26 January 2023

Paula Chan, Senior Portfolio Manager, Asia Fixed Income

Isaac Meng, Portfolio Manager, Asia Fixed Income

2022 saw fixed income managers’ investment process tested to the extreme – probably unseen in the last 30 years. Yet, despite the unprecedented conditions, our risk management and portfolio construction processes served us well – particularly when the market experienced deep drawdowns. In this 2023 outlook piece, Paula Chan, Senior Portfolio Manager, Asia Fixed Income, and Isaac Meng, Portfolio Manager, Asia Fixed Income, explain why China's favourable policy climate coupled with attractive long-term fundamentals, could help onshore and offshore China fixed income harvest positive returns in the 12 months ahead.

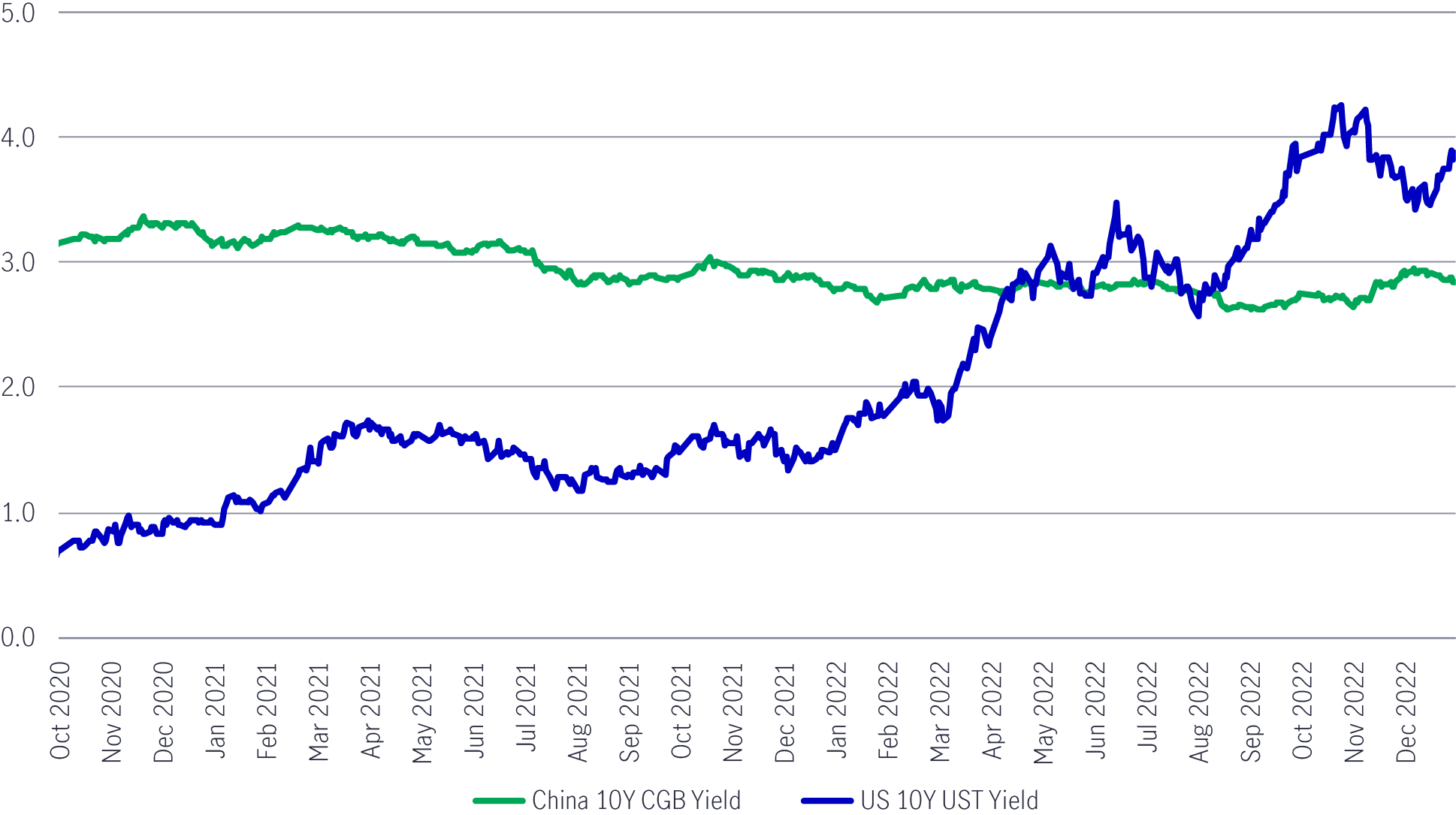

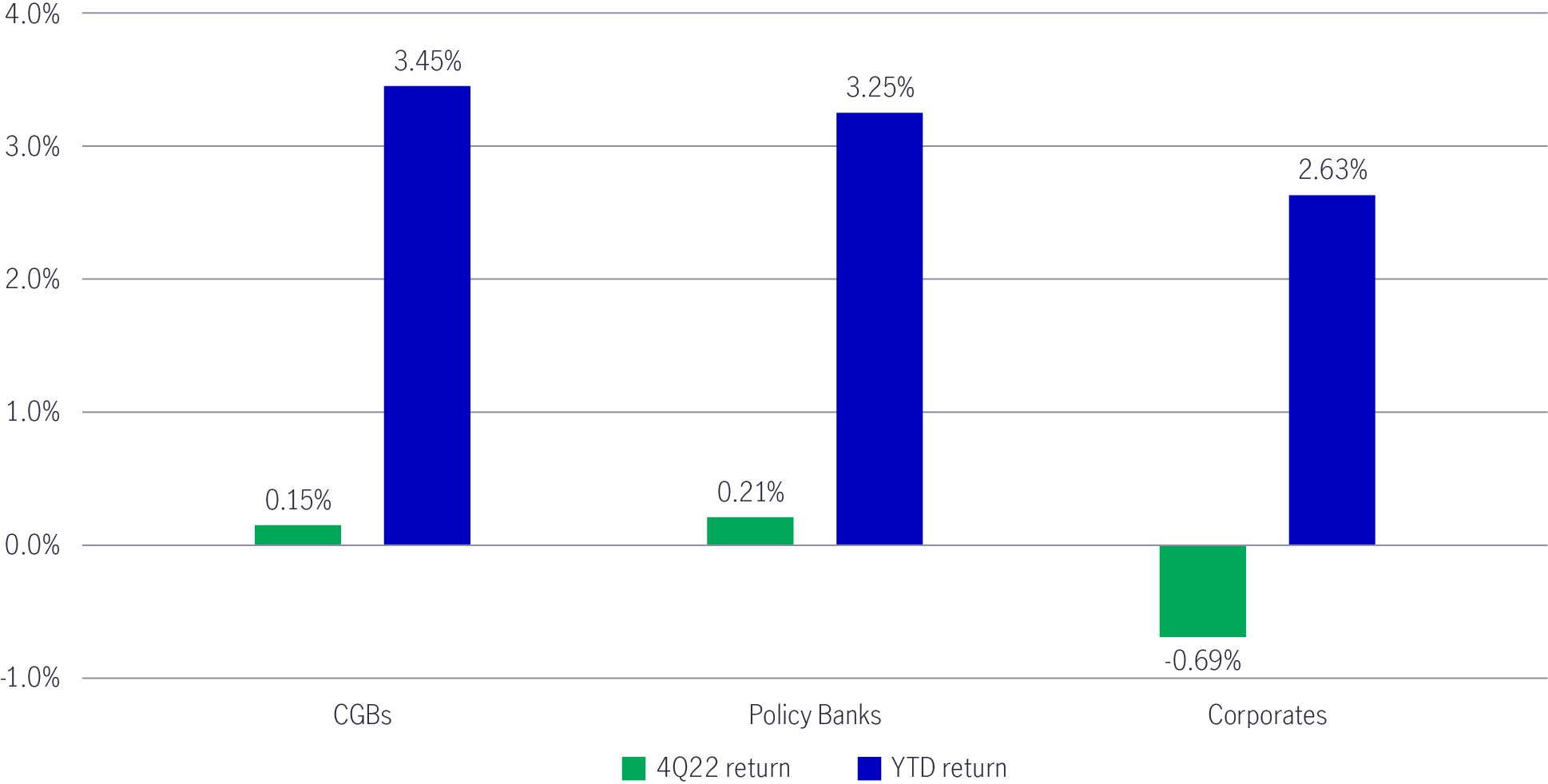

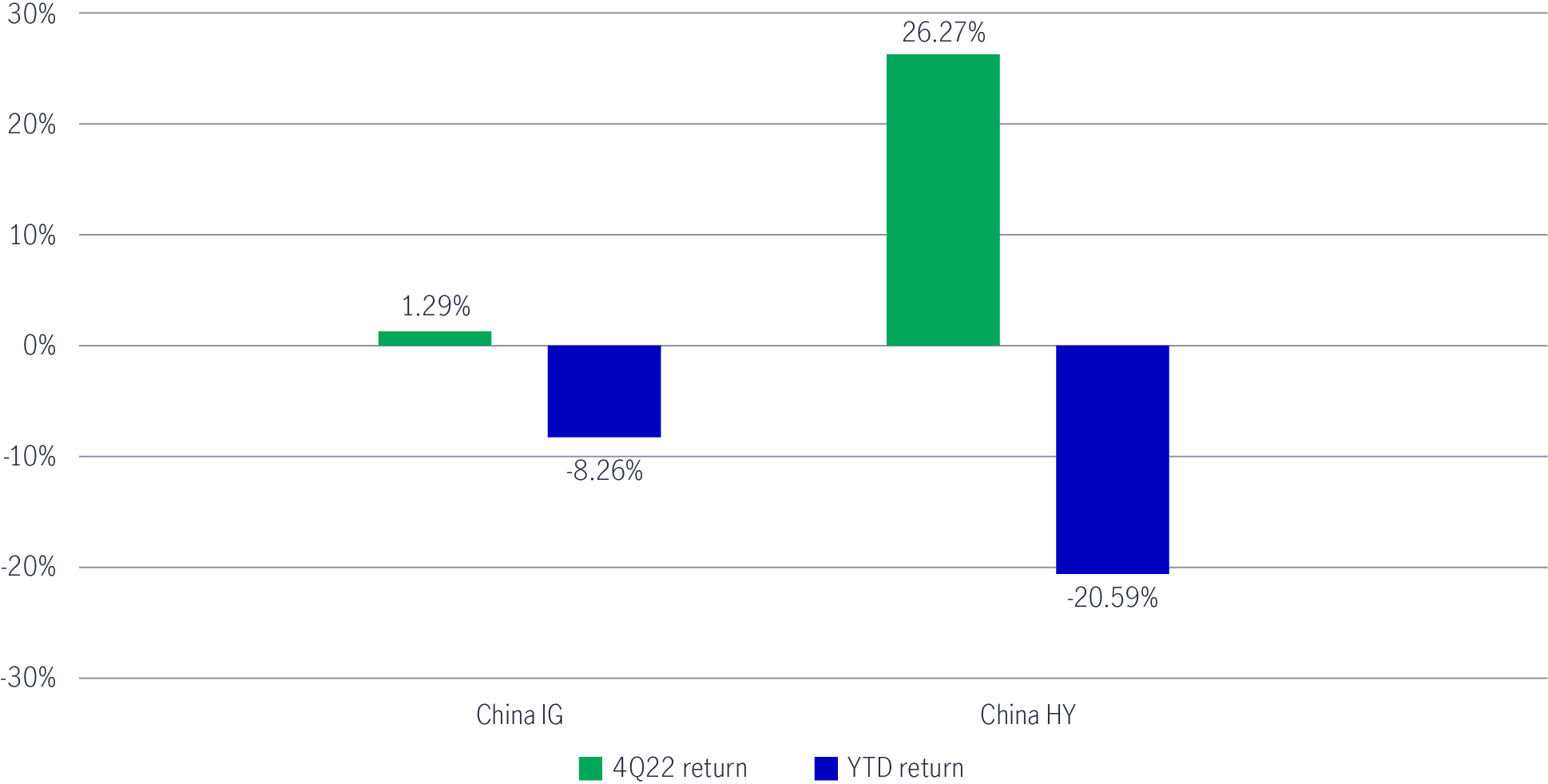

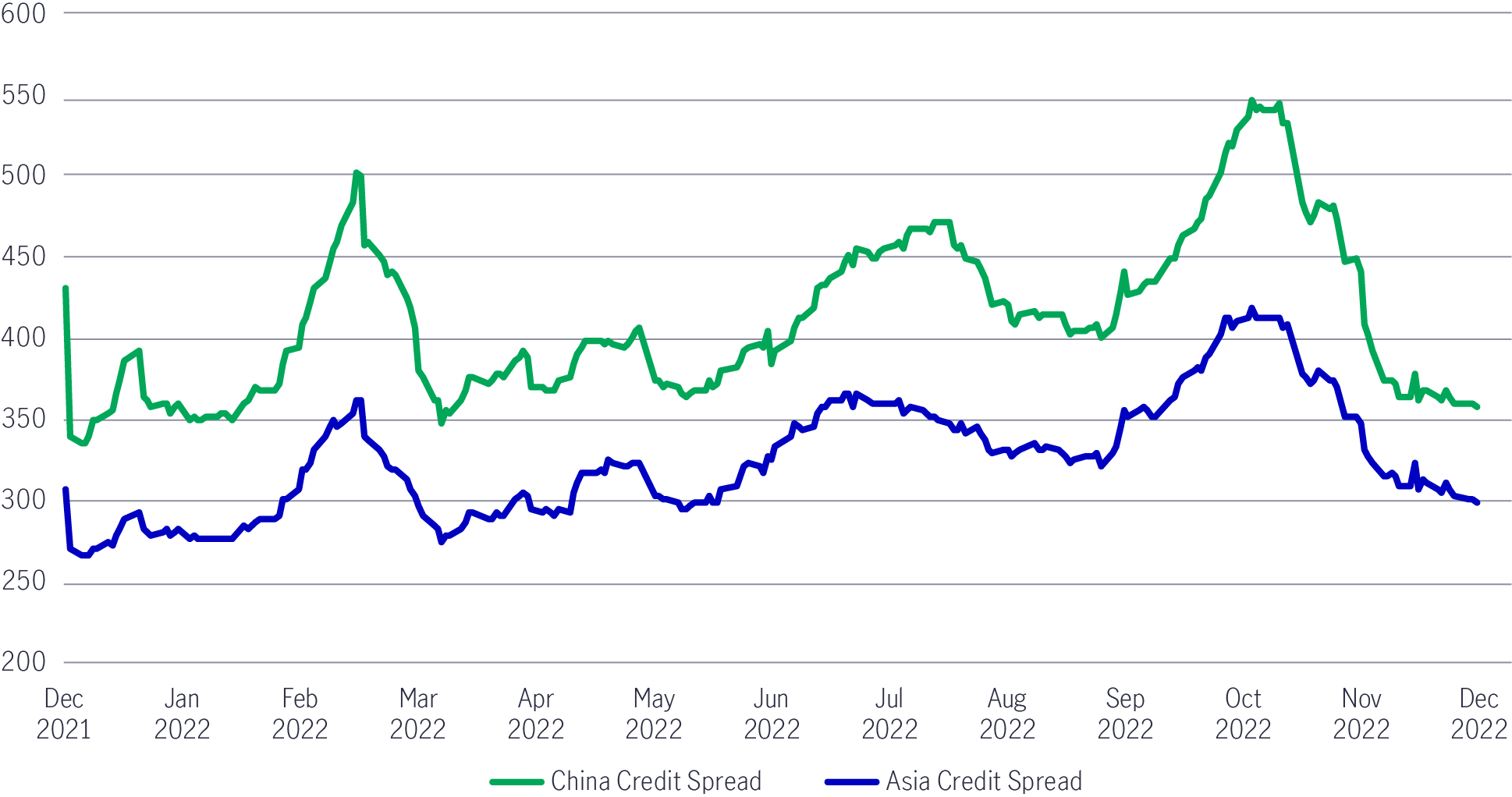

Against a volatile backdrop, onshore China bonds still managed to outperform most of their global peers in 2022 due to their liquidity buffer, lower correlation with other global fixed-income markets, and positive real yields. Indeed, “easing” has been the main tune for China’s monetary easing policies in 2022 (see Appendix). Offshore China bonds, however, were being dictated by another set of dynamics: they were notably impacted by ongoing issues in the property sector, hence the sharp correction seen among high-yield names in this space.

Key highlight of market performance1:

Towards the fourth quarter of 2022, a major shift to ease COVID restrictions and property sector policies boosted market sentiment. In our view, these measures should help the sector find a bottom over the next 12 to 18 months. We’ll detail our outlook for China’s onshore and offshore bonds in the next section.

Moving into 2023, our investment positioning could be viewed as more constructive compared to the defensive stance assumed during the previous year. Indeed, as soon as China announced a double pivot with a major shift in China’s COVID and property sector policies, we started to reposition ourselves more offensively in the fourth quarter of 2022:

1. China’s border re-opening and loosening of COVID-measures

2. Strong policy bazooka with an “all in” effort to boost economic growth

3. All-in type of property-sector support to sustain a recovery of the real-estate sector

4. US Fed to gradually slow down rate hikes or pause in 2023

We foresee our more offensive stance will continue to benefit from these macro and policy tailwinds operating throughout the fourth quarter of 2022 into the new year, as markets have not fully priced in the positive factors and the potential of underlying improvement of fundamentals. Moreover, the advanced reopening of some Asian economies continues to be a positive factor and one that is not fully priced in.

After announcing the zero-COVID fine-tuning (“20 measures”) in November 2022, late December saw China abolish hotel quarantine and on-arrival PCR testing requirements for inbound travellers starting from 8 January 2023. On 27 December, the government further announced that it would resume issuing tourist and business visas for Chinese mainland residents visiting Hong Kong and begin reopening sea and land ports.

We believe that China’s COVID U-turn paves the way for a shift to a strategy of living with the virus, which paves the way for resuming both inbound and outbound travels in the first half of 2023. Whether the return to normality will be gradual or abrupt is still subject to the surge of infections and the potential impact on supply chains. At the time of writing, the real growth rate of gross domestic product in China is forecast at 3.0% in 2022, followed by 4.8% in 2023 and 5.0% in 20242.

As the market now expects improved economic growth in China that may lead to a moderate rebound in inflationary pressures and higher onshore rates, we could see the onshore yield curve steepen. At the same time, the CNY might strengthen in the foreign exchange market. Therefore, having an underweight exposure to duration in our onshore CNY bond portfolios should help buffer the impact of rising rates.

Turning to the foreign exchange space, the CNY will likely benefit from the domestic economic recovery, more substantial policy stimulus, and a USD that may be peaking in value. Higher rates would also attract portfolio flows to the onshore markets as the interest rate differential between the CNY and USD should narrow, providing support to the renminbi. Therefore, we believe that the outlook for the renminbi is more constructive, and investors could benefit from a reduction of CNY hedges against the USD.

Regarding different segments of China bonds in the onshore market, we maintain a relatively cautious view of corporate credit and bank capital bonds as valuations appear unattractive. We are more neutral on policy bank bonds and China government bonds. Simultaneously, as we seek to benefit from China’s reopening theme, there is the potential to increase our offshore China USD high-yield exposure due to the latter’s attractive valuations. From a sector perspective, we are looking to selectively add higher-quality property developers, especially SOE developers that benefit from greater state support. We have also added some exposure to internet and technology names that are well-positioned to gain from a domestic recovery.

As a team, we always try to position the portfolio to reflect environmental, social, and governance (ESG) factors. Currently, the opportunity set for sustainable investing remains predominantly in the offshore USD market. However, once the onshore green-bond market develops further and becomes more scalable, it could offer multiple investment possibilities.

In the new year, we expect more supportive measures for the property sector following the financing support announced (“second arrow”) in November 2022. Significantly, in early January, the People’s Bank of China (PBOC) and the China Banking and Insurance Regulatory Commission (CBIRC) announced a bold new initiative to establish a new mortgage rate adjustment framework for first-time home buyers when housing prices drop. This will likely result in a material decline in these buyers’ mortgage rates and will be supportive for the property sector. At the same time, market headlines suggest that China is considering relaxing its stringent “three red lines” property rules for some developers. If implemented, this would represent a significant policy shift and likely build investor confidence in the sector.

Indeed, the recovery story depends on how quickly developers can reinstate cash flow. But as the economy reopens, there may be an uptick in household incomes that, in turn, should result in increased property transactional activity. A headwind to note is the slowdown in the US and Europe could have a knock-on effect on China’s export manufacturing sector, which may affect employment levels. Overall, the recovery should be quite meaningful in the second half of 2023 but possibly less robust (a U-shaped rebound) than the post-COVID upturn (a V-shaped rebound) in 2020.

The government and policymakers will be mindful of the aforementioned factors and likely observe how the reopening plays out before considering further fiscal stimulus. In terms of official benchmark interest rates, these should remain on hold, with no changes expected until late 2023, which could coincide with the US Federal Reserve (the Fed) reaching its terminal interest rate. Indeed, we may have already reached the maximum interest-rate policy differential between the PBOC and Fed. So, as China reopens and the Fed is in the latter stages of its tightening cycle, currency depreciation pressures have probably peaked. As we have detailed earlier, China bonds serve as a potentially resilient risk diversifier due to low correlation to other parts of the global fixed-income market, decent interest-rate carry (on a hedged basis) and abundant onshore liquidity.

When we look back at the challenging market environment in 2022, one of the key takeaways we want to emphasise is the need to maintain a highly liquid portfolio – either with cash or equivalents, such as short-term Treasuries, during such periods of market turmoil. Our investment team’s long track record and deep experience in China's onshore bond market3 have helped the team navigate treacherous market conditions. By adopting a higher level of liquidity under such conditions, investors are able to methodically manage their way through a volatile market cycle. At the same time, maintaining a diversified portfolio can further reduce the downside impact.

In summary, we believe liquidity and diversification remain essential, as do perseverance and patience.

Lastly, we expect low-to-mid single-digit returns for CNY onshore bond investors in this space and reiterate the appeal of the China bond asset class to global investors.

First quarter: the PBoC lowered its policy rates by 10 basis points, including the 7-day repo rate from 2.2% to 2.1% and the 1-year MLF interest rate from 2.95% to 2.85% on 17 January. This was followed by a reduction in the banks’ loan prime rate (LPR) which was reduced by 10 basis points to 3.70% for the 1-year rate and by 5 basis points to 4.6% for the 5-year rate.

Second quarter: China reduced the RRR by 0.25% in April with the average RRR in the banking system falling to 8.1% from 8.4%. The PBoC also cut the 5-year LPR by 15 basis points to 4.45% to boost mortgage support while leaving the 1-year LPR unchanged at 3.70%.

Third quarter: The PBoC cut policy rates (1-year medium loan facilities (MLF) and 7-day reverse repo rate) by 10 bps to 2.75% and respectively in August. This was followed by asymmetric cuts in Loan Prime Rates with the 1Y LPR reduced by 5bp to 3.65% while the 5Y LPR was cut by 15bp to 4.3% to support the property market.

Fourth quarter: The PBoC announced a universal Reserve Requirement Ratio (RRR) cut on 25th November.

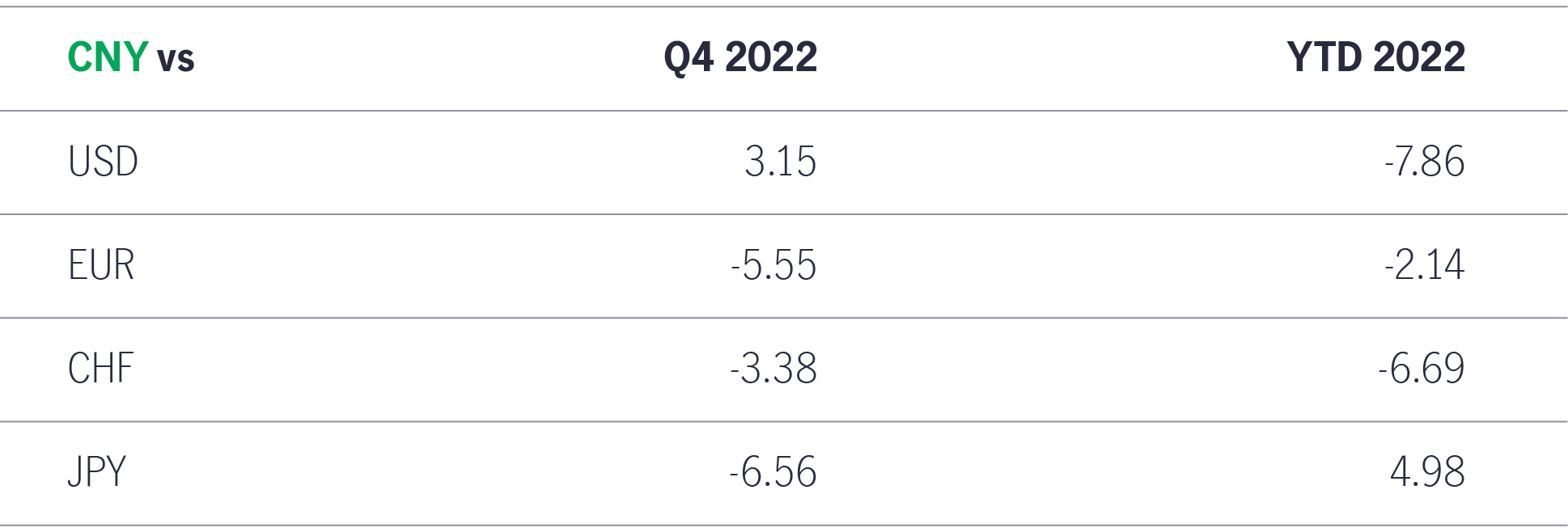

2022 Market review

China onshore rates (%)

Credit

Renminbi

China USD credit - returns (%)

China USD credit (spreads, basis points)

Source: Bloomberg, Manulife Investment Management, as of 30 December 2022. It is not possible to invest directly in an index. Past performance does not guarantee future results.

1 Bloomberg, data as of 28 December 2022. USDCNY was as high as 7.3050 on 31 October 2022 and depreciated to 6.9501 as of 28 December 2022.

2 Based on Bloomberg consensus forecasts.

3 We established our Onshore China Bond performance track record in 2010.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited