio Manager, Fixed Income, and Isaac Meng, Portfolio Manager, Fixed Income, outline why they believe China fixed income can continue to benefit from several key drivers.

As we approach the end of 2021, our constructive view on the Chinese onshore bond market at the beginning of the year has played out, despite a generally challenging environment for global fixed income markets due to rising interest rates. Going forward, we believe that China bonds should continue to benefit from several key drivers, namely the call to re-engage policy easing, sustainable currency strength, and their diversification benefits for global investors.

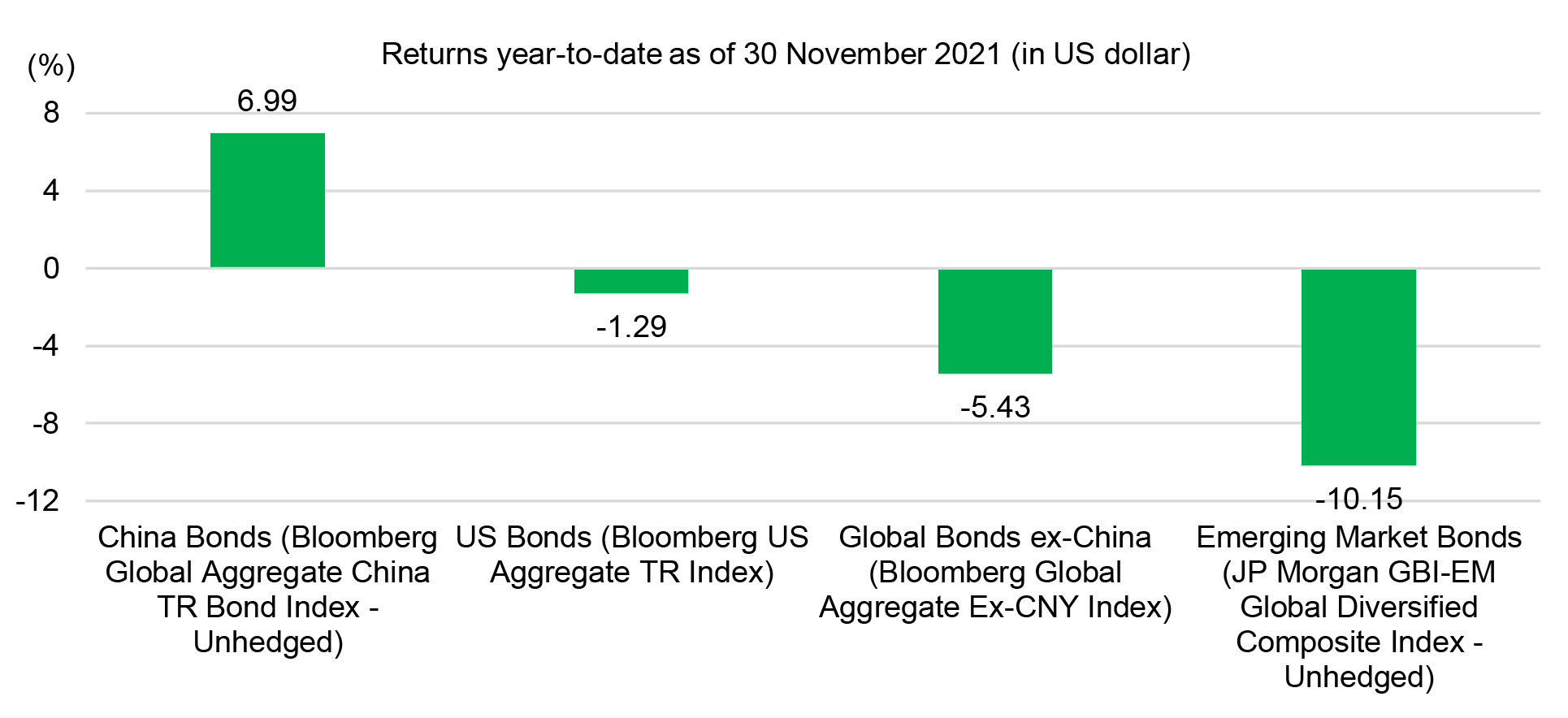

China bonds (based on the Bloomberg Global Aggregate China TR Bond Index) have outperformed other major bond categories, gaining +6.99% over the year to date – as of 30 November 2021, in US dollar (USD) terms. (see Chart 1).

Chart 1: Major bond market returns in 2021

Source: Bloomberg, data as of 30 November 2021. Past performance does not guarantee future results. It is not possible to invest directly in an index.

Related market moves:

The strong absolute and relative performance of Chinese bonds in 2021 can be attributed to the Chinese government maintaining a tighter monetary and fiscal stance that has helped CGBs retain an attractive yield level relative to other global government bond yields. Since the pandemic began in the first half of 2020, the People’s Bank of China (PBOC) has cut the 7-day reverse repo rate by only 30 bps to 2.2%. Unlike many global peers, the PBOC has refrained from implementing quantitative easing and has, therefore, preserved the capacity or policy room to ease monetary policy at a later stage. Accordingly, CGBs stand out with the bond curve offering a positive yield spread of between 150-200 bps above G7 sovereign bonds, given policy rates for G7 countries are negative or zero-bound with deeply negative real bond yields.

In terms of fiscal policy, China is the only major economy in the G201 to meaningfully tighten in 2021. Over the year, China’s fiscal impulse turned to -2.5% of GDP. The net issuance of government bonds (CGBs, local government financing, policy bank) declined by CNY 2.8 trillion over the first three quarters and is expected to be around CNY 2.4 trillion less than 2020 overall2. Moderate fiscal tightening has capped domestic demand and prices, while lower bond supplies have helped flatten the long end of the yield curve.

On the currency front, the CNY has appreciated by +2.6% against the USD and +8.3% against the CFETS currency basket, which measures CNY value against a trade-weighted basket of foreign currencies. The strength of the CNY has been underpinned by China’s record trade surplus of over US$650 billion as China’s economy benefitted from its resilient industrial supply chains, which have helped mitigate stagflation headwinds.

Overall, we think both China bonds and the CNY remain attractive given the above factors with ample risk-premium attached to China local bonds and the currency.

Looking ahead to 2022, we will closely watch the following three key macro themes and their implications.

1. Weakening of Chinese domestic demand: A call to re-engage policy easing

Chinese policymakers calibrated the 2022 economic planning at the annual Central Economic Work Conference on 10th December, where GDP growth and inflation targets, monetary policy, and fiscal budget objectives were agreed upon. We believe that sustaining a benign macro environment with stable growth and financial stability will be paramount ahead of the 20th Party Congress due to be held in the second half of 2022. The Party Congress is held every five years and is responsible for formally approving the membership of the Central Committee, which comprises the top leaders of the Communist Party of China.

Given the weaker economic data experienced in the second half of 2021, we believe there is a strong case for some moderate loosening of China’s monetary and fiscal stance, while additional credit and regulatory easing can be expected to provide relief to cushion the impact of the downturn in the property sector on the broader Chinese economy.

On 6th December, the PBOC made a broad-based 50 bps cut in the reserve requirement ratio (RRR) as widely expected by the market after the recent speech by Premier Li when he indicated that the RRR would be cut to support the real economy amid increasing signs of downside risk. According to the central bank, this will unlock CNY 1.2 trillion of long-term funding. We see the move as a clear sign of policy easing to address negative developments in the economy, while further monetary easing can still be expected in early 2022.

Chart 2: China government bonds stands out with positive yield spread

Source: Bloomberg, data as of 30 November 2021. Past performance does not guarantee future results. It is not possible to invest directly in an index.

2. COVID developments: The Omicron variant and evolution of pandemic stagflation supply shocks

While we are close to two years into the pandemic, there are still no signs of a clear ending in sight. Recently, risk markets have been roiled by the discovery of the Omicron variant and the uncertainty surrounding its impact on global growth. Economic data for the Chinese economy remains lacklustre, and a deeper pandemic could result in further stagflation supply shocks that would have important consequences on investors’ risk appetites and could drive their exposure to Chinese bonds in the short term.

3. Interest rate normalisation: An exit of pandemic stimulus, Fed tapering, and the path to higher rates

The Fed has proactively signalled its intention to increase the speed of tapering to exit its pandemic stimulus while the market is also currently pricing in two 25 bps rate hikes in the second half of 2022. Clearly, this will be an important theme for all asset classes and directly impact the attractiveness of Chinese bond yields versus US bond yields and determine the relative value of the CNY against the USD.

To summarise, our baseline 2022 outlook for China bonds is as follows:

From a positioning perspective, we believe investors can benefit from the following:

To conclude, China bonds are expected to remain attractive in 2022, buoyed by potential moderate policy easing, China’s divergent macro-policy cycle versus other major economies, as well as sustainable strength in the CNY which has been supported by China’s elevated trade surplus and persistent investor inflows.

1 Manulife Investment Management, as of December 2021.

2 WIND, Manulife Investment Management, as of December 2021.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited