Equity strategy:

Hong Kong and China Equities

Attractive valuations with structural opportunities

Strong fundamentals support Hong Kong and China equities

Learn moreChinese equities rebound

Learn moreCapture the benefits of re-opening and valuation recovery

Learn more

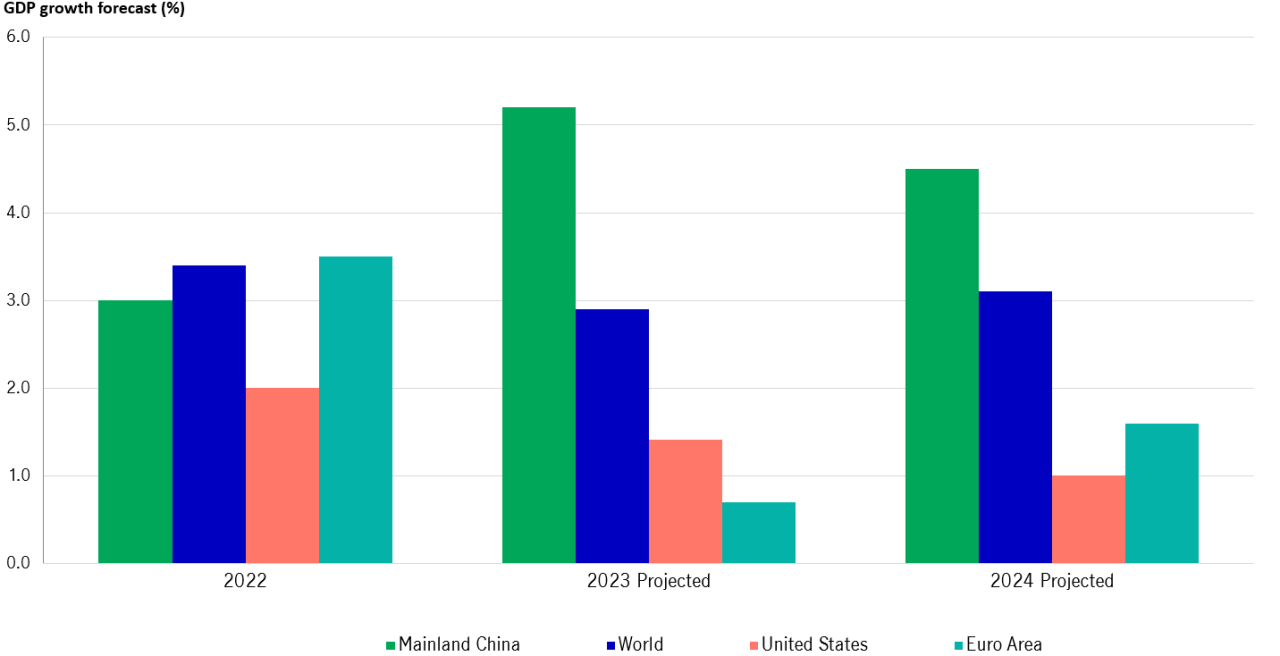

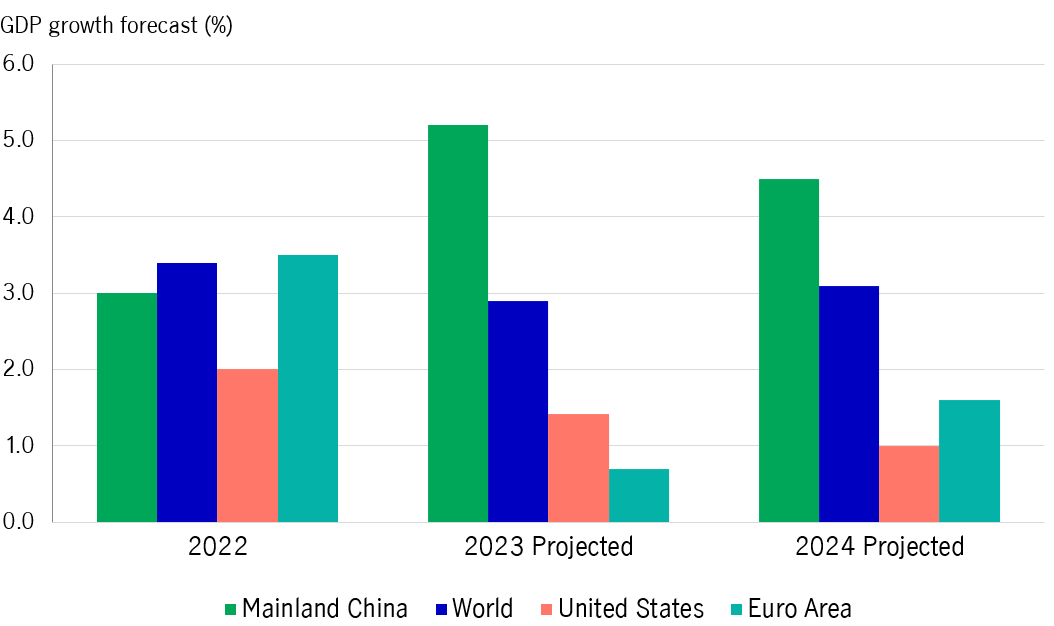

The ease of COVID control policy and the property support policy in 2022 Q4, could support the domestic economy. Latest forecast indicated China’s GDP to re-accelerate to 5.2% in 2023, contrary to the downward trend of major economies.

GDP growth forecast (%)1

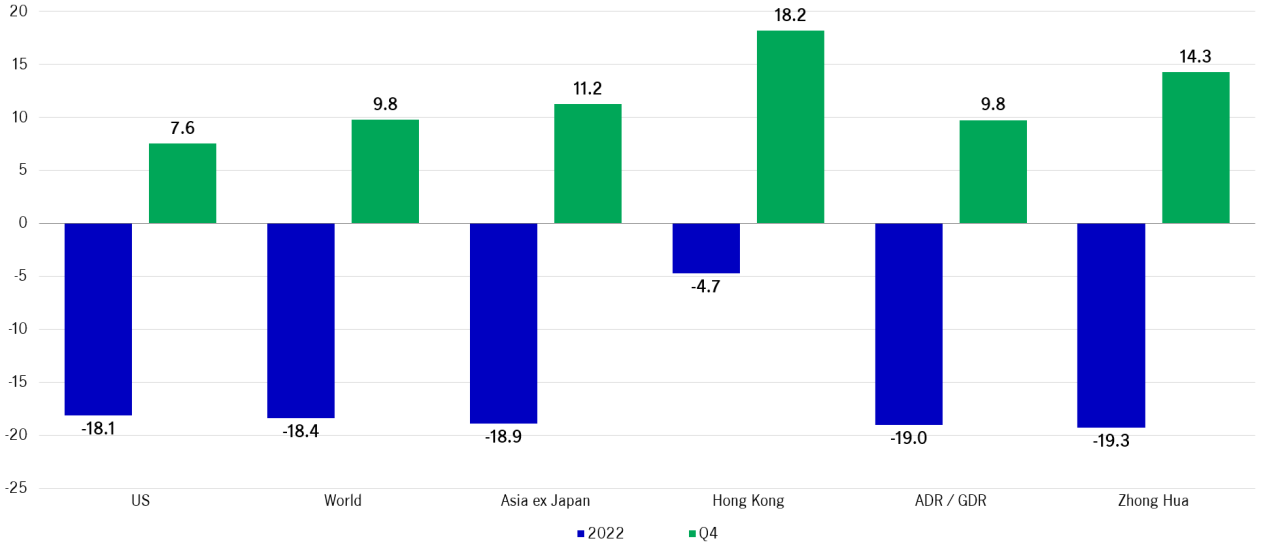

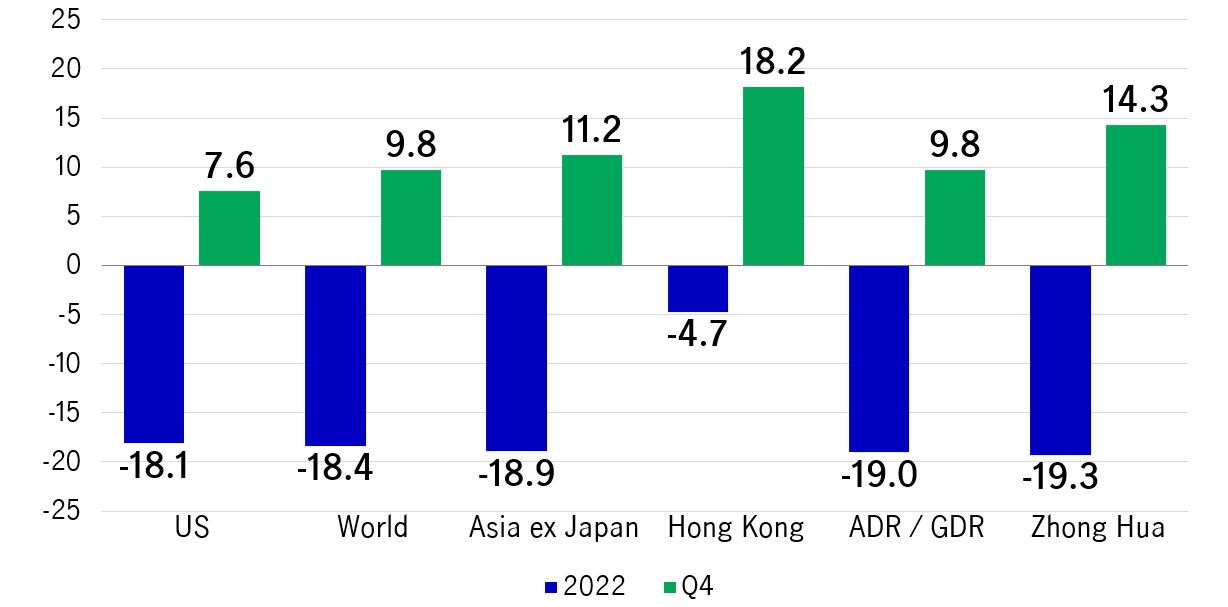

China equities rebounded and outperformed global markets in Q4 on the back of (1) removal of zero-COVID controls, (2) supportive measures for the property sector and (3) improved China-U.S. relations.

China and Hong Kong equities ourperformed other markets in Q4 20222

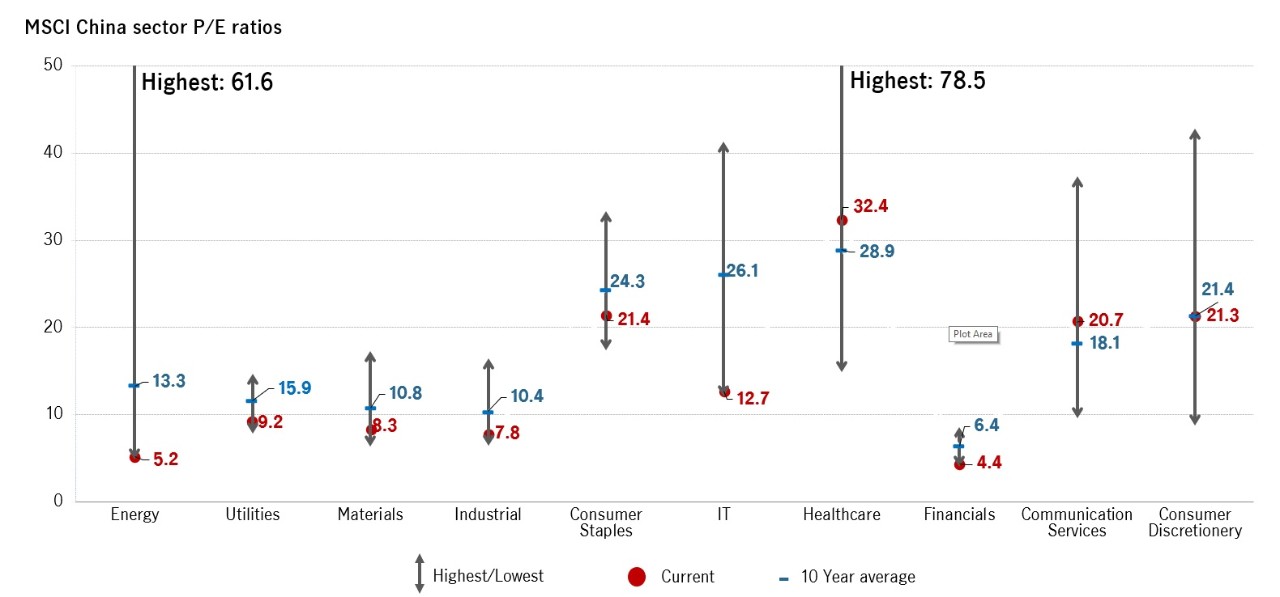

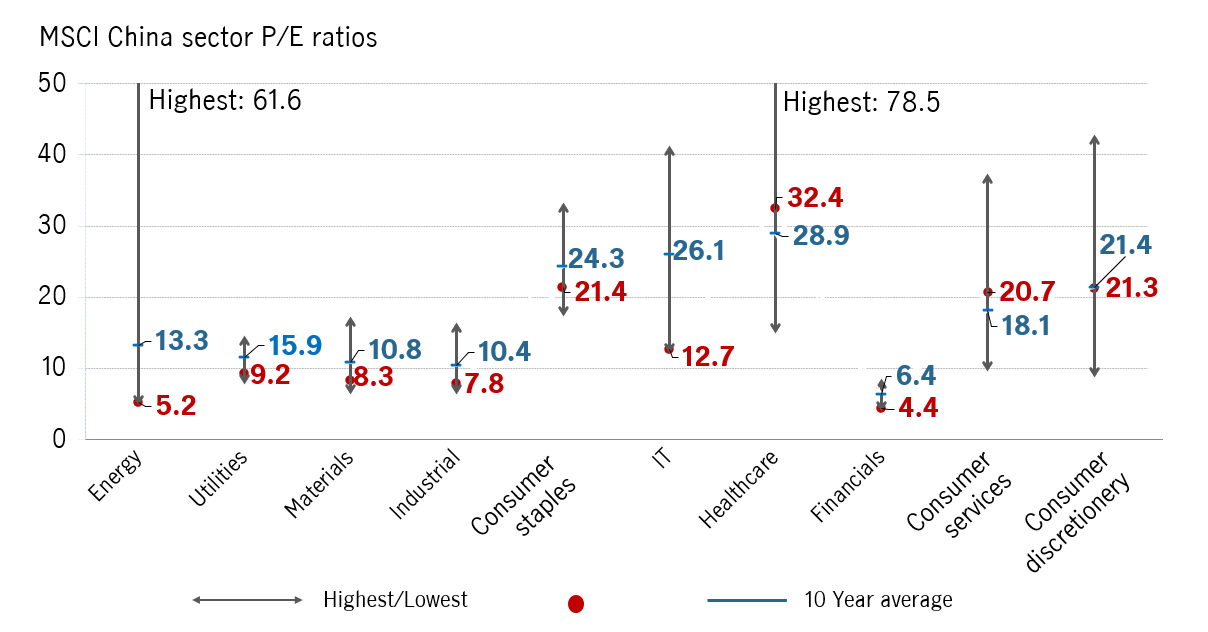

The value has emerged for China’s equity market from a fundamental standpoint. Resumption of daily activities may drive the economic recovery in 2023, which leads to valuation re-rating of numerous sectors.

MSCI China sector P/E ratios3

For more details, please contact your Manulife Financial Planning Manager or bank relationship manager.

Sources:

1. IMF, World Economic Outlook, January 2023. The above information may contain projections or other forward-looking statements regarding future events, targets, management discipline or other expectations, and is only as current as of the date indicated. There is no assurance that such events will occur, and may be significantly different than that shown here.

2. Bloomberg, as of 31 December 2022. Performance in local currency. Represented by MSCI indices. World was represented by the MSCI World Index. US was represented by the S&P 500 Index. Emerging Markets was represented by the MSCI Emerging Markets Index. Asia ex Japan was represented by the MSCI Asia ex Japan Index. China was represented by the MSCI China Index. Shenzhen was represented by the Shenzhen Component Index. Shanghai was represented by the Shanghai Composite Index. ADR/GDR was represented by the MSCI Overseas China Index. Hong Kong was represented by the MSCI Hong Kong Index. China A was represented by CSI300. Zhong Hua was represented by the MSCI Zhong Hua Index. It is not possible to invest directly in an index. Past performance is not indicative of future performance.

3. Bloomberg, as of 4 January 2023.

The above information may contain projections or other forward-looking statements regarding future events, targets, management discipline or other expectations. There is no assurance that such events will occur, and the future course may be significantly different from that shown here.

©1999 - 2024 Manulife Investment Management (Hong Kong) Limited