When it comes to managing household finances, budgeting makes sense. However, it’s sometimes hard to accurately estimate what your outgoings will be each month. Unexpected bills and one-off costs can disrupt the best-laid plans! While there is no perfect way to ensure you live within your means, we have some suggestions that might help.

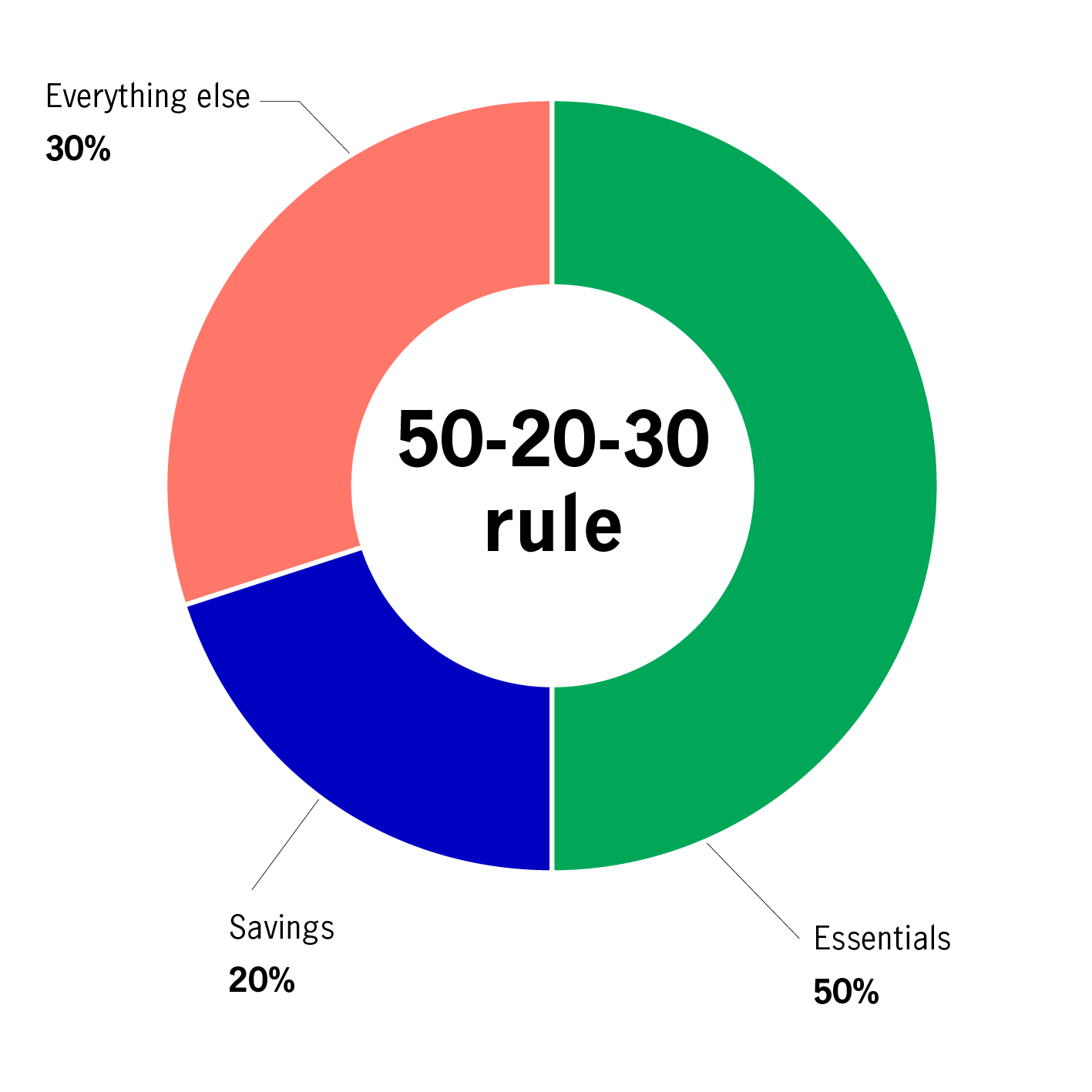

First of all, there’s the 50-20-30 rule. A wealth-management technique that divides your monthly income into three categories:

50% for essentials: rent and other housing costs, such as groceries, electricity or transport

20% for savings: savings accounts, retirement contributions, loans, or credit card payments

30% for everything else: non-essential expenses, such as clothing, eating out, monthly streaming subscriptions, or gym memberships

While you might not have a problem remembering the numbers 50-20-30, the rule itself isn’t always easy to live by. When it comes to expenses, one size doesn’t fit all and lifestyles will vary depending on, for example, where you live. City living can be more expensive and people may spend a large part of their income on rent, which can cause problems if your income is irregular. Housing costs can also be particularly tough for those in low-paid jobs.

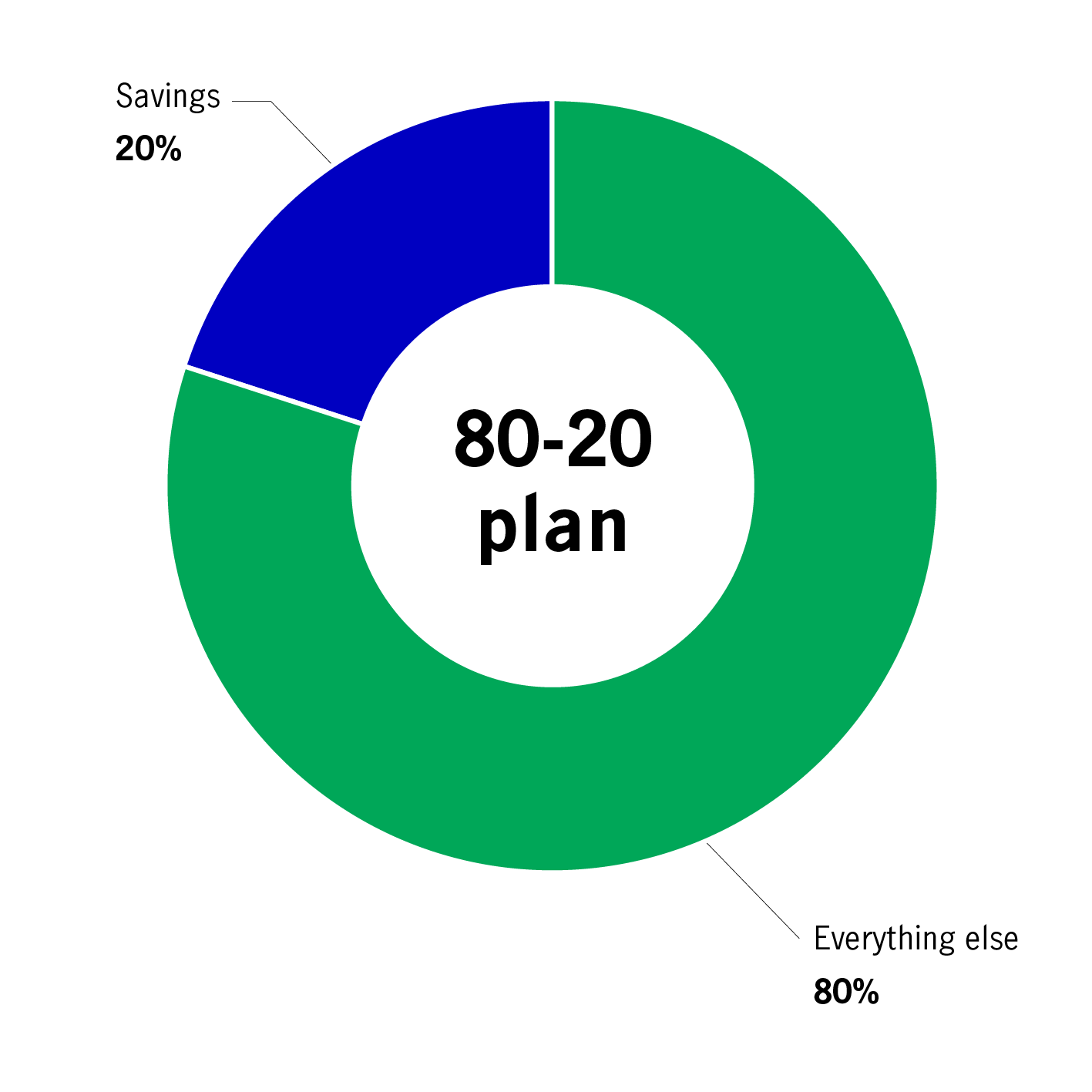

Even simpler than the 50-20-30 rule is the 80-20 plan. Instead of separating every expense into what’s essential and what’s not, you take 20% of your monthly income and deposit it directly into a savings account. What’s left over is available to spend however you want.

A good tip here: create an automatic transfer that sets aside 20% as soon your monthly salary is paid. By immediately placing the cash in a separate savings account, it’s like you never had it in the first place!

Everyone’s budgeting needs are different. That’s why it’s sometimes better to create your own method. Start by calculating all your monthly expenses. Check your bank statements to make sure you’re noting everything down. Mortgage or rent costs are easy to remember, but subscriptions, such as streaming services or phone contracts, may slip through unnoticed. And remember to account for payments that come off less regularly, such as annual fees.

Once you know how much you spend, a quick calculation will tell you what’s left each month. This is easy when you have a regular salary but could be a little harder to determine if you have a freelance job or get extra funds from other work, rental income, or interest payments.

Quick Budgeting Checklist:

Once you’ve counted up all these numbers, you can decide where your money will go each month and how much disposable cash remains.

Remember, it’s important to monitor your expenses on an ongoing basis. Save all your receipts and cross check them against your card statements at the end of the month. See if you’re overspending in certain areas or if you can save a little more.

Keeping an eye on income and spending is not easy. However, working to a budget can simplify matters. Once you have established a reliable system that tracks your money, the process becomes less tricky, and you’ll find it easier to take control of your finances.

Source: John Hancock

How much do I need to save?

Find out more by using our target savings calculator!

Real assets and the infrastructure behind AI

Artificial intelligence (AI) is often positioned as a story of models and applications, but its growth depends heavily on something far more tangible. Real assets such as data centres, power grids, and raw materials form the physical that supports AI development. As structural forces reshape the investment landscape, real assets are emerging as an enabler of the AI buildout.

The engine behind AI: Semiconductors are fuelling the next era of technology

Semiconductors belong to one of the most specialised yet globally integrated industry chains. From design, equipment, and materials to manufacturing and commercialisation, the production of a smartphone chip alone spans many countries across continents, creating tremendous opportunities for companies, consumers, and investors. With semiconductors increasingly becoming the backbone of an artificial intelligence (AI) race few are prepared for, understanding this sector is key to unlocking where the next wave of technology competition is heading.

AI innovation: Asia helps build many of the world’s technologies behind it

When electricity first arrived, the world built the necessary infrastructure – power plants, transmission lines – before the real transformation could take hold. A similar process is happening with artificial intelligence (AI). Today's massive investment in chips, data centres, and power grids is laying the foundation for a potential expansion in AI application that could take years to develop. In our view, the discussion is increasingly shifting from whether AI adoption will continue to how the enabling infrastructure is being built. Asia appears to be playing an important role in that development.

How much do you know about rates?

Recognise the different terms related to interest rates and understand how much yield global government bonds can offer.

Four essential keywords related to interest rates

Central banks in some emerging and Asian markets have started to hike rates, but deposit rates may not necessarily move in tandem. This would gradually erode depositors’ purchasing power in an inflationary environment. To achieve potential returns that beat inflation, deposit-focused investors should base any investment decisions on their risk tolerance levels and wealth management objectives.

Why demographic change requires a new set of cards

Many Asian governments are considering incentives to encourage larger families. These evolving policies will be vitally important, as the region looks to sustain a fast-greying population.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited