The latest article of our Diverse Asia series examines the changes to family structure taking place across Hong Kong, Indonesia, Malaysia, and Taiwan. It also considers a closely associated issue, which refers to the role that family support can play for old-age sense of security, in particular relating to income and care support. The content has been developed in partnership with the Sau Po Centre on Ageing at The University of Hong Kong.1

Gender and family are intertwined in shaping individuals’ experiences and behaviour throughout the lifecycle. The very concept of family has evolved significantly over the past several decades. The decline in birth rates that began in the 1960s has continued as more women have gained access to better education and greater bodily autonomy and actively sought the wider job opportunities this has afforded them. In addition, more people are choosing to get married and start a family later in life, if at all.

Multigenerational households that were once a common way of life in Asia are now much more disjointed, as each generation has greater choices to live independently. Moreover, younger generations have sought better economic returns that often requires them to leave their hometown communities and their families for more economically developed locations and more urbanised communities. Unquestionably, this has taken its toll on the feasibility of familial support that older generations would previously have been able to rely on during their old age. It will also continue to cause complications for younger generations as they grow older.

In many respects, the “traditional” nuclear family—featuring a mother, father, and at least one child—is no longer the only option. Non-traditional families consisting of a single parent or guardian, or same-sex parents/guardians, are increasingly common. Higher divorce rates have resulted in “blended” families (where the family unit includes children from previous relationships) becoming more normalised.

The concept of family has evolved, and attitudes, as well as dependence on familial support, must evolve with it. We’ve noted in past articles that the Asia-Pacific region shouldn’t be viewed as a homogenous entity. While Asia’s demographic trends may be broadly consistent, different factors are in play depending on the birth rates and population goals in individual countries or markets. The demographic challenge has already led to the announcement of several government policies and intervention measures aimed at increasing birth rates and encouraging more children. But for this article, we want to raise other critical issues. For example:

How should the complexities of the family structure be recognised and addressed?

How will changing family dynamics affect the retirement readiness and quality of life for the future cohort of older adults?

What issues and mindsets should be embraced in Asia that are typical only to Asian family values?

As with our other Diverse Asia insight pieces, we’ve gathered insightful data and proprietary research into the family structures across our chosen markets of Hong Kong, Indonesia, Malaysia, and Taiwan. Our aim is to highlight how the changing nature of family life is having an impact on retirement security, in particular financial and instrumental support to older adults, now and in the future.

Family structures evolve, and the implications of these shifts continue to be a highly complex issue. Moreover, familial support can vary significantly across markets and must be understood in specific social and cultural contexts. For this insight piece, we’ve elected to consider familial changes in each of our four markets across the following dimensions:

Horizontal: determining how household sizes have changed in recent decades

Vertical: considering contemporary surviving generations and living arrangements in the household

These dimensions (household sizes and living arrangements) have been chosen because there are overlaps between the concept of “family” and “household.” While the household is one of the most commonly used social and budgetary units (Fan, C.C., 2022), for older adults, their living arrangements are usually a significant determinant of their economic welfare (Tung & Lai, 2012). Living arrangements also imply the availability of different types of familial support.

Over the last two decades, the average household size (the horizontal dimension) across all four Asian markets has been shrinking gradually, although the rate of change is less significant for Indonesia2:

In Hong Kong, the average domestic household size has fallen from 3.3 persons in 2000 to 2.7 persons in 2021.3

In Taiwan, the average domestic household size has fallen from 3.3 persons in 2000 to 2.8 persons in 2020.4

In Malaysia, the average domestic household size has fallen from 4.6 persons in 2000 to 3.8 persons in 2020.5

Whereas in Indonesia, the average domestic household size increased from 3.9 persons in 2000 to 4.0 persons between 2005 and 2009 before returning to 3.9 between 2010 and 2019 (the most up-to-date data available).6

According to our observation, shrinking family size is a common trend among most of observed markets. How about living arrangements?

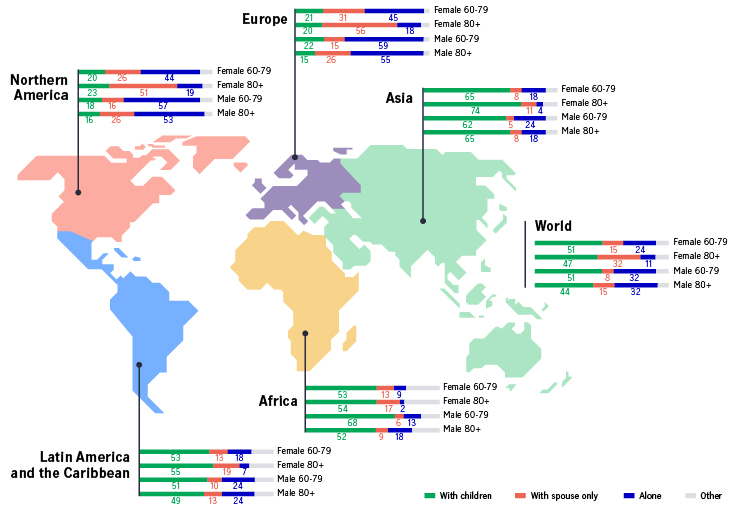

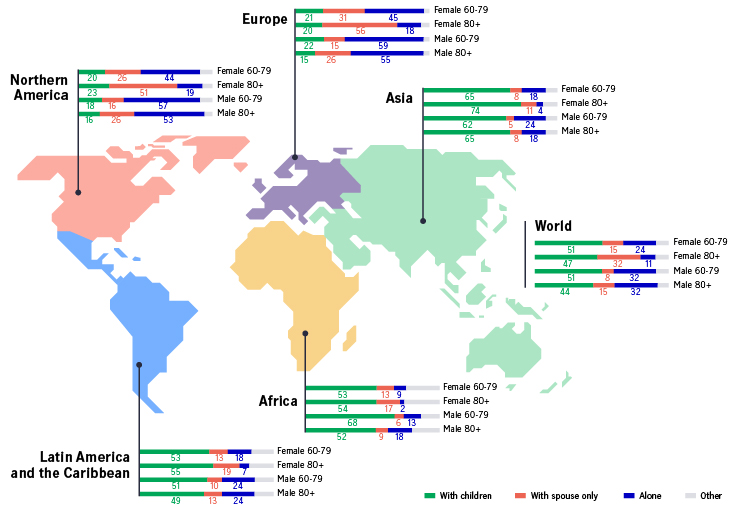

Chart 1 paints a broad-brush international comparison of living arrangements for the world’s major markets. Compared with developed markets in Europe and North America, living with adult children (therefore likely more shared monetary support) has still been the mainstream living arrangement of older adults in Asia, regardless of observed shrinking family size. Notably, Asia also has the lowest rate of its older population living alone globally.

Living arrangement (or co-residence in some literature) is usually treated as a proxy to indicate the availability/mechanism of familial social support, especially instrumental or emotional support, which is mainly provided with physical presence of family members.

Source: United Nations, Department of Economic and Social Affairs, Population Division (2017). Living Arrangements of Older Persons: A Report on an Expanded International Dataset (ST/ESA/SER.A/407). Latest country-specific data can be accessed here: Household size & composition, 2022; Living arrangement for older adults, 2022.

Source: United Nations, Department of Economic and Social Affairs, Population Division (2017). Living Arrangements of Older Persons: A Report on an Expanded International Dataset (ST/ESA/SER.A/407). Latest country-specific data can be accessed here: Household size & composition, 2022; Living arrangement for older adults, 2022.

Source: United Nations, Department of Economic and Social Affairs, Population Division (2017). Living Arrangements of Older Persons: A Report on an Expanded International Dataset (ST/ESA/SER.A/407). Latest country-specific data can be accessed here: Household size & composition, 2022; Living arrangement for older adults, 2022.

Source: United Nations, Department of Economic and Social Affairs, Population Division (2017). Living Arrangements of Older Persons: A Report on an Expanded International Dataset (ST/ESA/SER.A/407). Latest country-specific data can be accessed here: Household size & composition, 2022; Living arrangement for older adults, 2022.

Here’s how diverse with regard to an older person’s living arrangement is in our focused markets:

The proportion of Hong Kong older persons living with a spouse and children has remained unchanged at around 30% since 2006.

51.2% of Taiwan older folk aged 65 or above lived with their children.

70.1% of Malaysia’s older population lived with family members and others in their household.

Most of Indonesia’s 60+ population still lives with extended families; close to 60% live with their adult children.

The changing shape of the family structure, which can be attributed to multiple factors, including modernisation and urbanisation, is a universal challenge faced not just by markets in the Asia-Pacific region. It also applies to Western countries as Megan Gilligan describes “a shift in the structure of families from a pyramid-like structure, with multiple individuals at the base, to a longer, thinner structure that more closely resembles a beanpole” (Gilligan, et. al., 2018).

However, in contrast with Western countries, most older adults in Asia still reside with their children, even if that proportion decreases over time. Hong Kong, for example, is an affluent market characterised by having an increasing proportion of singleton and couple-only older households and is, therefore, tracking more closely to the “beanpole” family structure demonstrated in the West.

Moreover, although children are commonly viewed as important potential sources of “social insurance” in old age across most of Asia, this is under threat by the declining fertility rate (see fertility concerns under “The effects of COVID-19: a reality check”). There are few signs that this trend will reverse, even with government intervention. As a result, the next generations must not only provide support for their retired parents but also prepare for diminished upstream familial support during retirement and old age.

We should also note that as family structures have changed, those supporting mechanisms are also evolving. In other words, there are dynamic patterns of intergenerational support in each specific welfare regime. Therefore, using long-established descriptions of living arrangements may not adequately portray the networks, pathways, and direction of support between older persons and those they call “family” (UNDESA, 2017). It would be remiss to ignore or exclude, for example:

There are increasingly common arrangements in many developing countries, where children live in multiple-family compounds or in the same neighbourhood as their older parents.

Potential support from children or extended family living in the same township or city as their older parents while not cohabiting with them.

Unspecified support can be either upstream (from children to older parents) or downstream (from older parents to children, more details in the next section).

In summary, while family structures are increasingly complex and nontraditional, this does not necessarily lead to the conclusion that family structures are broken and the older generation is being abandoned. Beyond the household size and the living arrangement, in terms of old age support, “family members’ capacities vary, and competing values beckon” (Kreager & Schröder-Butterfill, 2008). The diversity of intergenerational support flows may suggest that family systems have more flexibility and adaptive capacity, therefore “a much closer look at the structure and content of flows of support over time is needed, and the patterns of actual support require comparing to stated norms” (Kreager & Schröder-Butterfill, 2008).

To most Hong Kong citizens, maintaining the same standard of living in Hong Kong for years after retirement seems like a challenge. And most older persons in Hong Kong are more likely to live in the domestic household instead of non-domestic households (e.g., hospital, elderly homes or other third places represent less than 10% of total older persons according to 2016 Census and Statistics Department Figure).

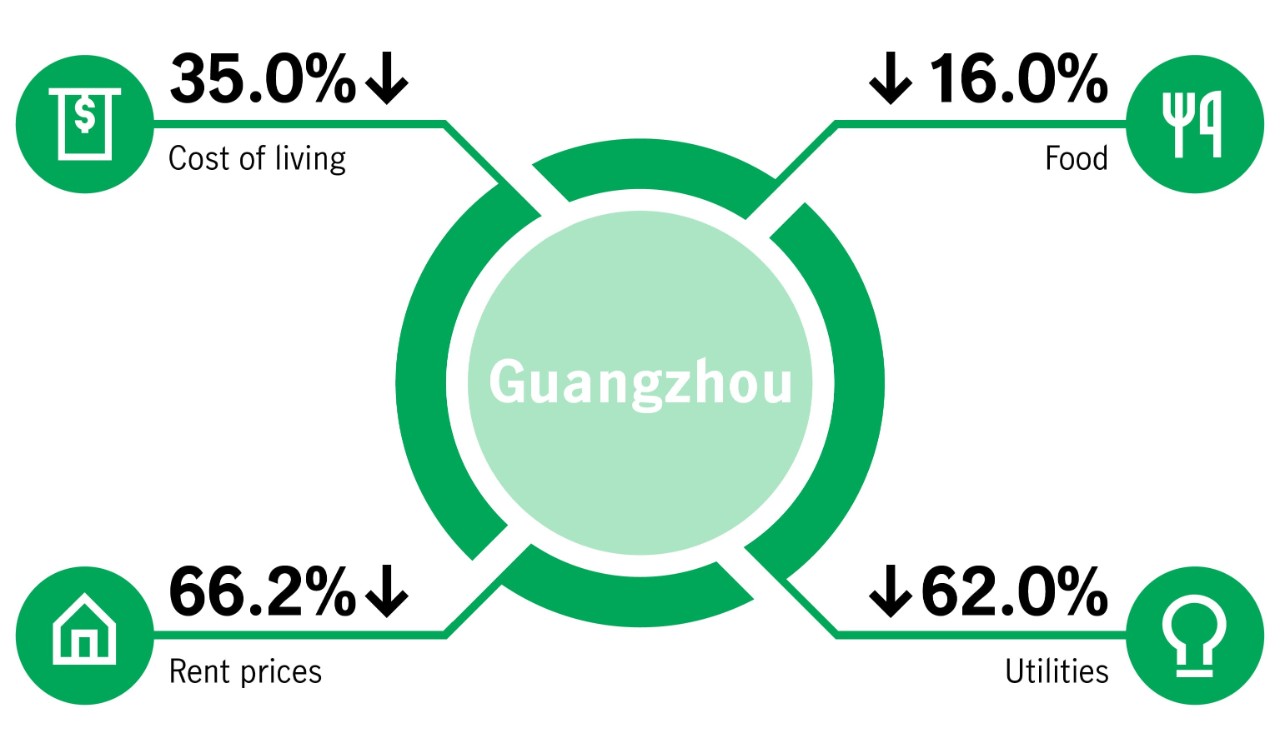

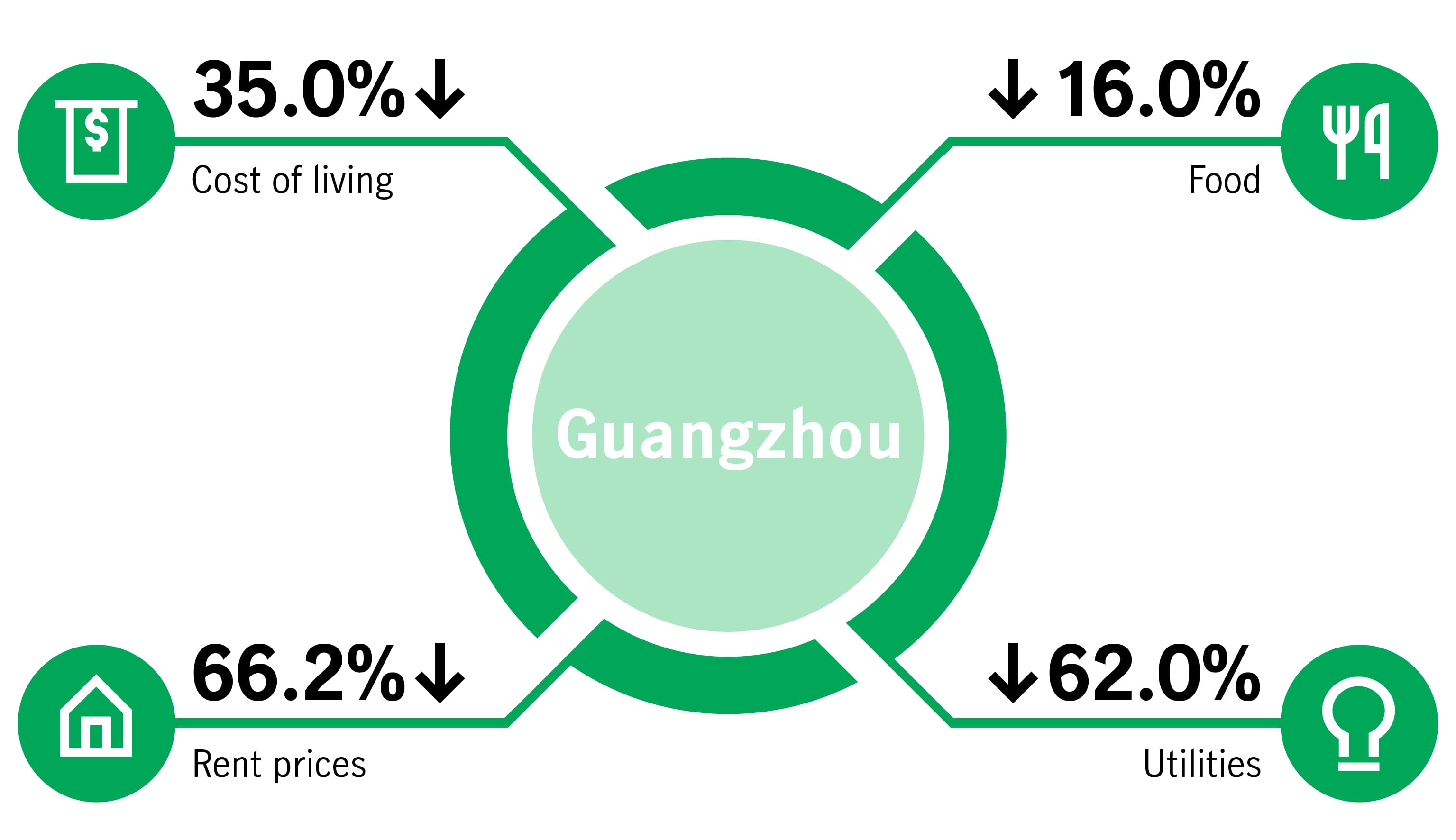

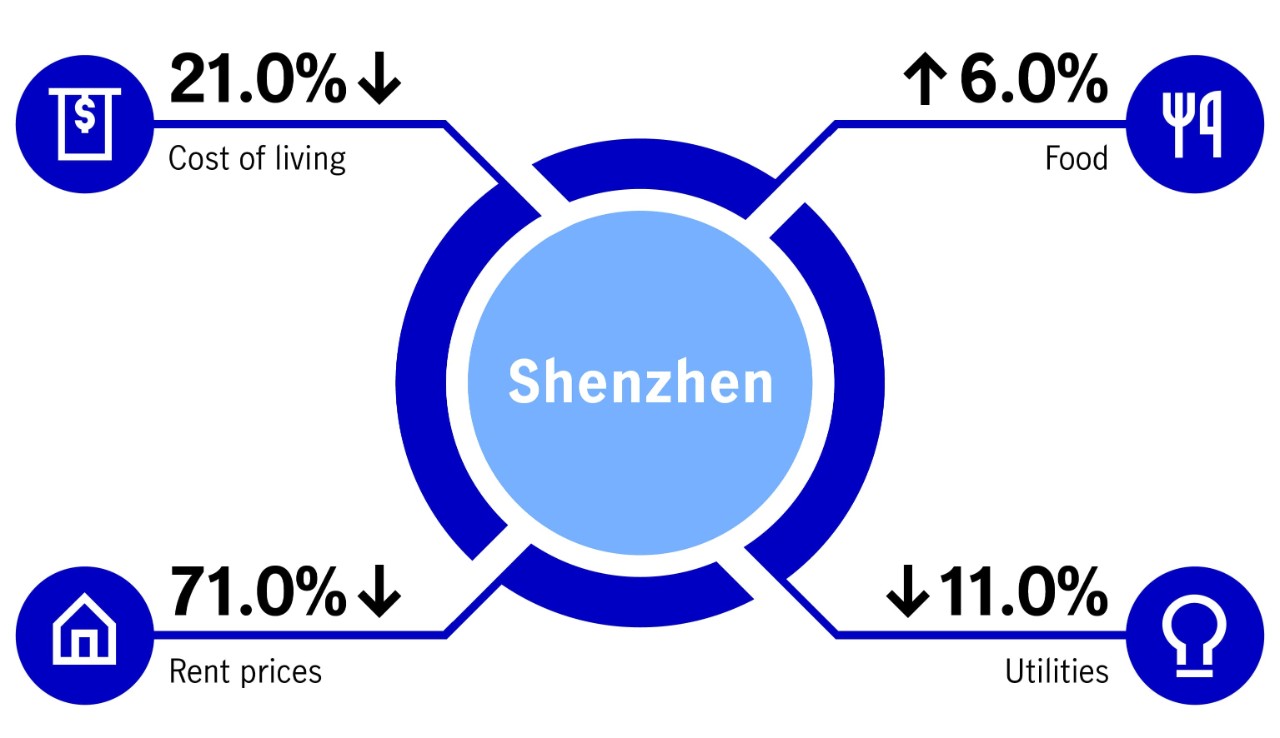

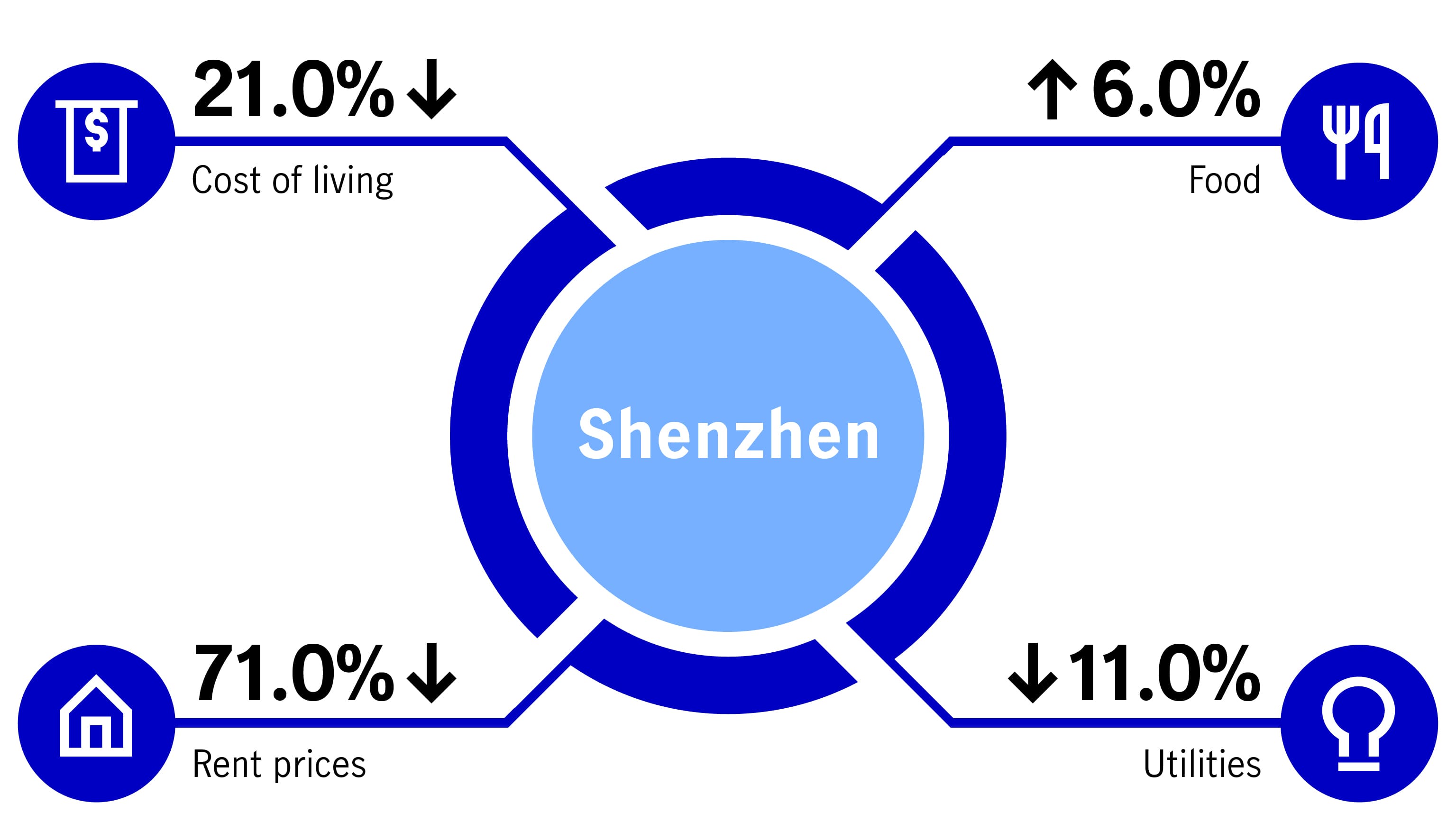

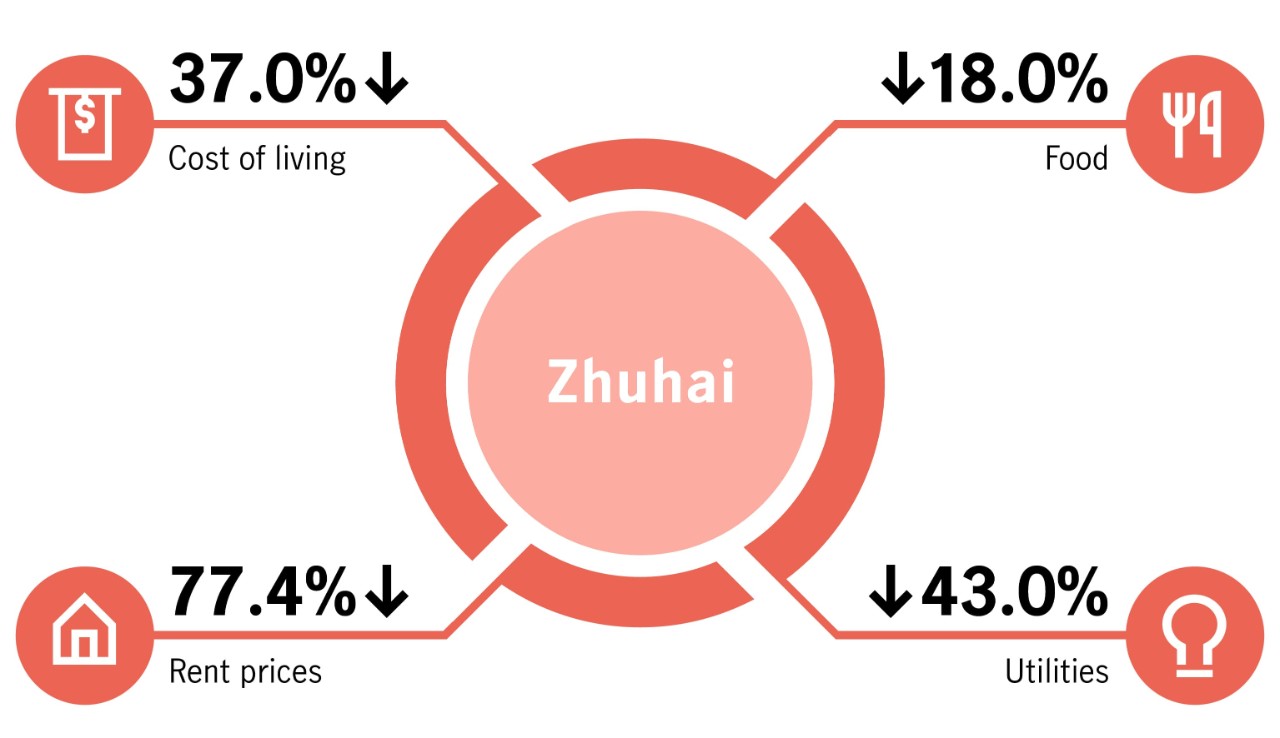

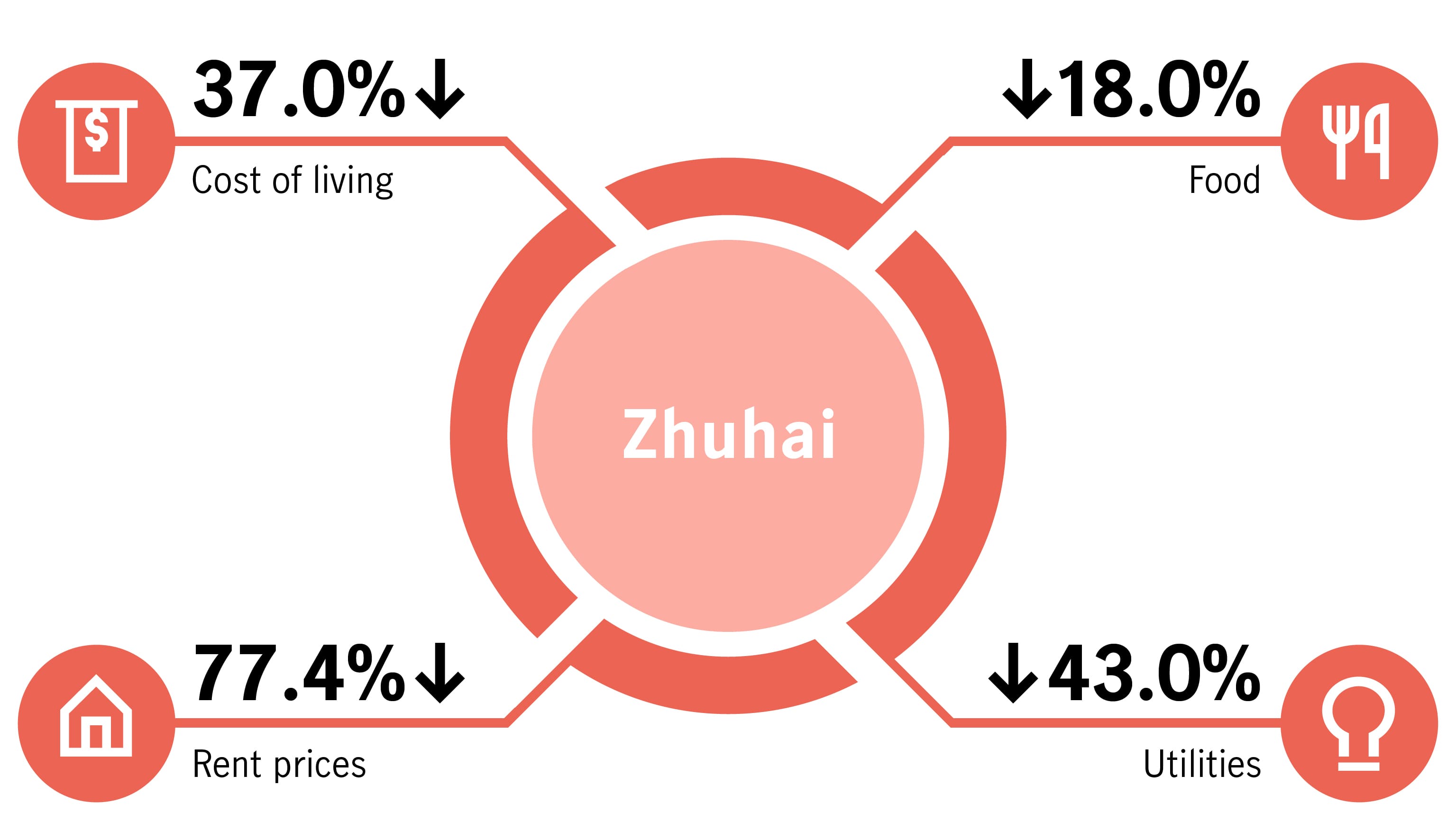

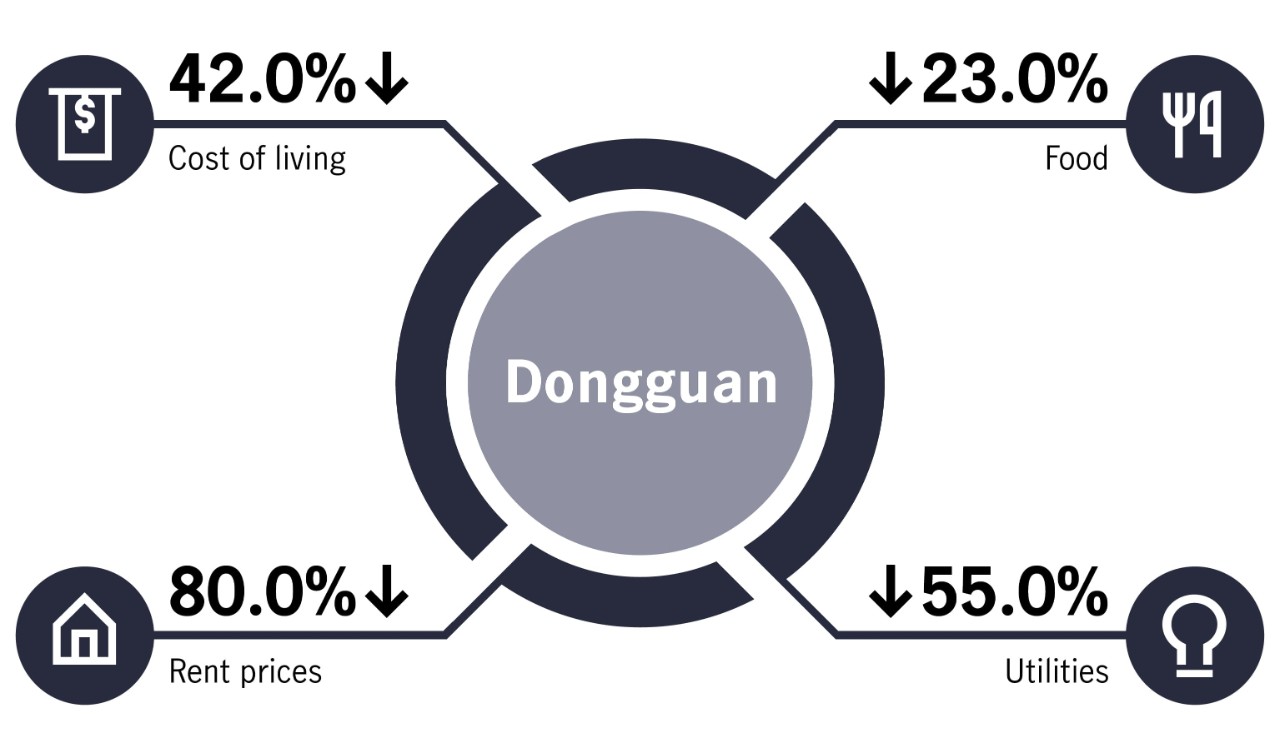

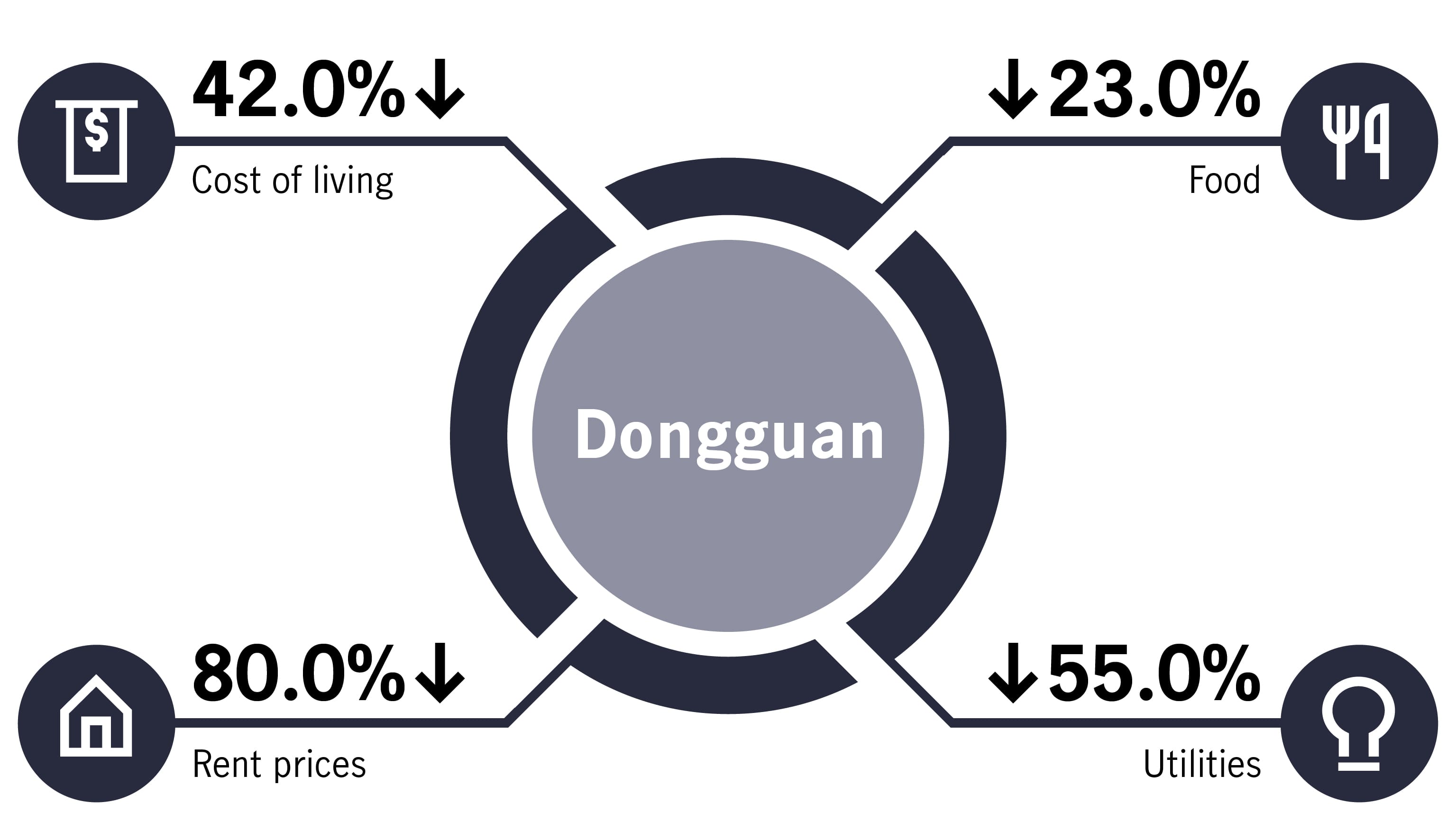

But what if Hong Kong retirees choose to move to another city where the cost of living is lower, so they can enjoy the benefits of a lower cost of living while still retaining easy access to Hong Kong’s quality healthcare system?

This illustrative example explores a way to acquire a second home in a lower-cost area post-retirement. The charts below (using Hong Kong as the base city) shows that the overall cost of living (consumer prices excluding rent) in Greater Bay Area cities such as Guangzhou, Shenzhen, Zhuhai, and Dongguan can be as much as 20% to 40% lower than living in Hong Kong. Rent is the key differentiator, which is estimated at 60% to 80% lower in these four areas. This means retirement living in these Greater Bay Area cities requires much lower spending when compared with retiring in Hong Kong.

Therefore, while many worry that their retirement funds aren’t sufficient to support quality retirement living, the place they live when they retire could make a significant difference in how long their savings last to support their retirement.

Source: Manulife study; data from EIU, data as of September 2022.

This section investigates how older adults finance their retirement (i.e., the composition of income sources) in our four markets, as well as explores the role that intergenerational exchange (support) plays in old age security. There are essentially four main categories of familial support:

Financial support: this can involve providing financial resources, including paying bills, buying goods or services, or offering capital or credit.

Instrumental support: this can include a wide range of help, such as housework, cooking, shopping, running errands, transport, and personal care.

Emotional support: this can be as nonspecific as simply showing care and compassion for an older person, helping them to cope with their emotions and experiences, or ensuring they do not feel isolated and alone (particularly important during old age).

Informational support: this includes offering advice, guidance, or useful information on a broad variety of subjects, including financial, health, or other digital/administrative assistance. (Gillen, et. al., 2012, p.4)

Using an intergenerational solidarity framework, a scope review (Wong, et. al., 2020) identified the main factors associated with intergenerational transfer. In this context, intergenerational transfers are defined as any family-based support that flows from older to younger generations or vice versa. The review placed these factors into four distinct categories:

Demographics such as age, gender, marital status, education, and ethnocultural background);

Needs and opportunities, including health, financial resources, and employment status;

Family structures namely, family composition, family relationship, and earlier family events; and

Cultural-contextual structures including state policies and social norms.

Within the scope review, it was found that people in Asia received the highest proportion of financial support from family (Wong, et. al., 2020), a conclusion arrived at by drawing an international comparative study by Khan (2014). More importantly, this review suggests a useful framework for analysis and organising the interwoven factors in dimensions (i.e., financial and instrumental), directions (i.e., unidirectionally and bidirectionally). This will help inform our research and broader views on the transfer of resources between generations across our four markets of Hong Kong, Taiwan, Malaysia, and Indonesia.

In Hong Kong, living with the younger generation had the tendency to increase finance and care transfers, and the number of children was positively associated with monetary support. Previous research (Chou, 2008) found that compared with the number of siblings who also provided financial support to their older parents, the earning capacity of adult children is a stronger predictor of the amount of monetary support provided to older parents (p.797).

However, Hong Kong’s declining birth rate, and subsequent smaller family sizes, continue to threaten the foundations of family care. Moreover, the explosion of housing costs and the rising cost of daily living have contributed to a worsening financial situation for older adults. It has also undermined the younger generation’s financial capacity to care for their older parents.

In response to these new familial and sociocultural realities, Hong Kong’s older population has been forced to modify their long-standing filial care expectations (Bai, 2019) and continue working to pay for their upkeep. Over the past decade, the number of working older persons has more than doubled (up by 136.6%), mainly due to the surge in working older persons in the 65 to 74 age category.

Not all older persons are able to keep working in old age, however. In fact, older-persons-only households without employment income increased at a much higher rate of 80.6%, with median monthly domestic household income increased from $3,200 to $5,780 over the same 10-year period. This significant increase in income among older-persons-only households without employment income was partly caused by the increase in cash social benefits distributed by the Hong Kong Special Administrative Region’s government. These benefits include the Old Age Living Allowance, which was introduced in 2013 to support older persons in need of financial support (Census & Statistics Department, 2016). As a result, the increasing importance of welfare (public money) and old adults’ own labour income for Hong Kong’s older population continues to be evident.

Taiwan is projected to become a “super-aged” society within the next decade. In Taiwan, the support of older parents is a statutory obligation for adult children and is still considered a societal norm. As a result, Taiwan’s society embraces the concept of strong family ties and local communities that allow the older population to age actively in place. In 2017, Taiwan’s Report of the Senior Citizen Condition Survey by the Ministry of Health and Welfare reported that 98% of people aged 65 and older live at home, and nearly two-thirds of people aged 65 and above live with their children or other family members, while over 33% live in a three- or four-generation household.

Higher education levels of adult children, the presence of younger grandchildren, and older people’s ownership of properties have been three factors correlated with higher co-residence of older and younger generations. Sources of financial support for the older population is relatively balanced, with adult children or grandchildren being the main income source of around one-quarter (24.3%) of people older than 65. Even so, a decreasing trend has been noted more recently, in part because Taiwan’s government has stepped up efforts to establish a long-term care system that includes increasing coverage of pensions and insurance for the older population.

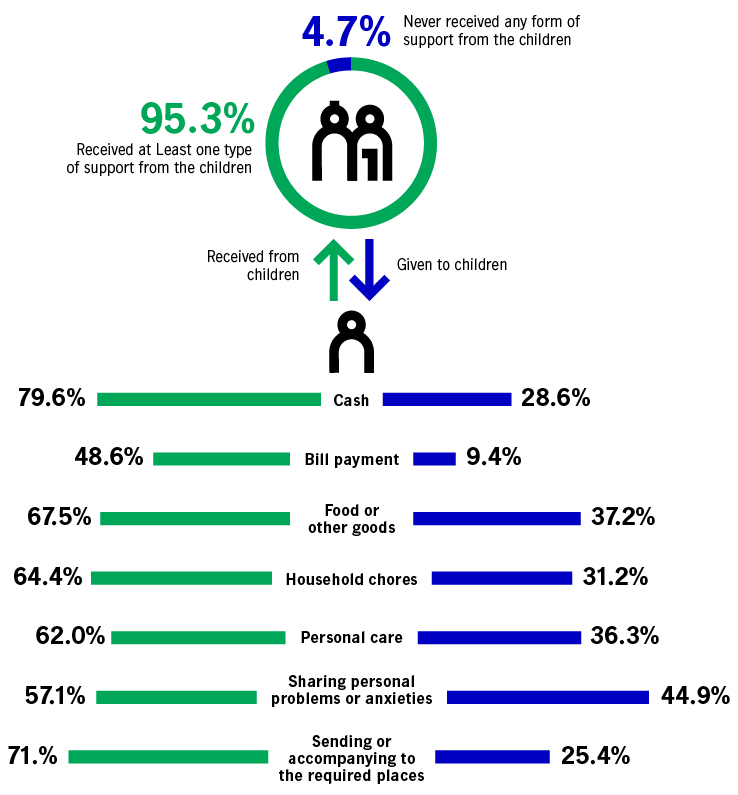

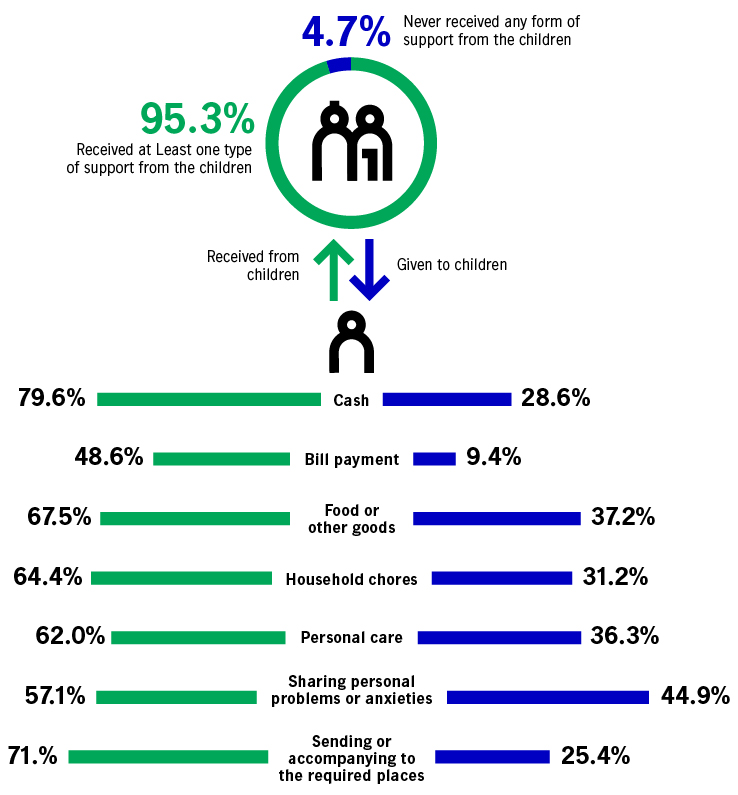

In Malaysia, it’s considered the children’s responsibility to give attention and support to their parents. A national survey showed overarching support has been provided to older adults from younger generations. Most of Malaysia’s older population (95.3%) receives support in the form of financial assistance, cooking and serving food, doing household chores, and for companionship and accompanying them on outings and visits. Whereas male offspring tend to provide financial support, female offspring are expected to provide support to parents (and in-laws) in the form of daily necessities and food (NPFDB, 2016).

But as no income source data was made available, it's harder to determine the proportion of assistance, and therefore whether any gaps exist. Most familial support studies tend to focus on diversity among major ethnic groups or from a gender perspective.

Source: National Population and Family Development Board (NPFDB). (2016). Report on Key Findings FIFTH MALAYSIAN POPULATION AND FAMILY SURVEY [MPFS-5] 2014. Malaysia.

Source: National Population and Family Development Board (NPFDB). (2016). Report on Key Findings FIFTH MALAYSIAN POPULATION AND FAMILY SURVEY [MPFS-5] 2014. Malaysia.

Source: National Population and Family Development Board (NPFDB). (2016). Report on Key Findings FIFTH MALAYSIAN POPULATION AND FAMILY SURVEY [MPFS-5] 2014. Malaysia.

Source: National Population and Family Development Board (NPFDB). (2016). Report on Key Findings FIFTH MALAYSIAN POPULATION AND FAMILY SURVEY [MPFS-5] 2014. Malaysia.

In Indonesia, as in other developing countries in the region, support for the older adults have primarily come from networks of families or relatives (Park, 2003; Huangfu & Nobles, 2022). Shared residences are an important mechanism for familial support (Witoelar, 2012). In addition, financial assistance often comes in the form of remittances received from adult children who have migrated elsewhere. For these migrants, “remittance is a currency of care.” (Hoang & Yeoh, 2015, p.3).

Child-to-parent transfers were not much associated with parents’ income or assets, and amounts transferred tend to increase along with parents’ age. Widowed mothers were more likely to receive larger transfers from children than other parents. (Park, 2003).

Research from the National Transfer Account indicates that older adults in Indonesia were characterised by:

Longer periods of working after retirement age, particularly for the self-employed

Dependent on their assets for their retirement

Being on the “giving” rather than “receiving” side of the intergenerational transfer, with net downward flows of wealth often extending very late in life

Scholars (Kreager & Schröder-Butterfill, 2008) also pointed out that the intergenerational supports within families tend follow a fluid arrangement which flows back and forth between family groups. For older family members, the strength of supports from adult children is often “a matter of considerable uncertainty” (p.1785).

Nevertheless, familial transfers appear to be needs-oriented, multi-directional across generations in Indonesia.

While no one-size-fits-all approach exists, the research across each of our four markets makes it clear that across Asia, financial security in old age can no longer be achieved through a single source of income. For people to enjoy an acceptable standard of living in old age, diversification of income must also play a critical role. Other sources of income, including familial transfer along with government benefits and welfare initiatives, must be used to help overcome the societal and demographic changes that are reshaping the family structure.

In our concluding section, we consider the challenges related to familial structure change, intergenerational support, and retirement readiness present across our four markets. We also consider any relevant actionable ideas and opportunities.

In Hong Kong, with family financial support declining, more than two-thirds of persons aged between 35 and 64 have prepared for their retirement financially; accumulating private savings (55.5%) was the most common way (Chou et al, 2016).

In the coming decades, a continuous growth of the savings in the Mandatory Provident Fund and private retirement savings are expected, and “measures are needed to facilitate the decumulation of these savings after retirement, while reducing both the threat that increasing longevity will pose to retirees’ income security and the risks associated with investments” (Chou, et. al., 2016, p.14).

Research investigating annuity demand in Hong Kong has pointed out that older people who didn’t expect to receive financial support from their adult children were more likely to choose to buy an annuity than those expecting to receive a certain amount of financial support from their adult children (Lee et al, 2019).

By observing the pattern of the bequest motive’s impact on the demand for annuity, the same research also found that a bequest motive operates (mainly as a barrier) over the first stage of retirement—the first 10 to 20 years—and subsequently decline. Therefore, it’s very likely that during the early retirement period of the retirees, younger generations in their family may still need support (such as costs associated with rearing their own children). Therefore, the decumulation plan of the retirement assets in this period would still be affected by the retiree’s familism mindset.

The gender lens must also be considered. A recent report issued by Hong Kong Deposit Protection Board (2021) revealed that among couples with mutual saving goals and practice, the savings would usually be managed by the wives. The research implies that decumulation would sometimes also be a collective decision made by the household instead of by the individual. Therefore, a gender lens would help achieve a better understanding of household financial planning and behaviours in Hong Kong.

Facing the challenges, recent policy developments in Taiwan have set an example of a more holistic approach regarding retirement protection. Examples of government initiations and reforms include:

Reform of Public pension and Military Pension reform (2017-2018): improving the sustainability of Taiwan’s pension system

Long-term Care 2.0 Plan (2017): made on the long-term care system for making it available for those in need, which also aims at reducing the financial burden associated with care

Middle-aged and Elderly Employment Promotion Act (2019): to improve employment service for older workers, and facilitate age-friendly environment by encouraging employees to support and retain senior workers

White Paper to outline comprehensive policies for aged society (2021): enhancing collaborations of all government departments to provide more comprehensive support for older adults

On a more personal level, as the Topical Report on Income Security (CUHK Jockey Club Institute of Ageing, 2020) pointed out, “social pensions can enhance individuals’ self-esteem and dignity by ensuring their retirement is driven by a reliable and steady source of income and improved social connections through sharing of additional resources. Social pensions can also promote overall economic development by boosting household consumption of food and healthcare” (p.19)

A study by Abdullah et. al. (2021) shows the impact of delayed childbirth by citing data from “Fifth Malaysian Population and Family Survey” MPFS-5. The study finds that 11% of ever-married women aged 40 and over had children below seven years of age. This means many men (who on average are about four years older than their wives) would still have to support their school-going children on retirement. MPFS data from 2014 also showed that about 1 in 10 persons aged 60 and above were still giving financial assistance to their children. That figure is expected to accelerate in the future.

Budgeting for family needs is therefore complicated. The research suggests future cohorts of retirees may face different roles and responsibilities compared with current retirees. These will need to be carefully budgeted for.

While bigger households would usually suggest more potential support for the older adults, a 2017 case study titled “Determinants of Retirement Wealth Adequacy in Malaysia” found that household size had a negative association with retirement wealth adequacy (defined in the study as “the retirement income from either defined benefit plan or defined contribution plan”). In other words, larger households often face lower financial adequacy due to higher spending and lower savings (Alaudin, et. al., 2017).

As the only one “young” region among the four markets, and with a fertility rate still above the replacement level, the family structure changes currently being experienced in Indonesia appear to follow a different pattern; however, the increasing longevity of younger generations is still likely to affect the availability of traditional familial support practices experienced by older generations.

Compared with countries with better pension coverage, financial adequacy in old age may “depend much on individual performance in the labour market and the success in investing the saving” (Ahmad, et. al., 2022). Therefore, particularly in regions with lower state welfare support and smaller households, a combination of a stronger compulsory defined contributory plan and enhanced retirement planning literacy are both necessary to ensure a greater proportion of the older population achieves a comfortable life in retirement.

Moreover, a 2022 study shows that “civil servants, military, and police in Indonesia, will be able to maintain their pre-retirement standard of living only when the saving during the working period is invested with rate of return at least 9.0% annually and continue being invested with the same rate of return during the retirement period” (Ahmad, et. al., 2022). The findings suggest that even those members of society fortunate to receive a formal pension from the state will need to find other sources to supplement their retirement wealth adequacy.

The Indonesian government therefore must keep working to enhance the coverage and adequacy of social pensions, while also facilitating and encouraging accumulation for the retirement protection of its current working population.

As the above research across our four markets demonstrates, the evolution of the “traditional” family structure has complicated the financial picture for modern-day families. Multigenerational households are now much more fragmented, with each generation choosing—to a varying degree—to live independently.

Budgeting for family needs, particularly when some family members are in old age, is now proving to be increasingly complicated. Therefore, the response from individuals and the state must evolve to embrace the broader dispersion of the familial structure. The suggested approach would appear to be a combination of stronger compulsory defined contributory plans for those in the accumulation phase of retirement savings, as well as enhanced retirement planning literacy to educate people of all ages about the intrinsic human need for a comfortable life in retirement where people have both a reliable and secure source of income, as well as valuable and meaningful human social interactions.

Manulife Investment Management engages Professor Vivian Lou from the Sau Po Centre on Ageing at the University of Hong Kong in the capacity of consultant (consultancy fee incurred) for the Diverse Asia thought leadership projects.

The data in this article has been compiled and verified to the best of our knowledge, but no warranty is given as to the completeness, accuracy, up-to-datedness of the information provided.

C&SD, HKSAR: C&SD: Table 5: Statistics on Domestic Households (censtatd.gov.hk).

Statistical Bureau, Taiwan. Retrieved from https://www.stat.gov.tw/public/Data/1112144316VT5YTOVB.pdf.

Khazanah Research Institute, 2018; The State of Households 2018: Different Realities. Kuala Lumpur: Khazanah Research Institute. 2020 census data retrieved from DOSM website.

2000-2015 data retrieved from https://www.bps.go.id/dynamictable/2015/09/07/849/rata-rata-banyaknya-anggota-rumah-tangga-menurut-provinsi-2000-2015.html. 2019 data cited from BPS-Statistics Indonesia (2020). Statistical Yearbook of Indonesia 2020. p.93, supported by United Nations, Department of Economic and Social Affairs, Population Division (2022). Database on Household Size and Composition 2022. UN DESA/POP/2022/DC/NO. 8.

Hong Kong: Census and Statistics Department, 2016, latest available data. Taiwan: Census data in 2020, latest available data. Malaysia: Fifth Population and Family Life Survey, 2014, latest available data. Indonesia: United Nations Department of Economic and Social Affairs, 2019.

2658937

Abdullah, A. S., Tey, N. P., Mahpul, I. N., Azman, N. A. A., & Hamid, R. A. (2021). Correlates and consequences of delayed marriage in Malaysia. Institutions and Economies Vol.13, No.4, pp.5-34. https://doi.org/10.22452/IJIE.vol13no4.1

Ahmad, I. A., Moeis, N. D. N., Aris A. & Vid Adrison | Walid Mensi (Reviewing editor). (2022). A Trade-off between Old-age Financial Adequacy and State Budget Sustainability: Searching a Government Optimum Solution to the Pension System in Indonesia, Cogent Economics & Finance, 10:1, DOI: 10.1080/23322039.2022.2079176

Census and Statistics Department. (2018). 2016 Population By-census Thematic Report: Older Persons. Hong Kong Special Administrative Region. Retrieved from: https://www.statistics.gov.hk/pub/B11201052016XXXXB0100.pdf

Chou, K.L., Chan, W.S., Inkmann, J., Kippersluis, H.V., Lee, S.Y., Yan, J. (2016). How to Increase the Demand for Annuity in Hong Kong: A study of Middle-Aged Adults. (Report No. 2014.A5.005.14E). Policy Innovation and Co-ordination Office, HKSAR. Retrieved from https://www.legco.gov.hk/yr15-16/english/panels/ws/papers/ws20160418cb2-1301-2-e.pdf

Chou, K.L. (2008). Parental Repayment Hypothesis in Intergenerational Financial Transfers from Adult Children to Elderly Parents: Evidence from Hong Kong, Educational Gerontology, 34:9, 788-799, DOI: 10.1080/03601270802095972

CUHK Jockey Club Institute of Ageing. (2020). AgeWatch Index for Hong Kong: Topical Report on Income Security. The Hong Kong Jockey Club. Retrieved from https://www.jcafc.hk/uploads/docs/Topical-Report-Income-Security_final.pdf

Fan, C.C. (2022, October 7th). Migration in the Global South: Householding, Gender and Intergenerational Perspectives. [Power Point Slides]. University of Hong Kong, Geography Distinguished Webinar Series.

Frankenberg, E., Lillard, L., & Willis, R. J. (2002). Patterns of Intergenerational Transfers in Southeast Asia. Journal of Marriage and Family, 64(3), 627–641. https://doi.org/10.1111/j.1741-3737.2002.00627.x

Fu T.H. (2022, November 5th). Challenges of Population aging and Retirement Protection in Taiwan. [Power Point Slides]. Retirement in Asia. Kyushu University Asia Week.

Gillen, M., Mills, T., & Jump, J. (2012). Family Relationships in an Aging Society: FCS2210/FY625, rev. 11/2012. EDIS, 2012(11). https://journals.flvc.org/edis/article/view/120317/118645

Gilligan, M., Karraker, A., & Jasper, A. (2018). Linked Lives and Cumulative Inequality: A Multigenerational Family Life Course Framework. Journal of family theory & review, 10(1), 111–125. https://doi.org/10.1111/jftr.12244

Hermalin, A. I. (2002). The well-being of the elderly in Asia: a four-country comparative study. University of Michigan Press.

Hoang, L., & Yeoh, B. (2015). Transnational Labour Migration, Remittances and the Changing Family in Asia. Palgrave Macmillan UK.

Hong Kong Deposit Protection Board. (2021). Survey on Hongkongers’ Sense of Security on Savings 2021. Retrieved from https://a2022.pori.hk/wp-content/uploads/2021/11/HKDPB_Saving_Monitor_2021_Eng_survey_findings_10Nov2021_v2_pori.pdf HKSAR.

Huangfu, Y., & Nobles, J. (2022). Intergenerational support during the rise of mobile telecommunication in Indonesia. Demographic Research, 46, 1065–1108. https://doi.org/10.4054/DemRes.2022.46.36

Jackson, R., & Peter, T. (2015). From Challenge to Opportunity: Wave 2 of the East Asia Retirement Survey. Retrieved November 14, 2022, from https://www.globalaginginstitute.org/assets/client-assets/gapi/downloads/publications/EARR_Wave2_Report_DL_LR-EIINC.pdf

Koda, Y., M. Uruyos, and S. Dheera-Aumpon. (2017). Intergenerational Transfers, Demographic Transition, and Altruism: Problems in Developing Asia. ADBI Working Paper 786. Tokyo: Asian Development Bank Institute. Retrieved from: https://www.adb.org/publications/intergenerational-transfers-demographic-transition-altruism

Kreager, P., & Schröder-Butterfill, E. (2008). Indonesia against the trend? Ageing and inter-generational wealth flows in two Indonesian communities. Demographic Research, 19(52), 1781–1810. https://doi.org/10.4054/DemRes.2008.19.52

Lowenstein, A. (1999). Intergenerational family relations and social support. Zeitschrift Für Gerontologie Und Geriatrie, 32(6), 398–406. https://doi.org/10.1007/s003910050136

Ministry of Health and Welfare. (2018). Report of the Senior Citizen Condition Survey 2017. Retrieved from https://dep.mohw.gov.tw/DOS/lp-5095-113-xCat-y106.html

National Population and Family Development Board (NPFDB). (2016). Report on Key Findings FIFTH MALAYSIAN POPULATION AND FAMILY SURVEY [MPFS-5] 2014. Malaysia.

Noriszura, Ismail & Alaudin, Ros Idayuwati & Isa, Zaidi. (2017). Determinants of Retirement Wealth Adequacy: A Case Study in Malaysia. Institutions and Economies. 9. 81-98.

Lee,S.Y., Chou.K.L., Chan.W.S., & Kippersluis,V.H. (2019). Consumer Preferences and Demand for Annuities: Evidence from Hong Kong, Journal of Aging & Social Policy, 31:2, 170-188, DOI: 10.1080/08959420.2018.1542242

United Nations, Department of Economic and Social Affairs, Population Division (2017). Household Size and Composition Around the World 2017 – Data Booklet (ST/ESA/SER.A/405).

United Nations, Department of Economic and Social Affairs, Population Division (2017). Living Arrangements of Older Persons: A Report on an Expanded International Dataset (ST/ESA/SER.A/407).

Witoelar. F. (2012). Household Dynamics and Living Arrangements of the Elderly in Indonesia: Evidence from a Longitudinal Survey. Aging in Asia (pp. 229–260). National Academies Press.

Wong, E. L., Liao, J. M., Etherton-Beer, C., Baldassar, L., Cheung, G., Dale, C. M., Flo, E., Husebø, B. S., Lay-Yee, R., Millard, A., Peri, K. A., Thokala, P., Wong, C. H., Chau, P. Y., Chan, C. Y., Chung, R. Y., & Yeoh, E. K. (2020). Scoping Review: Intergenerational Resource Transfer and Possible Enabling Factors. International journal of environmental research and public health, 17(21), 7868. https://doi.org/10.3390/ijerph17217868

Xue Bai (2019) Hong Kong Chinese aging adults voice financial care expectations in changing family and sociocultural contexts: implications for policy and services, Journal of Aging & Social Policy, 31:5, 415-444, DOI: 10.1080/08959420.2018.1471308

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited