9 June, 2021

Frances Donald, Chief Economist

We’re entering a period where concerns about inflation have reached fever pitch. As such, inflation-related data releases are likely to be scrutinized closely for clues pertaining to what could happen next. In this market note, Frances Donald, Global Chief Economist and Global Head of Macroeconomic Strategy, shares her inflation outlook.

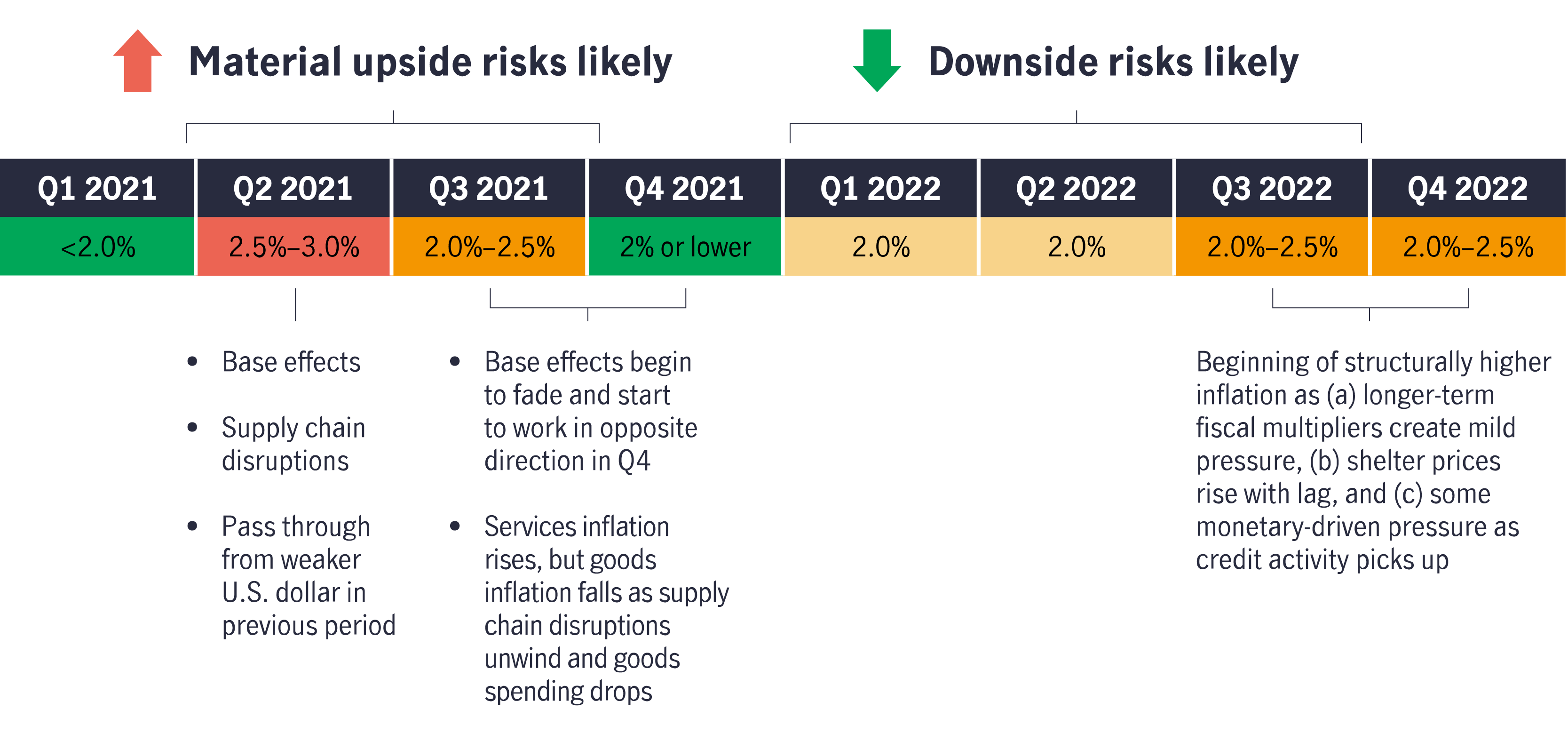

First, we expect to see a sizable pop in the already relatively elevated Consumer Price Index (CPI) readings, beginning with April’s 4.2% year-over-year rise¹—which is likely to head even higher in May. Throughout the end of Q2 and into the beginning of Q3, we’re also likely to encounter ongoing upside surprises across a host of price measures, from import prices to prices paid indexes in surveys.

Second, the pace of inflation should then begin to slow meaningfully in late Q3 2021 and continue into 2022 as the mismatch in demand and supply begins to ease. The handoff from goods price inflation to services price inflation, which typically takes some time, should also feed into that narrative. Crucially, we also expect labor supply to improve by late Q3, which should mollify concerns about wage pressures. This period should confirm that sizable increases in headline inflation were, indeed, transitory.

Finally, as we peer into 2023 and beyond, we see scope for slightly higher structural inflation (in the 2.0% to 2.5% realm versus the 1.5% to 2.0% range during the prepandemic period) as the delayed effects of higher shelter costs, infrastructure spending, lending activity, and medical costs translate into moderate longer-term price pressure.

Note that throughout our forecast period, we expect core inflation to remain below headline inflation (nearly all the time) and, crucially, within the U.S. Federal Reserve’s (Fed’s) average 2.0% inflation targeting mandate.

The United States isn’t an island—U.S. inflation is heavily correlated to global inflation, which remains muted. Notably, Chinese credit trends are consistent with future weaker inflation in China, which tends to filter through to U.S. inflation through trade and global forces. Crucially, the relatively weaker U.S. dollar has been an important contributor to inflation in the United States and signs of further weakness will translate into higher import prices.

US inflation outlook: an overview

Source: Manulife Investment Management, as of 13 May 2021.

1 U.S. Bureau of Labor Statistics, May 12, 2021.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited