26 May 2021

US bank portfolio management team

With each passing quarter since the pandemic began to disrupt the economy in early 2020 and the outlook for U.S. banks was upended, the industry has managed to successfully retrench and position itself to help lead the economy’s broader recovery. Nearly all publicly traded U.S. banks have released first-quarter results as of this writing, and the industry as a whole continues to exceed our expectations. Based on our analysis, here are nine salient points about the current state of banks and the implications for equity investors.

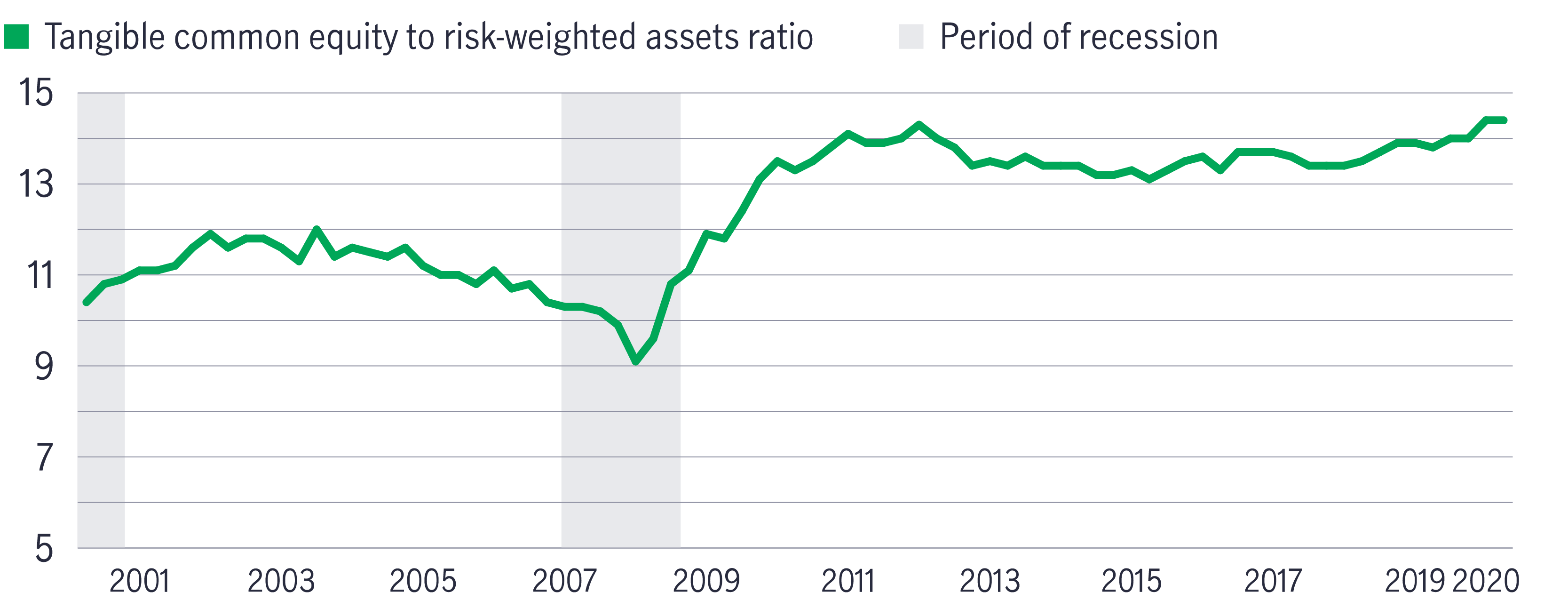

U.S. banks' capital levels have surged since a 2009 low

U.S. banks' ratio (%) of tangible common equity to risk-weighted assets, 2001–2020

Source: Federal Deposit Insurance Corp., January 2021. A tangible common equity to risk-weighted assets ratio is used to assess the potential for future bank financial stress based on commonly measured capital ratios.

U.S. banks appear to us to be fundamentally strong, with historically high levels of capital and liquidity. As the economy has reopened, credit fundamentals have been materially better than had been expected a year earlier. Strong results from regulators’ latest round of stress tests to assess major banks’ abilities to weather further economic shocks triggered a further loosening of restrictions related to share buybacks. We view these developments as a testament to the industry’s capital strength and improved underwriting. In addition, we believe that the most recent stimulus package that Congress approved in March should further support the economy and reduce credit costs. As these trends persist, we expect U.S. bank earnings to accelerate throughout 2021.

1 “KBW Bank Earnings Wrap-Up 1Q21, v. 2: Banks Continue to Deliver EPS Beats on Mostly Favorable Credit Trends,” Keefe, Bruyette & Woods, April 23, 2021.

2 Earnings per share (EPS) is a measure of how much profit a company has generated calculated by dividing the company's net income by its total number of outstanding shares.

3 U.S. Federal Reserve press release, March 25, 2021.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited