5 October 2021

Winson Fong, Senior Portfolio Manager, Greater China Equities

Concerns about potential defaults by real-estate developers have triggered risk aversion in the market, prompting a sell-off in property-related stocks. However, “real estate” is a broad term encompassing residential, shopping malls, and retail properties, with considerable regional differences. In this Investment Note, Winson Fong, Senior Portfolio Manager, Greater China Equities, discusses the implications of the current debt crisis for equity investors, as well as various opportunities in the Greater Bay Area (GBA).

Investors should first understand an important fact: the real estate sector has long been a focus of the Chinese government. From 2016 onwards, it has reiterated at high-level meetings that “residential properties are for housing, not for speculation.” Numerous policies have since been implemented to curb real-estate speculation (excluding moves to combat COVID-19 last year). This has included enforcing the “three red lines” policy1 in 2020 and 2021 to discourage real-estate speculation through excessive borrowing by developers.

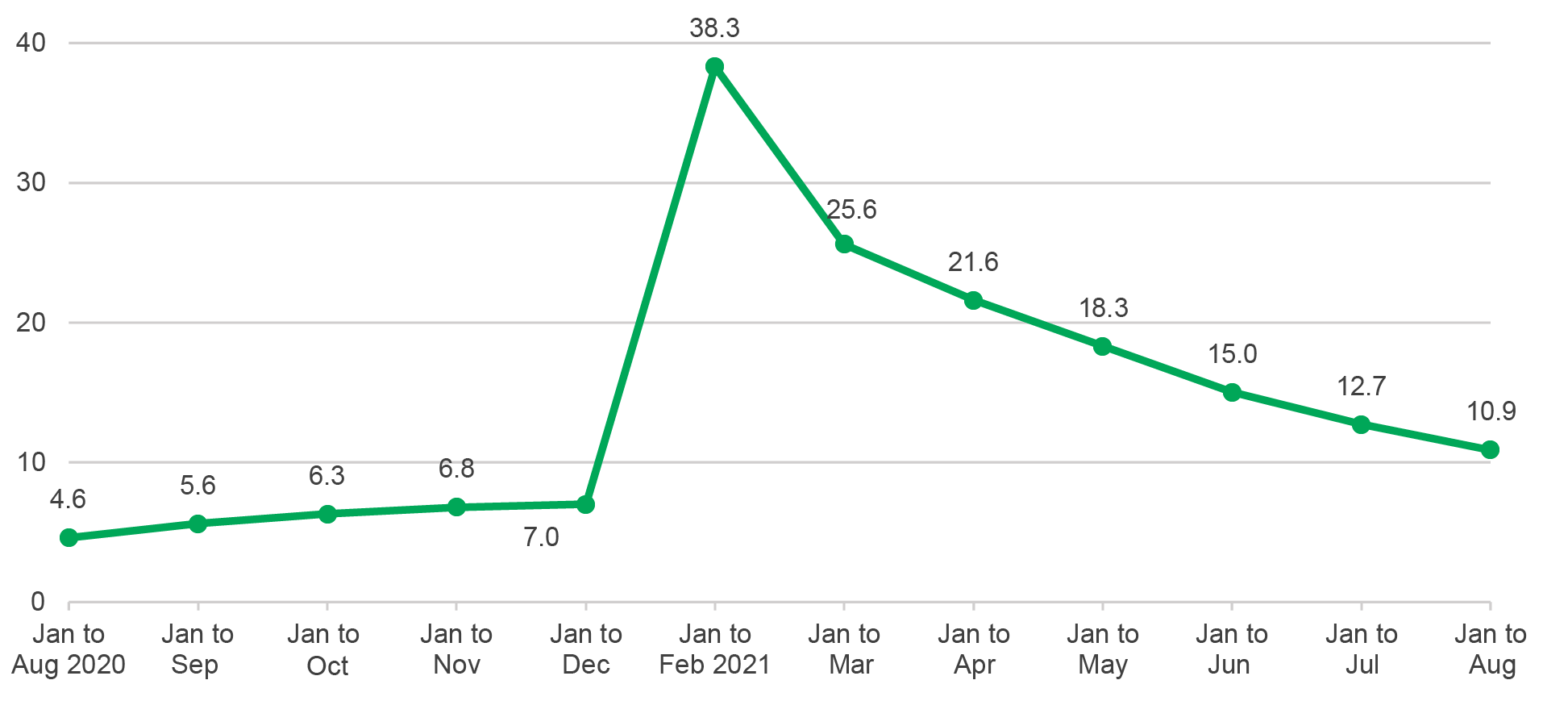

In fact, deleveraging and reducing the financial risks related to real estate have been the government’s primary objectives over the past two years, while investment in the industry has steadily retreated from its peak at the start of 2021.2

Chart 1: Growth rate (%) of investments in real estate development nationwide2

In terms of systemic risk, we believe that the likelihood of credit events at state-owned and private real-estate companies causing a domino effect is rather low. While some might compare the collapse of Lehman Brothers to the latest real-estate debt crisis, the former was an unexpected development; whereas the latter was a gradual process that unfolded over time.

Given today’s era of big data and internet technology, regulators have become much more proficient at anticipating and adapting to change. Meanwhile, the central government has been preparing the property sector for deleveraging in advance. It’s also important to recognise that the real-estate developers’ price-to-book ratios are at wide discounts, implying that their valuations have fully reflected the negative impact from credit crunch caused by deleveraging. The banks’ overall non-performing loan provision coverage is almost 200%3, a solid level far exceeding the required 120%-150% by China Banking Regulatory Commission (CBRC). We believe that there is no need to worry too much about systemic risks like those during the Lehman crisis.

As such, we think that the negative impact of the event on non-performing loans should mainly affect selected banks. Furthermore, the bad news is, to a certain extent, already reflected in the share prices of financials.

Concerns from the market and investors are inevitable, and we remain vigilant of volatility in the real-estate sector over the next three to six months. However, we believe that the real estate sector should come out from this period unscathed and follow a healthy growth trajectory. In our view, market information can be hard to follow at times, so individual investors should seek advice from investment professionals with good research capabilities, especially those who have witnessed many financial crises over the years and understand the characteristics of each crisis.

Monetary and fiscal policies will generally remain tight. There may be some moderation in regulatory tightening at the year-end Central Economic Work Conference, but since the outbreak of COVID-19, the central government has taken a focused approach by directing resources into strategic industries and providing targeted sector support to those areas closely related to investment and consumption.

It is worth noting that since the pandemic, quantitative easing and the printing of money have instilled international markets with confidence. Yet, such measures may not apply to China. First, printing money could create hot money and lead to speculation. Furthermore, suppose the pandemic persists or worsens. In that case, another round of expansionary (not tapering) measures to bail out markets and see the crisis through may not be possible, hampering the recovery of the external economy. In our view, under this scenario, China’s policy approach may be more favourable, so tighter macroeconomic policies will not be easily changed at this time.

Upstream, midstream, and downstream industries linked to the residential sector are more fragmented. Should they require central government support, this could be similar in structure to the measures implemented during the pandemic, such as allowing the delayed payment of loans and a series of initiatives targeted at helping SMEs.

For the real-estate industry, we believe that those financially sound companies may use this opportunity to expand and consolidate, resulting in the strong becoming stronger. Property-management businesses with stable operations have already faced sell-off pressures, but their stock prices rebounded sharply after markets calmed. In addition, the Hang Seng TECH Index has stabilised after undergoing a substantial correction in the third quarter of 2021. This was possibly due to capital flowing back into bellwether tech stocks (which had fallen by 40%-50%) from old-economy stocks (such as finance and real estate) after a period of risk aversion.

It is worth noting that real-estate developers in the GBA are primarily diversified businesses with stakes in commercial, hotel, and retail ventures, as well as residential projects. These developers have generally secured other financing channels, possess favourable fundamentals, and are in a better position than developers nationwide.

Aside from real-estate developers and property managers, there are also numerous real estate investment trusts (REITs) in the GBA. Thanks to macro-policy planning4 and investments in commercial activities (e.g., office buildings and shopping malls), REITs were more resilient when the developers sold off. REITs can be characterised as generating a potential income plus growth for investors due to their lower volatility profile than stocks, with an earnings yield that ranges from 6%-7%, making this asset class a well-rounded option.

Generally speaking, the Pearl River Delta region consists of solid fundamentals, stronger corporate governance and local demand which translate into better prospects of growth recovery.

First, we believe that the government encourages more diversified, institutionally managed investment products for domestic investors and actively promotes financial market innovation through connectivity.

Following the introduction of the Shanghai-Hong Kong Stock Connect (2014), Shenzhen-Hong Kong Stock Connect (2016), Northbound Scheme (2017), and Southbound Scheme (2021) for stocks and bonds – and after two years of planning, the Cross-boundary Wealth Management Connect scheme in the Guangdong-Hong Kong-Macao Greater Bay Area was launched on 10 September 2021, with service expected to begin as soon as mid-October 2021.

In general, the scheme will allow investors to conduct cross-boundary investments directly in RMB and can offer greater risk diversification among a wide range of investment products.

As previously mentioned, REITs are well-rounded (having both defensive and growth characteristics) investment options. In addition, REIT funds in Hong Kong can act as “super-connectors” between Hong Kong and the Mainland.5 REITs may choose to list in HK dollar or renminbi. Besides, the relevant authority has also suggested including REITs in the stock-connect programmes in the future. Once confirmed, investors on either side of the boundary can access each other’s eligible REITs via the stock-connect programmes. For overseas investors in Mainland infrastructure assets, the arrangements are expected to be implemented as a priority. Meanwhile, Mainland investors will have the opportunity to access Hong Kong and global real-estate projects.

We believe the Cross-boundary Wealth Management Connect Scheme will consist mainly of lower-risk products. When REITs can be accessed via stock-connect programmes, funds will likely increase their allocation to REITs, resulting in a potential market revaluation of the sector.

In recent years, international investors have taken a great interest in sustainable development. For real-estate developers, helping the government resolve social issues can be seen as an important contribution to the “social” aspect. As the community grows more vocal, we foresee social issues becoming more important in the city’s real-estate development. With an environmental, social and governance (ESG) platform, it can raise the transparency and communication of sustainability issues. Many developers are already providing updates on sustainable development in their investor relations updates and annual reports. They will likely receive more attention from markets on this topic in the future.

1 In 2020, PBOC and the Ministry of Housing and Urban-Rural Development announced new financing regulations for the real estate industry. Developers wanting to refinance are being assessed against three thresholds: a 70% ceiling on liabilities to assets, excluding advance proceeds from projects sold on contract; a 100% cap on net debt to equity; and a cash to short-term borrowing ratio of at least 1x.

2 National Bureau of Statistics, 15 September 2021.

3 The NPL coverage ratio was 182.23% as of end of 2020, “China Financial Stability Report”, People’s Bank of China, 3 September 2021; the ratio increases to 193.2% as of end of June 2021, according to JP Morgan estimates.

4 The area of Qianhai economic zone will be expanded from 15 km² to 120 km², which should benefit commercial activities in Shenzhen and Shekou.

5 17 September 2021, Financial Services Development Council.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited