7 February, 2020

Fiona Cheung, Head of Credit, Asia

The outbreak of the 2019 novel coronavirus (coronavirus) has negatively affected regional economies and financial markets. In this investment note, Fiona Cheung, Head of Credit, Asia, assesses the current and expected impact of the coronavirus on regional credit markets, focusing on Chinese, Indonesian, and Indian credits. Cheung highlights that during volatile markets, proprietary credit research is important to set investors apart and stringent security selection rises in importance.

The coronavirus outbreak remains a highly fluid situation. Scientists hypothesise that the pathogen is highly contagious, and many aspects of its transmission are still unknown1 . Our base case is built on the assumption that it could take the authorities three-to-six months to contain and stabilise the situation. China’s economy and credit markets are expected to face short-term pressure, while the impact on regional credits should be more limited.

If the coronavirus becomes a global pandemic that drags on beyond a three-to-six month period, then the financial and economic shock could be more significant. This scenario would have a materially adverse impact on China and potentially other parts of the world with service industries facing severe losses.

Due to a notable increase in reported coronavirus infections over the Lunar New Year holiday, most provinces of China will extend the holiday until at least 10 February. As for Hubei province, where the coronavirus outbreak is the most severe, the province is expected to remain in administrative lockdown for most of February, if not longer.

Given the severe disruption to national transportation networks and suspension of domestic supply chains and production, we expect a significant slowdown in China’s economy in the first quarter of 2020 (year-over-year). Overall, we estimate that China’s GDP growth may fall below 5% in the first quarter of 2020, reaching a range of 4.5%–5%.

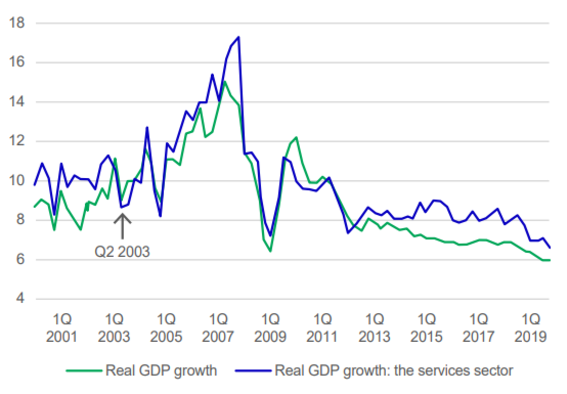

The impact of the coronavirus on second quarter growth and beyond will depend on how quickly China can contain the situation. However, judging from the 2003 SARS experience, we expect abovetrend growth to resume in the second half of 2020 (see Figure 1), assuming our base case scenario holds. We believe the Chinese government’s announced fiscal support measures and the People’s Bank of China’s injection of more than RMB$1 trillion into the financial system in early February should help mitigate the economic slowdown in the first half, as well as help catalyse a post-epidemic recovery2 .

Global Equity Diversified Income (GEDI) Fund: Staying selective through market volatility

Global equity markets have recently experienced greater volatility. Much of this has been driven by earnings announcements from AI hardware, semiconductor and large cloud-computing companies. Concerns about potential interest rate hikes have also added to investor uncertainty. After a prolonged period of strong performance in AI-related areas, market expectations have become demanding. Even companies reporting solid results have experienced sharp share-price moves when their outlook has only met, rather than exceeded, investor expectations. Against this backdrop, the GEDI Fund remains focused on its core objective: generating income while maintaining diversified exposure to potential capital growth.

Real assets and the infrastructure behind AI

Artificial intelligence (AI) is often positioned as a story of models and applications, but its growth depends heavily on something far more tangible. Real assets such as data centres, power grids, and raw materials form the physical that supports AI development. As structural forces reshape the investment landscape, real assets are emerging as an enabler of the AI buildout.

The engine behind AI: Semiconductors are fuelling the next era of technology

Semiconductors belong to one of the most specialised yet globally integrated industry chains. From design, equipment, and materials to manufacturing and commercialisation, the production of a smartphone chip alone spans many countries across continents, creating tremendous opportunities for companies, consumers, and investors. With semiconductors increasingly becoming the backbone of an artificial intelligence (AI) race few are prepared for, understanding this sector is key to unlocking where the next wave of technology competition is heading.

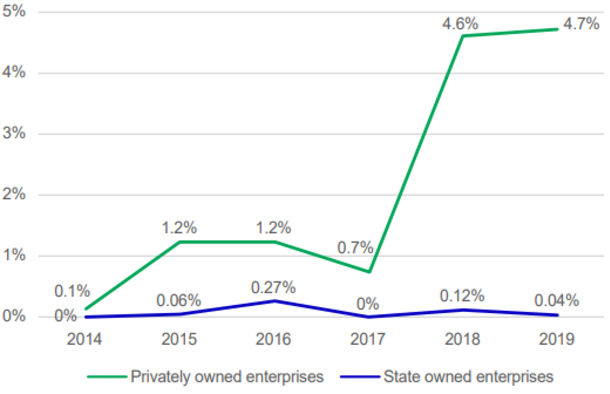

As a result of the virus outbreak’s economic impact, we expect to see a further rise in credit defaults (see Figure 2). They should remain elevated in 2020, driven by a structural economic slowdown and tighter liquidity for private-owned enterprises (POEs) under the coronavirus outbreak. We also believe there will be an uptick in defaults by those near-distressed POEs, some non-performing stateowned enterprises (SOEs), and weaker local government financing vehicles (LGFVs), in view of the mounting maturity wall in the offshore US dollar bond market in 2020 and 20214 .

However, our view is that the central government will adopt measures to prevent a sharp increase in the default rate, such as cuts to bank reserve ratio requirements (RRR) and market-liquidity operations. These moves will help to ensure stability and restore confidence, at least in the nearterm. We also believe further policy stimulus and system liquidity will likely be directed to strategically-important SOEs and LGFVs to boost growth through investment to mitigate the impact from a weak service sector.

By sector, Macau gaming credits should face shortterm pressure, as the number of visitors to the special administrative region has declined sharply. Property developers will likely fare better, as the Lunar New Year is traditionally a slower time for purchases. We also envisage that pent-up demand will help developers to regain lost ground in the second half of the year, if the virus outbreak proceeds according to our base case.

Finally, the impact on the financial sector should be relatively limited, as the sector’s loan exposure to affected cyclical businesses, such as hotels, restaurants, and the retail sector, is limited. Additionally, the banking sector boasts a higher capitalisation ratio compared to the 2003 SARS outbreak, which should serve as a cushion against a potential uptick in non-performing loans.

Beyond China, we expect a limited impact of the coronavirus on regional credit markets such as Indonesia and India, which have more domesticallydriven economies.

In Indonesia, there have been no reported cases of the coronavirus6 . The sovereign's fundamentals remain sound, and we expect the country to deliver steady GDP growth this year amid muted inflationary pressures. On the currency front, Bank Indonesia remains open to further rate cuts dependent on the economic situation. The rupiah has been strong relative to other Asian currencies, as well as appreciating against the US dollar year-to-date7 .

By sector, most utility, telecom, and SOE credits' have resilient business models and government support remain s unchanged. Also, developers are benefiting from the steady demand for self -use properties and a rise in industrial land sales due to the global realignment of the suppl y -chain.

We also see a narrow impact on India. With three reported case s in the country8 , the crucial issue now is virus containment to avoid it becoming a community -transmitted infection. On the policy front, the government’s Union Budget (Fiscal Year 2020 – 2021) , announced last week , saw a fiscal deficit that was mostly in line with expectation s, which should keep the rating agencies at bay , for now. Activity in India’s manufacturing sector hit an eight -year high in January9 , indicating ample near -term domestic economic strength.

We are aware of the potentially negative impact arising from the coronavirus outbreak , and it will serve investors’ interest by actively managing their exposure through the sizing of the positions , and trimming or exiting more vulnerable and high - beta /high -yield names.

What’s more, investors shall closely monitor development s, assessing their impact and adjusting their investment view accordingly. While we expect default rates to rise and remain elevated in China, propreit ary credit research is important to set investors apart, as stringent security selection and proactive risk -management processes rise in importance. These fac tors should be able to help investors ride through the negative shock over the short term.

1Source: The outbreak of novel coronavirus appears more contagious than seasonal flu and is on par with SARS in 2002 and 2003, studies say”, Wall Street Journal, 2 February 2020.

2Source: “PBOC vows to maintain ample liquidity amid coronavirus outbreak”, Bloomberg, 2 February 2020.

3Source: Wind and Nomura Global economics (January 29, 2020)

4According to Bloomberg Intelligence, US$ 17 billion and US$ 26 billion of LGFV overseas bonds are due to mature in 2020 and 2021, respectively. Bloomberg, 5 February 2020.

5Source: Wind, Bloomberg, and Goldman Sachs.

6As of 3 February 2020.

7Bloomberg, 5 February 2020.

8As of 5 February 2020.

9Source: Bloomberg, 2 February 2020.

Global Equity Diversified Income (GEDI) Fund: Staying selective through market volatility

Global equity markets have recently experienced greater volatility. Much of this has been driven by earnings announcements from AI hardware, semiconductor and large cloud-computing companies. Concerns about potential interest rate hikes have also added to investor uncertainty. After a prolonged period of strong performance in AI-related areas, market expectations have become demanding. Even companies reporting solid results have experienced sharp share-price moves when their outlook has only met, rather than exceeded, investor expectations. Against this backdrop, the GEDI Fund remains focused on its core objective: generating income while maintaining diversified exposure to potential capital growth.

Real assets and the infrastructure behind AI

Artificial intelligence (AI) is often positioned as a story of models and applications, but its growth depends heavily on something far more tangible. Real assets such as data centres, power grids, and raw materials form the physical that supports AI development. As structural forces reshape the investment landscape, real assets are emerging as an enabler of the AI buildout.

The engine behind AI: Semiconductors are fuelling the next era of technology

Semiconductors belong to one of the most specialised yet globally integrated industry chains. From design, equipment, and materials to manufacturing and commercialisation, the production of a smartphone chip alone spans many countries across continents, creating tremendous opportunities for companies, consumers, and investors. With semiconductors increasingly becoming the backbone of an artificial intelligence (AI) race few are prepared for, understanding this sector is key to unlocking where the next wave of technology competition is heading.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited